14 Jun 2018

Japan has had a sobering 2018 so far, with both growth and inflation coming in below expectations. Is this likely to trigger a policy response, or should we expect more of the same?

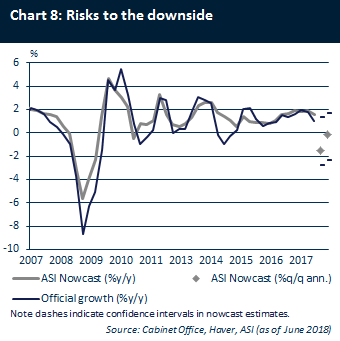

In terms of economic activity, the disappointment of a contraction in Q1 is threatening to turn into a (technical) recession, with our Nowcast framework pointing to another negative quarter in Q2. This is significantly below our judgemental forecast (see Chart 8). This reflects our views that production and sentiment data have been distorted by idiosyncratic factors in the semiconductor sector, rather than a broader downturn in the industrial cycle, and that consumer weakness is adverse weather related. If the downside risks do materialise, this will raise significant questions about the policy outlook. Most notably, pressure will increase on the government to recalibrate its fiscal policy. At present, the government has pencilled in a VAT hike in October 2019. However, even with the additional revenue from this levy, it has been forced into a five-year delay of its target for a primary budget surplus. A final decision on the VAT hike will be taken after the release of the Q3 GDP data – set for November 14th. If momentum does not recover sufficiently, an implementation delay may be on the cards, putting fiscal consolidation plans into turmoil – and potentially testing market lethargy on debt sustainability.

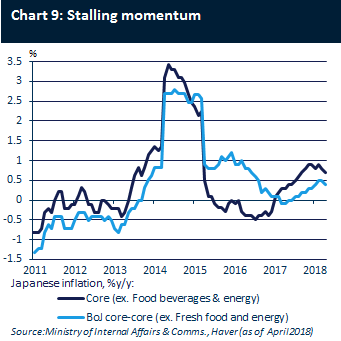

Turning to inflation, the disappointments in H1 have been no less distressing. Inflation has stalled again, with the April core CPI decelerating to 0.7% quarter-on-quarter (q/q), from 0.9% in March. More importantly, the Bank of Japan’s (BoJ) preferred core core measure was a miserly 0.4%q/q in April (see Chart 9). This dashes optimism on the inflation outlook, with the BoJ rumoured to be considering revising down its price outlook – prompting media speculation that it will launch a review at its June and July meetings of why inflation remains so weak. On our key measures of inflation fundamentals, we have observed some positive signs such as a closing of the output gap in 2018 and a sustained rise in core CPI – although this has largely been driven by energy prices. The big disappointment has come in wage setting behaviour, with the labour unions’ fourth estimate of the shunto outcome indicating a 0.53% rise. This is a long way from the 2-3% consistent with the BoJ’s target and only a marginal increase from the 0.48% year-on-year in 2017, versus the BoJ’s hopes for a step change. Further, survey-based measures of inflation expectations have weakened of late. The key question is whether the BoJ will respond. Its new leadership team has retreated from comments guiding markets toward exit of late.

We think the BoJ has been late to recognise the trap it finds itself in. We believe this has two elements. Firstly, essential to any successful policy exit will be improving inflation fundamentals. However, the current Yield Curve Control framework does not provide the firepower to generate sufficient momentum for fundamentals to endure an exit. Secondly, debt sustainability rests increasingly on financial repression, with the government inaugurating a debt-to-GDP target to accompany its primary deficit target. This requires nominal interest rates to remain below nominal GDP for a very long time – meaning a normalisation of debt pricing remains impossible until the government has achieved a primary surplus. The stakes around the price and growth outlook are clearly rising. However, we think policy settings are sufficient for things to get back on track in H2. However, events so far this year have demonstrated Japan’s vulnerability to a downturn.

Govinda Finn is Japan and Developed Asia Economist for Standard Life Investments.

Important Information

The value of investments, and the income from them, can go down as well as up and you may get back less than the amount invested. Past performance is not a guide to future results. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. We recommend that you seek financial advice prior to making an investment decision.

Aberdeen Standard Investments is a brand of the investment businesses of Aberdeen Asset Management and Standard Life Investments.

The details contained in this marketing communication are for information purposes only and should not be considered as an offer, investment recommendation, or solicitation, to deal in any of the investments mentioned herein and does not constitute investment research. Aberdeen Standard Investments does not warrant the accuracy, adequacy or completeness of the information contained herein and expressly disclaims liability for errors or omissions in such information and materials.

Any research or analysis used in the preparation of the information has been procured by Aberdeen Standard Investments for its own use and may have been acted on for its own purpose. Some of the information may contain projections or other forward looking statements regarding future events or future financial performance of countries, markets or companies. These statements are only predictions, opinions or estimates made on a general basis and actual events or results may differ materially.

No information contained herein constitutes investment, tax, legal or any other advice, or an invitation to apply for securities in any jurisdiction where such an offer or invitation is unlawful, or in which the person making such an offer is not qualified to do so.

Third party websites provided by hyperlinks are completely beyond the control of Aberdeen Standard Investments. Accordingly, Aberdeen Standard Investments accept no responsibility for the accuracy, completeness and legality of the contents of such third party website, or for any offers, services and products contained therein.

Issued by:

Aberdeen Asset Managers Limited. Authorised and regulated by the Financial Conduct Authority in the United Kingdom. Registered Office: 10 Queens Terrace, Aberdeen, Aberdeenshire, AB10 1YG. Registered in Scotland No. SC108419.

Standard Life Investments Limited registered in Scotland (SC123321) at 1 George Street, Edinburgh EH2 2LL. Standard Life Investments Limited is authorised and regulated in the UK by the Financial Conduct Authority.