31 Mar 2026

In this series, Christine Baalham and Tom Record, portfolio managers of Fidelity World and Global Special Situations, profile a mix of well-known and under-the-radar companies from across the portfolios. Below, they explore the use of AI in banking – a part of the market not typically associated with technological elegance, using Belgium’s KBC Groupe to illustrate what happens when digital capability is treated as core infrastructure rather than an incremental enhancement.

European banks enjoyed a rare alignment of forces in 2025. Cyclical, structural and policy tailwinds converged just as fundamentals were strengthening, underpinning a period of notable outperformance. It would be easy to assume the story is now largely told. Yet beneath the surface, the sector is offering one of the more compelling and underappreciated AI narratives. Banking is a part of the market not typically associated with technological elegance, but one where business models are quietly evolving and where the considered application of AI can deliver tangible, economically meaningful gains.

Following years of post-Global Financial Crisis restructuring and digitalisation, cost bases across European banks have quietly stabilised. Operating expenses have been broadly flat even as revenues have grown. This decoupling of growth from cost is historically unusual for the sector and provides fertile ground for AI to act as an accelerant.

The investment opportunity centres on pragmatism. Financial services are rich in standardised, repeatable processes and employ large numbers of knowledge workers, meaning tangible productivity gains can be very real here.

Much of the excitement around AI centres on productivity gains. In the banking space, risk, compliance, Know Your Client requirements, customer servicing and internal operations account for a significant share of banks’ cost bases. These functions have expanded materially over the past decade as regulation intensified, often relying on manual processes and growing headcount. AI offers a way to reverse this trend: automating checks, accelerating decision-making and reducing error rates, while improving customer experience.

Importantly, this is not about wholesale disruption. In many European markets, labour laws, culture and public scrutiny mean that change will be gradual. Natural attrition, redeployment and incremental productivity gains matter far more than dramatic headline cuts. But over time, even modest annual improvements can compound into meaningful value creation.

In many respects, the Nordic banks illustrate what the industry is aiming for. Their structurally lower cost-income ratios, often below 40%, reflect earlier digitalisation, simpler product sets and cleaner IT estates. AI is now being used to extend that advantage, rather than create it, by automating mortgage approvals, credit decisions and anti-money laundering (AML) processes.

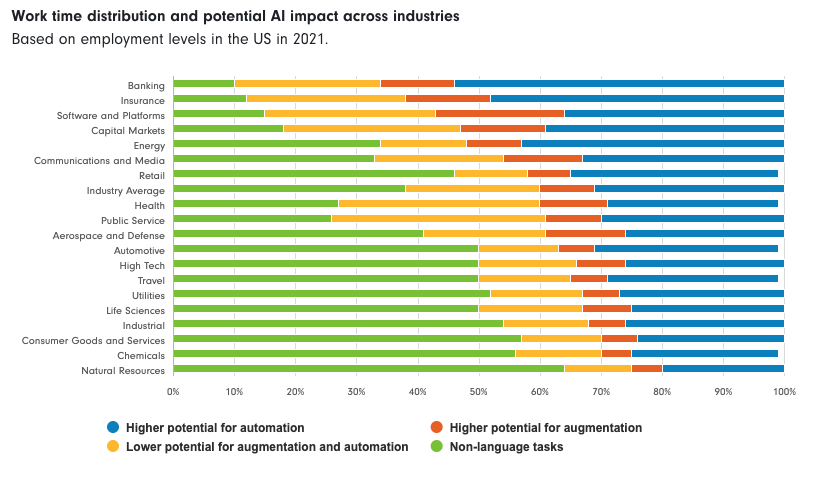

Source: Accenture Presentation ‘A new era of generative AI for everyone’ Link. May 2023. Chart recreated by Fidelity International for illustrative purposes only. The underlying analysis is the work of Accenture and does not constitute investment research or a recommendation. Accenture Research based on analysis of Occupational Information Network (O*NET), US Dept. of Labor; US Bureau of Labor Statistics. Notes from the report: We manually identified 200 tasks related to language (out of 332 included in BLS), which were linked to industries using their share in each occupation and the occupations’ employment level in each industry. Tasks with higher potential for automation can be transformed by LLMs with reduced involvement from a human worker. Tasks with higher potential for augmentation are those in which LLMs would need more involvement from human workers.

While the Nordics might be perceived as a credible benchmark for what is achievable elsewhere in Europe, it is Belgium’s KBC Groupe that illustrates what happens when digital capability is treated as core infrastructure rather than an incremental enhancement.

KBC is a bancassurance group with leading retail franchises in Belgium and selected Central and Eastern European markets, combining banking and insurance through a highly integrated operating model. Its focus on being a ‘big player in small countries’ underpins a stable, customer-centric core business with strong capital generation and repeatable economics.

Crucially, this operating discipline has been reinforced by leadership continuity. CEO Johan Thijs has been at the helm for over a decade and has consistently emphasised the strategic importance of digital investment. Long before AI became a dominant market narrative, KBC was investing heavily in its technology ‘real estate’ by modernising systems, simplifying architecture and embedding digital capability across the organisation.

This early investment matters. Many large incumbents remain constrained by fragmented legacy systems that limit what technology can deliver beyond the front end. Customer interfaces may appear slick, but complexity beneath the surface often prevents true front-to-back automation. KBC enters the current phase of AI adoption without that baggage. The foundations were laid early, allowing innovation to compound rather than stall.

At the heart of this sits ‘Kate’, the group’s digital backbone described by management as the ‘brain of the business’. Kate is not a chatbot layered on top of legacy processes, but an integrated system spanning front and back office, continually evolving as capabilities expand.

Kate convinces customers

Source: KBC Groupe Company Presentation 3Q 2025. Link. Graphics and stats recreated by Fidelity International for illustrative purposes only. The underlying analysis is the work of KBC Groupe and does not constitute investment research or a recommendation.

Today, a significant majority of commercial workflows are handled through straight-through processing (STP) without human intervention. Contextual AI, which combines information from different sources to better understand a situation, enables Kate to resolve most customer interactions while simultaneously triggering downstream processes such as fraud checks, underwriting decisions and claims allocation.

In practice, Kate independently resolves around 70% of customer queries, equivalent to the workload of roughly 350 full-time employees. However, as customer expectations continue to rise, Kate has evolved. In 2025, Kate was upgraded to more advanced large language models, enabling it to handle more complex queries, retain context and respond in a more natural, human way. The result has been improved customer satisfaction and a clear step in Kate’s evolution from a functional chatbot towards a true digital assistant that saves customers time and money.

By automating routine, repetitive tasks across customer service and internal processing, Kate allows staff to focus on higher-value activities such as complex advice, relationship management and exception handling where judgement truly matters.

With personnel forming most of the cost base and wage inflation structurally embedded through indexation, AI-led productivity is essential. KBC uses automation to redeploy staff, manage natural attrition and protect margins.

The outcome is not simply lower cost, but greater scalability, improved service quality and strategic optionality. Importantly, this model is replicable across geographies and supports future expansion without proportionate increases in complexity.

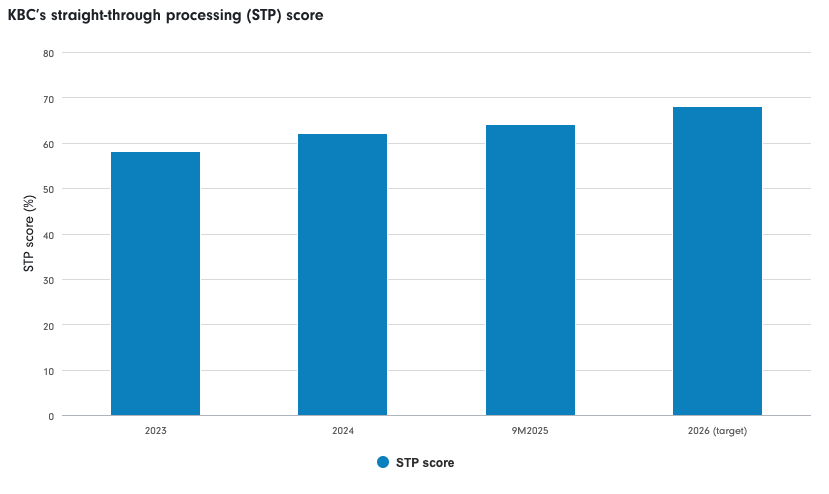

A defining feature of KBC’s technological advantage is its routine disclosure and internal measurement of straight-through processing (STP). While many banks reference automation in broad terms, KBC consistently reports that around two-thirds of its commercial processes are fully automated – a level of transparency beyond the industry standard.

Source: KBC Groupe Company Presentation 3Q 2025. Link. Graphics and stats recreated by Fidelity International for illustrative purposes only. The underlying analysis is the work of KBC Groupe and does not constitute investment research or a recommendation. Note: The STP ratio measures how many of the services that can be offered digitally are processed without any human intervention and this from the moment of interaction by a client until the final approval by KBC. *Based on analysis of all retail processes.

This disclosure matters because it reflects reality. Across much of the banking sector, automation remains partial, siloed or confined to customer interfaces. Legacy architectures often prevent processes from flowing seamlessly from initiation to completion. KBC stands apart because automation is genuinely front-to-back, rather than cosmetic. In mortgages and loans, Kate does not simply gather customer information – it connects directly into credit decisioning, documentation and fulfilment systems. Human intervention is reserved for exceptions where absolute accuracy is required, rather than embedded by default.

This distinction is critical. True STP shortens processing times, reduces error rates and allows productivity gains to compound across thousands of transactions. It also explains why KBC can credibly offset rising wage costs through efficiency and redeployment, while peers remain constrained by systems that look modern at the surface but retain manual intensity beneath. In this context, STP is not a technical footnote. It is evidence of a structural operating advantage that many peers are still working towards.

AI should not be viewed as a standalone sector, but as an enabling force that cuts across industries. A balanced approach looks beyond the most visible narratives, to identify where adoption is disciplined, repeatable and economically meaningful. Early phases of technological change tend to reward visibility and excitement, while later phases reward execution. In financials, AI is not replacing the banking model, but rather improving it. These developments reflect a ‘quiet change’ - as efficiency gains translate into higher returns on equity and more resilient profitability, the market may gradually reassess what these businesses are worth.

The balanced investor recognises that different expressions of the same technology can coexist, and that some of the most attractive risk-adjusted opportunities often sit away from the most crowded ideas.

Important information

This information must not be reproduced or circulated without prior permission. This material is for Institutional Investors and Investment Professionals only, and should not be distributed to the general public or be relied upon by private investors. This material is provided for information purposes only and is intended only for the person or entity to which it is sent. It must not be reproduced or circulated to any other party without prior permission of Fidelity.

This material does not constitute a distribution, an offer or solicitation to engage the investment management services of Fidelity, or an offer to buy or sell or the solicitation of any offer to buy or sell any securities in any jurisdiction or country where such distribution or offer is not authorised or would be contrary to local laws or regulations. Fidelity makes no representations that the contents are appropriate for use in all locations or that the transactions or services discussed are available or appropriate for sale or use in all jurisdictions or countries or by all investors or counterparties. This communication is not directed at, and must not be acted on by persons inside the United States. All persons and entities accessing the information do so on their own initiative and are responsible for compliance with applicable local laws and regulations and should consult their professional advisers. This material may contain materials from third-parties which are supplied by companies that are not affiliated with any Fidelity entity (Third-Party Content). Fidelity has not been involved in the preparation, adoption or editing of such third-party materials and does not explicitly or implicitly endorse or approve such content. Fidelity International is not responsible for any errors or omissions relating to specific information provided by third parties.

Fidelity International refers to the group of companies which form the global investment management organization that provides products and services in designated jurisdictions outside of North America. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. Fidelity only offers information on products and services and does not provide investment advice based on individual circumstances, other than when specifically stipulated by an appropriately authorised firm, in a formal communication with the client.

Europe: Issued by FIL Pensions Management (authorised and regulated by the Financial Conduct Authority in UK), FIL (Luxembourg) S.A. (authorised and supervised by the CSSF, Commission de Surveillance du Secteur Financier), FIL Gestion (authorised and supervised by the AMF (Autorité des Marchés Financiers) N°GP03-004, 21 Avenue Kléber, 75016 Paris) and FIL Investment Switzerland AG.

In Hong Kong, this material is issued by FIL Investment Management (Hong Kong) Limited and it has not been reviewed by the Securities and Future Commission.

FIL Investment Management (Singapore) Limited (Co. Reg. No: 199006300E) is the legal representative of Fidelity International in Singapore. This document / advertisement has not been reviewed by the Monetary Authority of Singapore.

In Taiwan, Independently operated by Fidelity Securities Investment Trust Co. (Taiwan) Limited 11F, No.68, Zhongxiao East Road, Section 5, Taipei 110, Taiwan, R.O.C. Customer Service Number: 0800-00-9911.

In Korea, this material is issued by FIL Asset Management (Korea) Limited. This material has not been reviewed by the Financial Supervisory Service, and is intended for the general information of institutional and professional investors only to which it is sent.

In China, Fidelity China refers to FIL Fund Management (China) Company Limited. Investment involves risks. Business separation mechanism is conducted between Fidelity China and the shareholders. The shareholders do not directly participate in investment and operation of fund property. Past performance is not a reliable indicator of future results, nor the guarantee for the performance of the portfolio managed by Fidelity China.

Issued in Japan, this material is prepared by FIL Investments (Japan) Limited (hereafter called “FIJ”) based on reliable data, but FIJ is not held liable for its accuracy or completeness. Information in this material is good for the date and time of preparation, and is subject to change without prior notice depending on the market environments and other conditions. All rights concerning this material except quotations are held by FIJ, and should by no means be used or copied partially or wholly for any purpose without permission. This material aims at providing information for your reference only but does not aim to recommend or solicit funds /securities.

UAE: The DIFC branch of FIL Distributors International Limited is regulated by the DFSA for the provision of Arranging Deals in Investments only. All communications and services are directed at Professional Clients and Market Counterparties only. Persons other than Professional Clients and Market Counterparties, such as Retail Clients, are NOT the intended recipients of our communications or services. The branch is established pursuant to the DIFC Companies Law, with registration number CL2923, as a branch of FIL Distributors International Limited, registered in Bermuda. FIL Distributors International Limited is licensed to conduct investment business by the Bermuda Monetary Authority.

For information purposes only. Neither FIL Limited nor any member within the Fidelity Group is licensed to carry out fund management activities in Brunei, Indonesia, Malaysia, Thailand and Philippines.

GLEMUS5742-0526