10 Apr 2026

The US’s actions in Iran, Venezuela, rhetoric around Greenland, and ongoing tariff threats are the actions of a traditional hegemon rather than a steward of a globalist system. Alongside Germany’s shift towards expansionary fiscal policy and Canada’s calls for the middle powers to unite, they are symptomatic of intensifying geoeconomic fragmentation.

This is not cyclical noise, but a structural regime shift towards fiercer ongoing international competition. The dynamics are unpredictable and inherently non-linear, with the potential to affect market conditions abruptly and significantly. Macroeconomic volatility, a proxy for inflation and growth uncertainty, has increased.

Among the key factors underpinning US actions are its twin deficits. President Trump has blamed the trade deficit explicitly for the socioeconomic woes of his electoral support base, with protectionist trade policies his cure. He also views strong US GDP growth as a symbol of superiority in today’s more fragmented world, but the One Big Beautiful Bill Act’s tax cuts which are designed to boost growth may also widen the government’s fiscal deficit. This could result in a period of fiscal dominance and financial repression, particularly given that the Fed has shifted its reaction function towards growth support at a time when inflation remains above target.

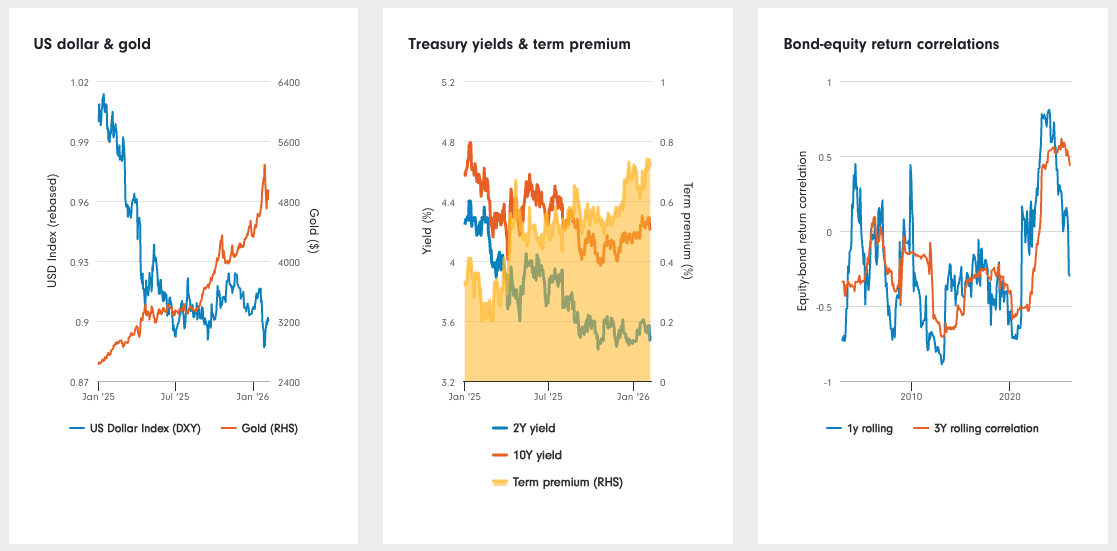

Treasury investors have taken note, with some US creditor nations adjusting their reserve policies. Over the past year, this has affected a realignment of global capital flows, a weakening of the dollar (which is unusual during periods of strong US growth), and a rapid increase in the prices of alternative reserve assets like gold. Another critical consequence has been a rise in the term premium, the extra yield that investors demand for holding long-term Treasuries rather than rolling over shorter-term equivalents. This has kept long-term yields elevated even as more policy-sensitive shorter-term equivalents have moved lower over the past year.

These dynamics have important implications for investors. Long-term bonds provide a source of higher nominal income, but equity and fixed income returns could remain more correlated and the ability of duration exposure to hedge equity risk may remain reduced (outside of a recession scenario). There is also greater risk that high long-term Treasury yields could catalyse bouts of equity market volatility; this has historically often been the case when 10-year yields rise above 5% (per the Fed Stock Valuation Model). The potential for such an outcome is worth monitoring closely amid changes to the Fed’s leadership, particularly given that the valuations of real assets like equities arguably benefitted from an ‘easy money’ dollar debasement narrative in 2025.

Past performance is not an indication of future results.

Source: Fidelity International, LSEG DataStream, 6 February 2026. Term premium = 10-year minus 2-year yield. Rolling correlations of monthly S&P 500 and ICE BofA US Treasury index total returns.

A fragmenting world is inherently a less globalised world. Old alliances may be undone, but new ones will be forged as decoupling intensifies and the world becomes more multipolar. In this new world, influence and control will matter more. Self-sufficiency will be prioritised over interdependence, with just-in-time strategies that prioritise efficiency replaced by just-in-case approaches in the name of resilience.

Unpredictable shocks have become an inherent feature of the backdrop, raising volatility and making investment fundamentals more fragile. Timing markets becomes even more difficult and with established diversification principles being called into question, the ability to spread risk across multiple sources of return becomes more important.

The policies underpinning the US’s grand strategy of geopolitical retrenchment, rebuilding of its industrial base, and repair of a left-behind middle class have weakened key pillars of US exceptionalism. This is occurring at a time when the US remains the dominant component of global capital markets and its assets command premium valuations, but its government’s interventionist stance is challenging the market-friendly narrative embedded within this pricing. For example, US corporates are encouraged to bear the impacts of tariff hikes rather than pass them on to consumers. Active exposure to the US market remains warranted as it continues to offer an array of attractive opportunities, but it is also prudent to reassess equity allocations and disperse risk geographically.

The lagged impact of recent monetary easing and Germany’s fiscal impulse remain key tailwinds. Despite their recent outperformance, European equities continue to trade at a discount to their US counterparts amid ongoing tensions, even in some areas where earnings growth trends are favourable. Selective stock-picking can exploit such valuation gaps. Meanwhile, the euro remains the most obvious beneficiary of US dollar weakness. The UK equity market also stands out for its high yield and deep valuation discount.

The emerging markets stand to benefit from strong macroeconomic fundamentals, easing global financial conditions and improving capital flows. The diverse region provides an array of unique idiosyncratic opportunities in areas like commodity supply and demographic-linked growth, as well as access to the AI theme through Asia. Fiscal positions look favourable in many markets, particularly in context of US debt sustainability concerns, while largely controlled inflation provides scope for monetary policy support. Despite these dynamics, equity valuations trade near multi-decade discounts to their US counterparts, albeit with a high level of dispersion across the region that justifies discerning investment selection. Emerging market debt also looks attractive, helped by favourable currency dynamics.

At a time when differentiated exposures are desirable, Japan presents a particularly interesting opportunity. After years of subdued inflation and extremely low rates, the domestic policy backdrop is shifting strongly towards growth and reflation, particularly following the new Takaichi government’s recent election victory. Factors like corporate governance reform provide additional potential tailwinds.

Across Asia, monetary policy stances are likely to ease in support of growth as inflation is largely a non-issue for most of the region. China is using consistent policy to ward off deflation while resilient manufacturing and exports underpin its growth; it may also roll out further fiscal support to support consumption. The rapid development of China’s AI capabilities provides interesting opportunities as it seeks to boost innovation and adoption rapidly across its vast domestic markets, while Korea and Taiwan also hold critical and differentiated positions in global AI supply chains. Additional tailwinds include demographic dividends in key growth markets like India and Indonesia, corporate reforms, and global diversification trends.

Anthony Bolton