07 Apr 2026

The shift towards digital labour represents one of the biggest business model pivots of all time, with huge ramifications for virtually every industry. It is already propelling US growth through unprecedented corporate capital spending, which shows no sign of abating even if financing is increasingly debt-fuelled and circular in places. The hugely cash-generative hyperscalers continue to commit to massive investments, underpinning impressive earnings from AI infrastructure supply chain businesses such as semiconductor manufacturers, energy providers and certain commodity suppliers, especially where inventories are scarce.

However, technological revolutions rarely proceed smoothly. Investors’ focus is increasingly shifting towards the question of whether capex and equity valuations will be justified by the monetisation of AI-driven productivity. Elevated valuations and astronomical financing requirements simply raise the bar for success. Not every AI project will justify its capital outlays, so it will be a critical year for non-profitable AI companies as investors will demand clarity that their business models are workable amid rising competition.

Fortunately, our bottom-up analysts are increasingly reporting that AI will boost corporate profitability across sectors. To date, this has mostly been through automation and cost reduction, but gradually creative capabilities that drive revenue generation are also being delivered, as we discussed in our 2026 Outlook.

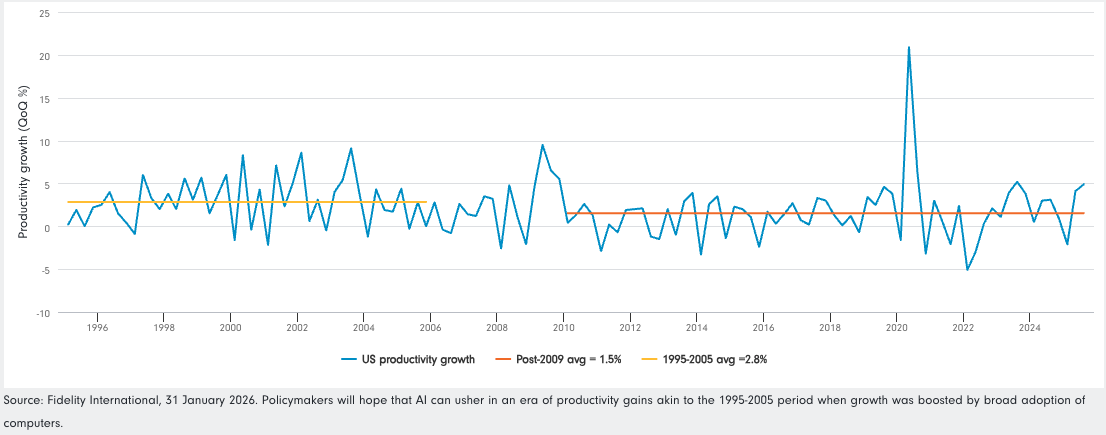

For now, market narratives are swinging between optimism about productivity gains to pessimism about creative destruction. For example, Q325 US productivity data, the fastest in over a decade outside Covid-era distortions and Q323 when source data was revised, catalysed a bout of broad positive performance across potential AI adopters by suggesting that AI is boosting firms’ efficiency. However, indiscriminate sell-offs have also taken place in sectors as diverse as software, logistics, wealth management, law and commercial real estate which are perceived as threatened by AI disruption.

The reality is more complex. Individual businesses have different characteristics, competitive positions, economic moats and cost bases. Some will suffer from disruption, but others will adapt and emerge stronger. Where there are successes, the winners and losers will largely be determined by whether incumbents can adopt AI and increase their effectiveness, or whether they become dependable on (or replaced by) more efficient AI companies. These dynamics will play out differently across industries and geographies.

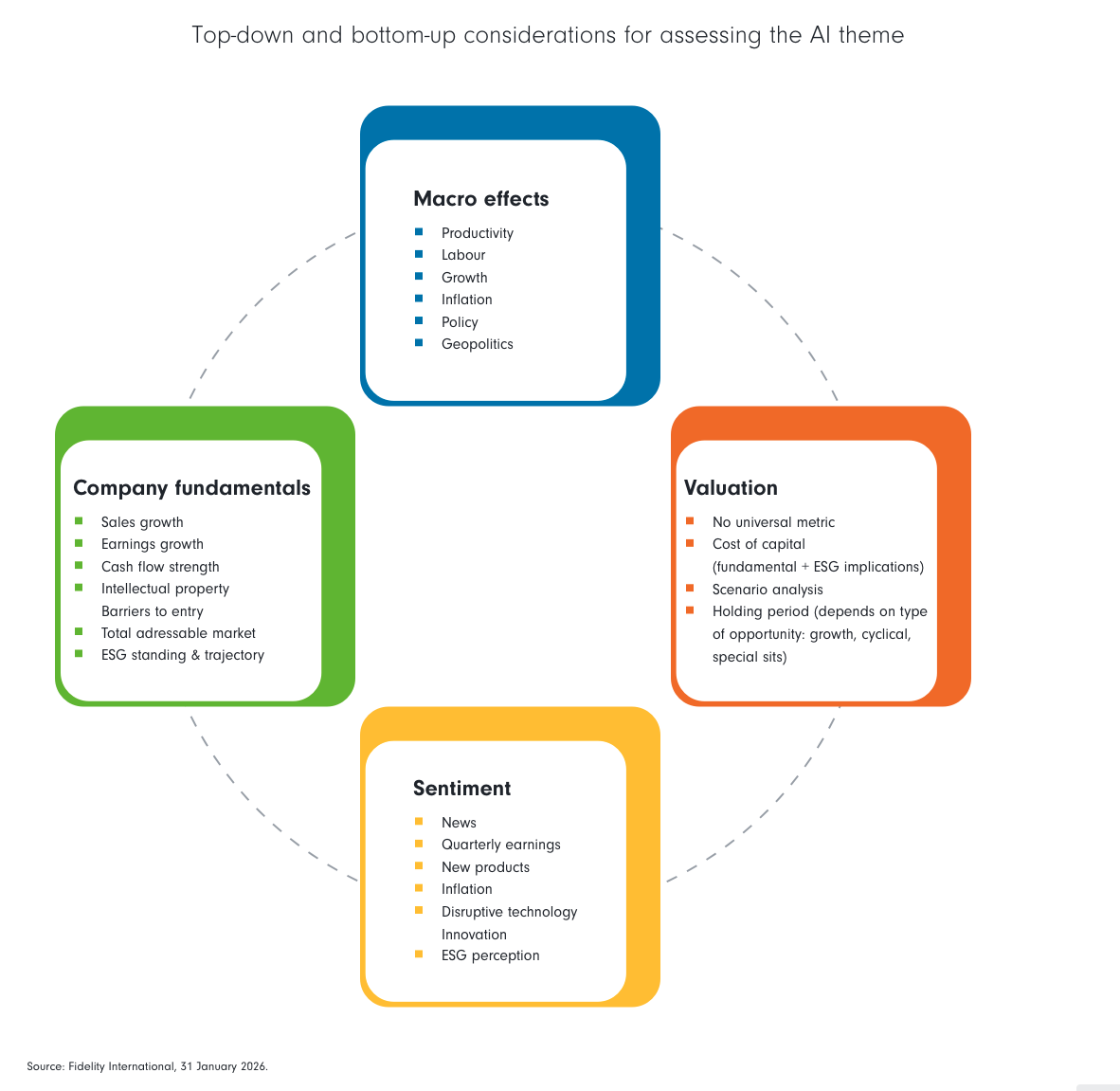

Thematic evolution: Productivity growth accelerates

Either way, exuberance will result in excessive valuations in places as investors chase outsized gains, while fear will leave prices implying an unlikely degree of impairment in others. Any resulting market bifurcation will present both opportunities and risks, the latter including elevated concentration, which increases the importance of certain idiosyncratic stock-level drivers to its overall returns. This comes at a time when AI represents perhaps the greatest threat that some of the largest companies have seen to key business lines, in areas like internet search and advertising. High capex plans also represent a risk to near-term payout ratios, which can be a key determinant of valuations through share buyback activity. Each of these factors challenges the credibility of a capitalisation-weighted approach to equity investment, but they do not warrant disengagement. Rather, a fertile hunting ground has been created for nimble active investors to identify mispricings and deliver alpha through in-depth research.

“In the short run, the stock market is a voting machine. Yet, in the long run, it is a weighing machine.”

Benjamin Graham

AI has the potential to usher in an era of elevated growth by reshaping supply chains, enhancing product design, and creating entirely new markets. By unlocking efficiency gains across industries, it could even deliver a disinflationary growth impulse which might allow more accommodative monetary and fiscal policy. Indeed, this is the hope of Fed Chair nominee Warsh, who has asserted that AI will restrain inflation by boosting productivity, justifying lower interest rates.

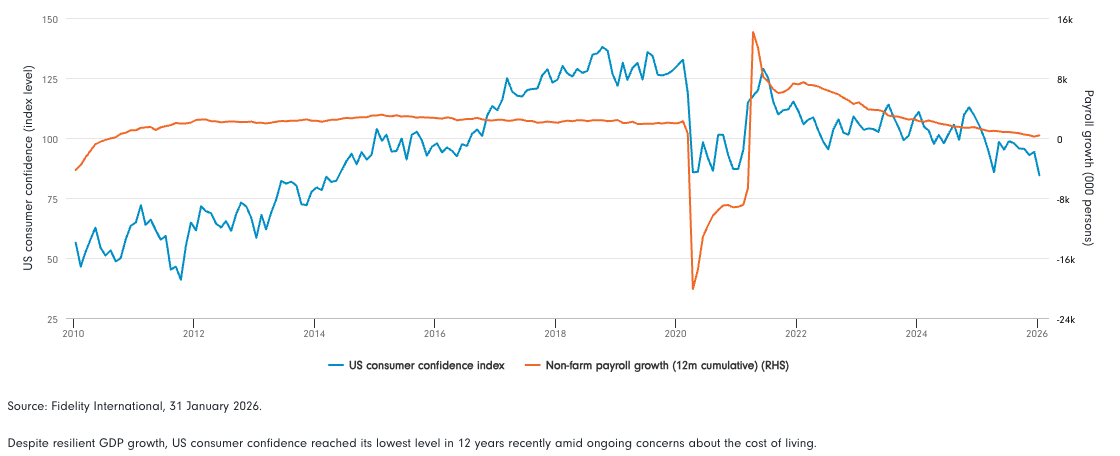

However, given that businesses are deploying AI technologies to save on labour costs, it is also difficult to envisage a scenario where this will not result in any adverse labour market effects. We have already witnessed a few highly publicised instances of corporate layoffs and there are signs of reduced reliance on labour as a factor of production in some industries. AI has been at least partly responsible for the failure of current elevated growth to reflect in stronger employment, even if the primary driver of weaker employment growth may have been lower net migration. Meanwhile, concerns about weak labour market prospects are partly responsible for low US consumer confidence and perceptions of K-shaped economic outcomes, which will be an important factor in November’s mid-term elections.

As consumption represents the lion’s share of economic activity in many economies, the labour-market effects of AI’s proliferation are a risk worth monitoring. For now, there is limited evidence that it is putting large swathes of people out of work, but it is possible that such a scenario will play out over time, especially as wage bills represent low-hanging fruit for ambitious AI disruptors. If labour market weakness begins to outweigh the positive dynamics associated with AI investment and wealth effects from rising corporate profitability, economic trajectories might begin to shift downward.

Under such a scenario, AI capex plans, monetisation timelines and overall value creation would likely be scrutinised more intensely. Moreover, the socioeconomic and political ramifications could be significant. In today’s era of intensifying international competition, such developments could draw protectionist policy reactions, propelling the world more rapidly towards a multi-polar system.

K-Shaped AI economy: Robust growth but gloomy consumer confidence

The US holds a clear early lead in the AI supply chain, although it faces bottlenecks in areas like energy supply and skilled labour. Meanwhile, the rest of the world is playing catch up. In particular, China is scaling its capabilities rapidly, igniting fears of a race between the two superpowers. Once China enters a space, it has historically tended to flood the market with supply and bring down prices and margins. The release of DeepSeek’s open-source AI model in early 2025 highlighted this potential and drove a bout of market volatility by demonstrating that use cases do not necessarily require the most expensive, cutting-edge technology.

Increased supply chain competition would be detrimental to many AI infrastructure companies, but could have positive implications for AI adopters. We note that the benefits from new technologies have historically tended to accrue mostly to those that employ them effectively through higher returns on investment, rather than early-stage innovators that benefit from hype. With this in mind, China might benefit disproportionately in relative terms as it holds some advantages in terms of adoption, including its more open-source approach, state-driven industrial strategy, less stringent data laws, access to raw materials, and abundant energy capacity.