30 Jun 2025

Author | Ross Olusanya, Quantitative Investment Director

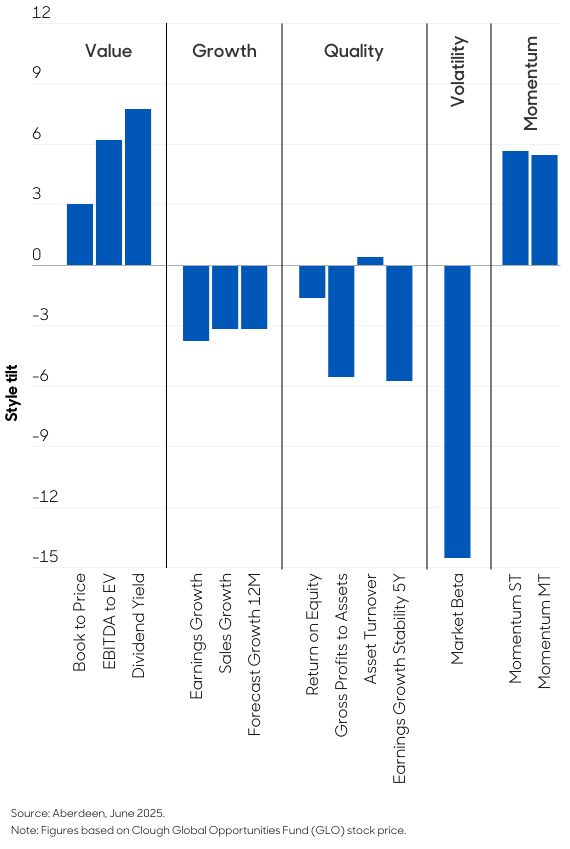

The recent escalation between Israel and Iran offered a live test of how equity styles behave during geopolitical stress.

The following is what we observed (Chart 1), and what it tells us about Momentum, Value, and Quality in volatile markets:

Momentum held up because it had already rotated into defensive stocks

Value performed, but thanks to energy and utilities, not cheapness

Quality lagged as many high-quality stocks still carried interest rate or market risk

Chart 1. Israel-Iran conflict factor style skyline

In systematic strategies like enhanced indexing, investors knowing what they truly own – and how it’s positioned – is critical to navigating risk.

Factors aren’t static. Their behavior reflects not just economic conditions but also investor positioning and sentiment. By looking under the hood, we believe investors can better prepare their portfolios for the next surprise and not just react to shocks but also anticipate how style exposures will respond.

Key style insights

The following provides several important dynamics among investment styles and factors:

Low beta vs. High beta

In response to the Israeli attack on Iran on June 13, low beta stocks (e.g., consumer staples, utilities, etc.) outperformed strongly, while high-beta stocks sold off.

Why? Investors sought safety in stable, lower-volatility names. Once hopes for a ceasefire rose, the pattern reversed, and high-beta names bounced back.

The takeaway

Fear trading = long low beta and short high beta, while relief trading meant the opposite.

Momentum surprises

Typically, a sudden shock breaks the momentum factor (as yesterday’s momentum leaders crash and laggards soar). Yet momentum strategies delivered positive returns, especially on June 13.

Why? Recent momentum had rotated into defensive names before the conflict. For months, uncertainty has been the new normal, so traders were riding trends in low beta stocks. So, when the news of the bombing occurred, those trends accelerated instead of reversing.

The takeaway

This underscores how momentum is context-dependent, and in this case, its winners were the market’s defensive stalwarts.

Value’s sector secret

Value stocks, often seen as cyclical and riskier, performed well at the start of the crisis, but not because investors suddenly developed an appetite for cheap stocks. Its outperformance came largely from sector exposure, particularly to Energy and Utilities. Strip those sectors out, and Value wouldn’t have looked so defensive.

Why? Many value names in sectors, such as Energy and Utilities, benefited from surging oil and a flight to safety. In our factor decomposition, dividend yield and other value metrics were significant positive contributors on June 13.

Vs. growth

Growth stocks, however, especially high-growth tech, underperformed, which is often due to their longer duration and tendency to be sold off as yields and risk aversion spike.

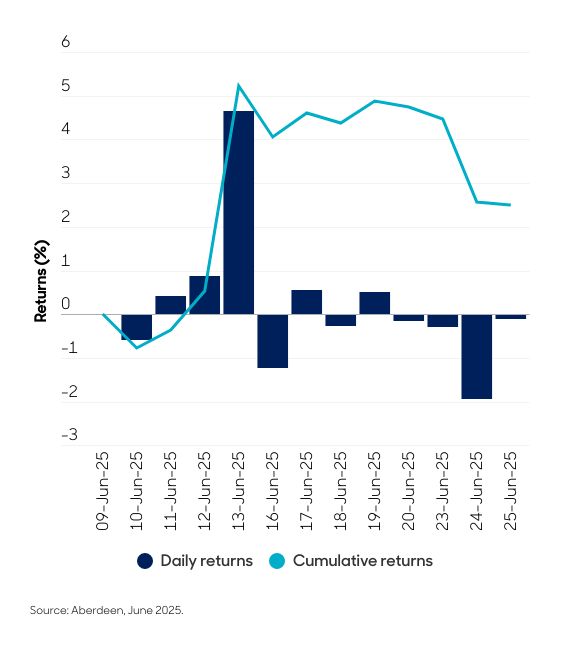

When tensions subsided, growth resumed. News of a potential ceasefire broke on June 24, and markets reacted rapidly: oil prices fell, high beta and cyclicals rebounded, while defensive stocks lagged. Factor exposures reversed just as quickly, the short book rallied, and prior defensive longs faded. It was a textbook risk-on relief rally (Chart 2).

Chart 2. Israel-Iran conflict factor daily returns

The takeaway

Value’s behavior isn’t always about valuation; it’s often about what’s inside: its sector mix (oil and utilities). How you define your factors and whether they are sector-neutral can have a significant impact on returns.

Quality not always a safe haven

Quality stocks, or companies with strong balance sheets, stable earnings, high return on equity, etc., saw mediocre performance in the initial shock.

Why? Many quality companies – think big tech or premium consumer brands – still carry market risk. Plus, quality isn’t the same as low beta. Investors can be attracted to a high-quality business, but it may still be cyclical or sensitive to interest rates.

The takeaway

In crisis mode, quality wasn’t a primary focus; instead, investors prioritized explicitly low-risk factors, such as low beta and dividend yield.

So, what’s the big picture?

During extreme events, whether geopolitical, social, or environmental, markets tend to behave in a playbook-like fashion, albeit with some twists that reflect the current times. In this case, a few conclusions:

Composition matters

Broad labels like value or growth may be misleading. However, within value, for example, the sector composition (energy, utilities, etc.) was critical to its success in this conflict. Understanding why a factor behaves a certain way (e.g., value performance hinged on oil prices) is crucial. Investors need to know what they truly own beneath the surface of the factors.

Momentum and positioning

The fact that momentum didn’t break reveals a great deal about market positioning before the conflict. It appears that many were already in defensive positions before the missiles were launched. When one extreme tail risk follows another, the market’s earlier positioning can either soften or intensify the impact on factors. In this case, it softened the blow with momentum, having already moved to safer names, which helped it withstand the storm.

Final thoughts

Markets will always have surprises. However, by delving into the behavior of styles and factors, we aim to stay one step ahead, positioning our portfolios to withstand shocks and seize opportunities. There’s often a lot more going on, and as investors, it pays to pay attention.

Important information

Projections are offered as opinion and are not reflective of potential performance. Projections are not guaranteed, and actual events or results may differ materially.

Open-end Mutual Funds and ETF Disclosure:

INFORMATION REGARDING MUTUAL FUNDS/ETFS: Investors should carefully consider the investment objectives, risks, fees, charges, and expenses of a mutual fund or ETF before investing. The summary and full prospectuses contain this and other information about the mutual fund or ETF and should be read carefully before investing. To obtain a prospectus for the Mutual Funds, contact Aberdeen Fund Distributors, LLC at 1-866-667-9231 or download it from this site. To obtain a prospectus for the ETFs, contact Aberdeen Investments at 1-844-383-7289 or download it from this site.

Investing in mutual funds and ETFs involves risk, including possible loss of principal. There is no assurance that the investment objective of any fund will be achieved. ETF shares are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. As a result, an investor may pay more than net asset value when buying and receive less than net asset value when selling. In addition, brokerage commissions will reduce returns. Fund shares are not individually redeemable directly with the Fund but blocks of shares may be acquired from the Fund and tendered for redemption to the Fund by certain institutional investors in Creation Units.

Aberdeen Investments Global is the trade name of Aberdeen's investments business, herein referred to as "Aberdeen Investments" or "Aberdeen". In the United States, Aberdeen Investments refers to the following affiliated, registered investment advisers: abrdn Inc., abrdn Investments Limited, and abrdn Asia Limited. abrdn Inc. has been registered as an investment adviser under the Investment Advisers Act of 1940 since August 23, 1995.

Aberdeen Fund Distributors, LLC is a wholly owned subsidiary of abrdn Inc. abrdn Inc. is a wholly-owned subsidiary of Aberdeen Group plc. abrdn’s mutual funds are distributed by Aberdeen Fund Distributors LLC, Member FINRA and SIPC. 1900 Market Street, Suite 200, Philadelphia PA, 19103.

Aberdeen Investment's exchange-traded funds are distributed by ALPS Distributors, Inc. ALPS is not affiliated with Aberdeen Investments.

1940 Act Commodity ETF Disclosure: Bloomberg®, Bloomberg Commodity Index Total ReturnSM, Bloomberg Commodity Index 3 Month Forward Total ReturnSM and Bloomberg Industrial Metals Subindex Total ReturnSM are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the indices (collectively, “Bloomberg”) and have been licensed for use for certain purposes by abrdn Inc. Bloomberg is not affiliated with abrdn Inc., and Bloomberg does not approve, endorse, review, or recommend abrdn Bloomberg All Commodity Strategy K-1 abrdn Inc, abrdn Bloomberg All Commodity Longer Dated Strategy K-1 abrdn Inc and abrdn Bloomberg Industrial Metals K-1 abrdn Inc. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to Bloomberg Commodity Index Total ReturnSM, Bloomberg Commodity Index 3 Month Forward Total ReturnSM and Bloomberg Industrial Metals Subindex Total ReturnSM.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

1933 Act Fund ETF Disclosure:

The statements and opinions expressed are those of the author and are as of the date of this report. All information is historical and not indicative of future results and subject to change. Reader should not assume that an investment in any securities and/or precious metals mentioned was or would be profitable in the future. This information is not a recommendation to buy or sell. Past performance is not a guide to future results.

abrdn Silver ETF Trust, abrdn Gold ETF Trust, abrdn Platinum ETF Trust, abrdn Palladium ETF Trust and abrdn Precious Metals Basket ETF Trust are not investment companies registered under the Investment Company Act of 1940 or a commodity pool for purposes of the Commodity Exchange Act. Shares of the Trusts are not subject to the same regulatory requirements as mutual funds. These investments are not suitable for all investors. Trusts focusing on a single commodity generally experience greater volatility.

Commodities generally are volatile and are not suitable for all investors. Trusts focusing on a single commodity generally experience greater volatility. Please refer to the prospectus for complete information regarding all risks associated with the Trusts.

Investors buy and sell shares on a secondary market (i.e., not directly from Trusts). Only market makers or “authorized participants” may trade directly with the Trusts, typically in blocks of 50,000 to 100,000 shares. Commodities generally are volatile and are not suitable for all investors.

This material must be accompanied or preceded by the prospectus. Carefully consider the investment objectives, risk factors, and fees and expenses of each Trust before investing. To view the prospectus, please click here – abrdn Silver ETF Trust, abrdn Gold ETF Trust, abrdn Platinum ETF Trust, abrdn Palladium ETF Trust and abrdn Precious Metals Basket ETF Trust.

ALPS Distributors, Inc. is the marketing agent for abrdn Silver ETF Trust, abrdn Gold ETF Trust, abrdn Platinum ETF Trust, abrdn Palladium ETF Trust and abrdn Precious Metals Basket ETF Trust.

Closed-end Funds Disclosure

Closed-end funds are traded on the secondary market through one of the stock exchanges. Investment return and principal value will fluctuate so that an investor’s shares may be worth more or less than the original cost. Shares of closed-end funds may trade above (a premium) or below (a discount) the net asset value (NAV) of the fund’s portfolio. NAV return data includes investment management fees, custodial charges and administrative fees (such as Director and legal fees) and assumes the reinvestment of all distributions. Returns for periods less than one year are not annualized. There is no assurance any Fund will achieve its investment objective. Past performance does not guarantee future results.

International investing entails special risk considerations, including currency fluctuations, lower liquidity, economic and political risks, and differences in accounting methods. These risks are generally heightened for emerging market investments. Foreign securities are more volatile, harder to price and less liquid than U.S. securities.

There are also risks associated with international investing, including the risk of investing in a single-country Fund. Concentrating investments in a single region region subjects the Fund to more volatility and greater risk of loss than geographically diverse funds.

Equity stocks of small and mid-cap companies carry greater risk, and more volatility than equity stocks of larger, more established companies.

Dividends are not guaranteed and a company’s future ability to pay dividends may be limited. The use of leverage will also increase market exposure and magnify risk.

Fixed income securities are subject to certain risks including, but not limited to: interest rate (changes in interest rates may cause a decline in the market value of an investment), credit (changes in the financial condition of the issuer, borrower, counterparty, or underlying collateral), prepayment (debt issuers may repay or refinance their loans or obligations earlier than anticipated), and extension (principal repayments may not occur as quickly as anticipated, causing the expected maturity of a security to increase).

Because the real estate funds concentrate their investments in the real estate industry, the portfolio may experience more volatility and be exposed to greater risk than the portfolios of many other mutual funds. Risks associated with investment in securities of companies in the real estate industry may include: declines in the value of real estate, overbuilding and increased competition; increases in property taxes and operating expenses; changes in zoning laws; casualty or condemnation losses; variations in rental income, neighborhood values, changes in interest rates and changes in economic conditions.

Infrastructure-related issuers may be subject to a variety of factors that may adversely affect their business or operations, including high interest costs in connection with capital construction programs, high leverage, costs associated with environmental and other regulations, the effects of economic slowdown, surplus capacity, increased competition from other providers of services, uncertainties concerning the availability of fuel at reasonable prices, the effects of energy conservation policies and other factors.

The Fund’s investments in private companies may be subject to higher risk than investments in securities of public companies.

Investments in HQH, THQ, HQL, and THW may be subject to additional risks including limited operating history, security selection, concentration in the healthcare industries, pharmaceuticals sector, biotechnology industry, managed care sector, life science and tool industry, healthcare technology sector, healthcare services sector, healthcare supplies sector, healthcare facilities sector, healthcare equipment sector, healthcare distributors sector, healthcare REIT, interest rate, credit/default, non-investment grade securities, key personnel, discount to NAV, anti-takeover provisions, related party transactions, non-diversification, government intervention, market disruption, geopolitical, and potential conflicts of interest.

As of 9/30/2023, Tekla Capital Management LLC was the Fund’s investment manager. Effective immediately after the market close on 10/27/2023, abrdn Inc. became the Fund’s investment manager. Destra Capital Advisors LLC, a registered investment advisor, is providing secondary market servicing for the Fund

The Market Price is the current price at which an asset can be bought or sold. There is no assurance that the Fund will achieve its investment objective. Past performance does not guarantee future results.

Please see the Fund’s most recent annual report for more information on risks applicable to the Fund.