13 Mar 2018

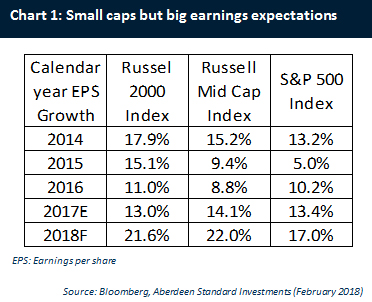

One of the central strands of the tax reform package that recently made its way through the US Congress is a lowering of the corporate tax rate from 35% to 21%. US small-cap companies stand to benefit more than larger ones from this reduction given a higher proportion of their revenues and earnings are generated domestically when compared to big multi-nationals. Consequently, small-caps will see some of the largest reductions in ongoing tax rates. Accelerating GDP growth tends to favour them as well. Consequently, we expect profits growth of as much as 20% net of tax in 2018 for US smaller companies, with non-tax affected operating income rising by about 8% (see Table 1).

However, it is important to note that the broad-based benefit of low inflation appears to be coming to an end. This bolstered corporate margins over the past decade, pushing them through 2007 peak levels, but now looks set to fade given wage growth is starting to accelerate and raw material prices started 2018 at much higher levels than in 2017.

We look for companies that can pass along input cost hikes; pricing power as a theme should be more important in coming years. A key characteristic of such companies is that their customers cannot do without them. Take Lippert Components Inc (LCI) as an example. LCI manufactures components and after-market parts for trailers and RVs, and acts as a distributor for some specialized RV and marine products. As one of the largest component makers for the industry, its share of dollar content per new RV has risen every year of this century. LCI is indispensable to its customers.

Based in a small town in Indiana where the labour market is extremely tight, LCI is experiencing wage pressures as it tries to service 15+% volume growth from customers. While LCI is vital to the ability of its customers to make and sell products, the original equipment manufacturers (OEM) who are the customers raise prices only infrequently during a model year. Historically, OEMs have taken up to five months to acknowledge and be willing to pay for input cost shifts that start suddenly. As a result, LCI’s margins are under pressure from both wage and input cost hikes – for now. That leads to some volatility in margins as prices rise, but not to permanent margin compression.

While the path may not be a straight one, we believe LCI should shortly be able to push pricing and margins higher, allowing earnings to rise on much higher revenue. In addition, LCI’s tax benefits will partly fund higher wages and materials costs, helping to create more stable net margins for a company that has increased its reach over the past decade. Despite short-term challenges, LCI’s story is attractive partly because of the significant improvement in its customers’ end markets. RVs are becoming popular with younger people and the industry forecasts growth well in excess of automobile growth for the next few years.

Another example is AMN Healthcare, a temporary staffing company supplying nurses into a market struggling with a dearth of qualified staff. Given the shortage of nurses, temporary staffing services have become important providers of flexible labour. We like AMN Healthcare’s much more direct approach to dealing with wage inflation and it has been able to pass wage hikes for temporary workers through to end customers, usually hospitals. As a result, AMN’s core employees have enjoyed wage gains well ahead of those in the general economy in recent years and the company’s gross margins have expanded every year since 2008.

In addition to having businesses that sound decidedly low-tech and even unexciting, both LCI and ACM share other characteristics, such as solid balance sheets and high conversion of earnings into cashflow. Those things matter in any environment, but in one where interest rates might rise further our preference is for higher-quality business models that are sustainable even in the case of a policy mishap.

Recently, we have observed markets quickly and somewhat indiscriminately adjusting stock prices, presuming higher earnings as a result of the Tax Cut and Jobs Act. Now there is a more thoughtful reassessment of the real winners and losers of the evolving environment. We view small-cap companies as somewhat undervalued relative to the longer-term premium to large-caps which they deserve. We also recognise the need to be selective about which smaller companies to own. After all, the impacts of inflation, tight input markets and increased competition from companies “reinvesting their tax windfall into price competition” differ across companies. As a result, we look for a smaller and carefully selected group of companies that share strong financial characteristics and the ability to deal with the changes in an economy that has already been expanding for nearly nine years.

Ralph Bassett is Deputy Head of North American Equities, and Douglas Burtnick is Senior Investment Manager, North American Equities, at Aberdeen Standard Investments.

Important Information

The value of investments, and the income from them, can go down as well as up and you may get back less than the amount invested. Past performance is not a guide to future results. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. We recommend that you seek financial advice prior to making an investment decision.

Aberdeen Standard Investments is a brand of the investment businesses of Aberdeen Asset Management and Standard Life Investments.

The details contained in this marketing communication are for information purposes only and should not be considered as an offer, investment recommendation, or solicitation, to deal in any of the investments mentioned herein and does not constitute investment research. Aberdeen Standard Investments does not warrant the accuracy, adequacy or completeness of the information contained herein and expressly disclaims liability for errors or omissions in such information and materials.

Any research or analysis used in the preparation of the information has been procured by Aberdeen Standard Investments for its own use and may have been acted on for its own purpose. Some of the information may contain projections or other forward looking statements regarding future events or future financial performance of countries, markets or companies. These statements are only predictions, opinions or estimates made on a general basis and actual events or results may differ materially.

No information contained herein constitutes investment, tax, legal or any other advice, or an invitation to apply for securities in any jurisdiction where such an offer or invitation is unlawful, or in which the person making such an offer is not qualified to do so.

Third party websites provided by hyperlinks are completely beyond the control of Aberdeen Standard Investments. Accordingly, Aberdeen Standard Investments accept no responsibility for the accuracy, completeness and legality of the contents of such third party website, or for any offers, services and products contained therein.

Issued by:

Aberdeen Asset Managers Limited. Authorised and regulated by the Financial Conduct Authority in the United Kingdom. Registered Office: 10 Queens Terrace, Aberdeen, Aberdeenshire, AB10 1YG. Registered in Scotland No. SC108419.

Standard Life Investments Limited registered in Scotland (SC123321) at 1 George Street, Edinburgh EH2 2LL. Standard Life Investments Limited is authorised and regulated in the UK by the Financial Conduct Authority.