07 Apr 2026

Download this article in flyer format

Investors are increasingly being forced to make decisions under conditions of heightened uncertainty, as several key capital market drivers have become less predictable in recent years. For example, the trend of geoeconomic fragmentation is characterised by binary policy decisions with potentially significant macro ramifications that can occur without notice. Meanwhile, in the world’s dominant economy, the US, the government’s fiscal requirements are complicating the job of monetary policymakers at a time when inflationary pressures appear sticky and the realignment of global capital flows is affecting US dollar exchange rates. The interplay of different policies and their implications is therefore less clear.

At the same time, the inter-related dynamics surrounding AI innovation, investment, adoption and economic disruption are highly complex, making top-down and bottom-up outcomes hard to forecast. For example, the technology could drive inflationary or disinflationary outcomes depending on the trajectory of investment activity and the ways in which disruption occurs.

These layers of uncertainty come at a time when global capital markets are exhibiting high levels of concentration and valuation dispersion, partly due to the related dominance of the US and AI themes. The enormous level of AI investment and its associated wealth effects are driving robust US growth, outweighing fragmentation headwinds like tariff-related inflationary pressures, higher term premia, and a weaker dollar. However, the narrowness of this growth makes portfolios that depend on it relatively fragile.

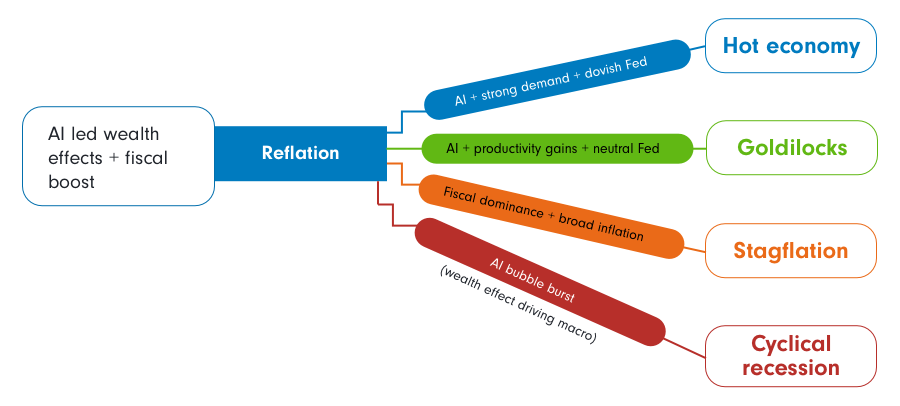

Although US growth could broaden in the near term if fiscal and monetary stimulus drive a cyclical upturn, if this is perceived to undermine the Fed’s ability to maintain price stability a loss of credibility could require remedies which result in stagflationary longer-term outcomes. Such conflicting dynamics make a range of US macro scenarios possible and volatility is likely to remain elevated until investors gain clarity on which will play out. In the meantime, they will have to find ways to address the associated risks.

A range of US macro scenarios remain possible

Source: Fidelity International, 31 January 2026.

From an asset allocation perspective, more positive asset class return correlations are likely to be among the key consequences of this new, more uncertain regime. If debt markets are more influenced by fiscal policy and less predictable, term premia may remain higher and more volatile, raising bond-equity return correlations and weakening the diversifying potential of duration exposure within multi-asset portfolios.

Under such conditions, traditional 60/40 portfolios may deliver lower risk-adjusted returns than investors have become accustomed to. Despite this, the long-term benefits of exposure to equities, bonds, and private assets remain compelling, so investors should put cash to work. New methods of investment selection and portfolio construction will simply be required to embed stability into portfolios alongside return potential.

“Only when the tide goes out do you discover who's been swimming naked.”

Warren Buffett

In a more competitive world of geoeconomic fragmentation, investing is not about predicting the next shock but accepting that shocks are now an inherent and unpreventable feature of the environment that must be managed. In such an environment, investors must broaden their horizons and employ a more layered approach to investment selection and portfolio construction, using a more varied toolkit to access a wider range of differentiated risk premia. The balanced portfolio is not dead, but it needs updating for today’s new regime.

A key factor will be the ability to employ active management in the face of narrow market leadership and high valuation dispersion, each of which increase the importance of certain idiosyncratic bottom-up risk and return drivers. Environments with these characteristics tend to raise the potential for research-informed strategies to convert heterogeneity into alpha.

Visit our page to see the full list of levers.