08 Apr 2026

The investment landscape is evolving in ways that challenge long-standing assumptions about the foundations of diversified portfolios. Investors are now reassessing the role of several core exposures, particularly US equities and global bonds. In this perspective, we explore why these questions have arisen and how our portfolios are handling these challenges and delivering long-term outcomes for clients.

For much of the past decade, US equities have been the dominant force in global portfolios. Strong economic growth and technological leadership drove the US market to outperform other regions. Today, that narrative is being tested. A series of macroeconomic and structural shifts have prompted investors to question whether their US equity allocations continue to meet their objectives.

The first challenge is the changing macro backdrop. We still expect the US economy to perform strongly this year, but the balance and type of risks inherent in US equity exposure have shifted. Domestic and foreign policy changes in the US are driving markets to a greater degree than in the past, adding a layer of uncertainty to return and volatility expectations. Meanwhile, inflation in the US remains a key risk. Although lower than its peak, it remains sticky, and the stimulative monetary and fiscal policy that should power the US economy in 2026 could yet cause inflation to take hold again. This uncertainty is compounded by political risk and tariff-related tensions, which threaten corporate profitability and global trade flows.

Equity valuations and high market concentration further cloud the picture. US equity valuations are high both compared to history and other markets, leaving little margin for error should sentiment shift. Meanwhile, a handful of mega-cap technology and AI-focused companies now account for an outsized portion of the US equity market, potentially adding significant single stock and thematic risk to investor portfolios. The runaway performance of US equities over the past decade means global indices are even more dominated by US companies, potentially leaving investors more exposed to a narrow set of drivers than they realise. Active rather than passive exposure is one way investors can mitigate the dangers of overconcentration and high valuations. However, our research indicates that US large-cap equities can be difficult for active managers to outperform in.

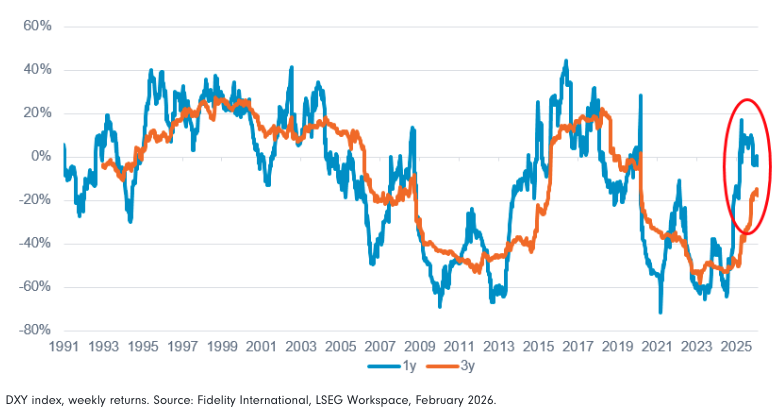

Currency dynamics present another layer of complexity. Over the past 15 years, the dollar has reached historically high levels on a trade-weighted basis, benefiting from its safe-haven status and investor demand for US assets due to strong corporate profits.

However, we believe recent changes to US policy will precipitate a weaker dollar over the medium term, which will act as a drag on US equity returns for non-USD based investors. In addition, questions over the safe-haven status of the dollar could meaningfully alter the risk and diversification characteristics of the portfolios of investors based outside the US, who in the past could rely on currency exposure to curtail US equity losses in risk-off events.

Dollar may not offer as much protection in risk-off episodes for non-USD investors in future

US dollar correlation to S&P 500

These factors combine to create a more fragile environment for US equities than many investors have experienced in recent years. Alongside this, the opportunity cost of investing in US equities has risen with the improving outlook for other regions. Europe is undergoing a significant fiscal expansion, improving corporate earnings momentum and a supportive policy and macro backdrop is raising sentiment in Japan, the outlook for many emerging markets is positive, and optimism around AI is growing in China.

The US equity market has been a significant driver of global returns for many years and still undoubtably has many favourable characteristics. However, we believe that the expected risk-reward profile of US equities is less straightforward than in the past. Investors are beginning to ask whether a more considered approach, incorporating other regions and asset classes, might offer better resilience to prevailing macro and market trends.

We manage two multi asset risk-rated ranges with very different goals. Diversification is a central feature of both, but they are designed to take differing approaches to questions about the changing characteristics of US equities.

In the Multi Asset Open range, we use a highly dynamic approach with the flexibility to adjust the portfolios to take advantage of tactical opportunities. We therefore have the option to tilt away from US equities when we believe risks are rising or opportunities elsewhere are more compelling. In contrast, the Multi Asset Allocator range is designed as a low-cost, strategic solution that maintains consistent exposure to global markets through a passively implemented long-term asset allocation framework. The portfolios are rebalanced regularly, but their goal is to provide stable, diversified exposure that has been proven to deliver long term returns.

In the Open range, we have responded to rising concentration and valuation risks in US equities not only by reducing exposures but also by actively broadening regional exposure and adjusting how equity risk is expressed. We are allocating more capital to emerging markets where domestic demand, policy support and improving earnings momentum offer differentiated return drivers. Countries such as India, China, and South Africa stand out, supported by structural reform, favourable demographics or commodity linkages. These markets also benefit from a softer US dollar environment, which we believe is likely over the medium term.

We continue to hold exposure to technology and AI-related themes, but we are increasingly selective about how that exposure is expressed. Rather than concentrating risk in a small number of US mega-cap stocks, we are diversifying across the global value chain, including Asian hardware manufacturers, European industrials, and emerging market suppliers that stand to benefit from global capex without carrying the same valuation risk. This approach allows us to participate in long-term growth while reducing concentration risk. Diversification also extends beyond equities. Gold plays an important role in our portfolios as a hedge against macro uncertainty, policy error and geopolitical risk, all of which have the potential to undermine highly valued equity markets. We complement this with absolute return strategies and exposure to more defensive equity sectors, which could help dampen portfolio drawdowns if sentiment around US equities turns.

For investors in the Allocator range, the objective is different. Allocator is not designed to time markets or rotate aggressively between regions. Instead, its strength lies in providing broad, diversified exposure to global equities that reflects the long-term opportunity set rather than short-term views. While US equities remain a significant component of global markets, Allocator portfolios are structurally diversified across regions, styles, and market capitalisations, including meaningful exposure to emerging markets, global small caps, and real estate. This diversification helps mitigate concentration risk over time without relying on tactical decisions.

The disciplined rebalancing process is a key advantage of the Allocator range. By rebalancing regularly back to strategic asset allocations, portfolios naturally trim areas that have performed strongly after periods of outperformance, including US equities, and reinvest into areas that have lagged. This systematic approach helps manage unintended concentration and supports long-term risk-adjusted returns, while keeping costs low and outcomes transparent.

Overall, we believe that US equities remain a key source of growth in portfolios, but the need for appropriate diversification is more important than ever. This is reflected in the Allocator range via a robust, globally diversified core holding that captures long-term growth efficiently, while in the Open range, we have the flexibility to pursue a more dynamic approach to managing our US equity exposure.

For decades, bonds have been regarded as the anchor of diversified portfolios, providing stability and income while offsetting equity risk. However, bonds have been a less reliable source of protection in recent years, leaving some investors questioning whether their portfolios are as resilient as they once were.

The traditional diversification benefits of bonds have evolved in recent years. Historically, government bonds tended to rally when equities sold off, cushioning portfolios during periods of stress. However, the inflation shock that followed the pandemic disrupted this relationship. Rising prices and the subsequent aggressive rate hikes caused bonds and equities to fall together in 2022, undermining a key feature of the classic 60/40 portfolio model. Although correlations have eased somewhat now, they are likely to remain volatile, potentially making bonds less predictable as a defensive asset in future.

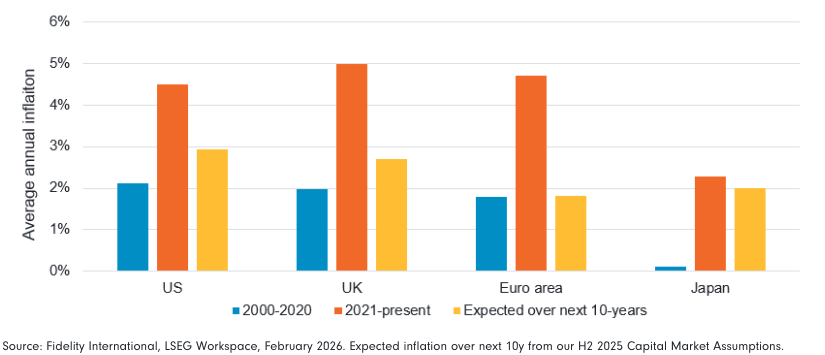

Inflation remains a central concern. Although headline rates have declined, underlying pressures persist, making the path for interest rates less certain. This volatility translates into greater price swings for bonds, particularly at longer maturities, meaning duration could be a larger source of risk in the future than in the past.

Inflation likely to be higher and more volatile in future than in the 2000s and 2010s

Credit markets pose their own challenges. Spreads in investment grade and high yield bonds are very tight, offering limited compensation for risk and lowering expected future returns. At the same time, corporate balance sheets face pressure from higher refinancing costs, raising questions about future default rates.

There are also structural factors at play. Persistent fiscal deficits and politicised capital flows are reshaping the behaviour of sovereign bond markets. Scale of government borrowing has implications for yields and liquidity, while regulatory changes influence demand patterns among institutional investors.

This is not that say that bonds do not still have an important role to play in portfolios. However, recent developments have posed questions over whether they will continue to provide the same level of protection they once did. The challenge is to adapt to a world where fixed income remains important, but its role is more nuanced and requires more thought than in the past.

In the Multi Asset Open range, we can tactically adjust fixed income exposure as the macro environment evolves. In contrast, in the Multi Asset Allocator range bonds play a more structural role within a long-term strategic asset allocation that prioritises stability, diversification and cost efficiency.

Within the Open range, we have become more selective in how we use bonds as a defensive tool. Higher inflation volatility, fiscal pressures, and greater interest rate uncertainty mean that traditional duration exposure may not always provide reliable protection. As a result, we actively vary duration, favour flexible and unconstrained bond strategies, and complement core fixed income with credit, emerging market debt, and alternative sources of defence such as gold and absolute return strategies.

The flexibility of the Open range also allows us to separate the objectives of return generation and portfolio protection more clearly. Rather than relying on government bonds alone to deliver both, we can allocate to assets that offer attractive carry when spreads are supportive, while using derivatives and liquid alternatives to manage downside risk. This approach recognises that correlations can change quickly in stressed environments.

The Allocator range, by contrast, is built to deliver dependable diversification rather than tactical defence. Return objectives are set over a medium- to long-term horizon (5+ years), meaning the range is built for resilience across many macro environments, not just the current one. Persistently positive equity-bond correlations are not typical over longer horizons, they tend to fluctuate with the prevailing macro regime, and bonds can still offset some equity risk even when correlations are elevated. Therefore, global government and corporate bonds remain core components because of their long-term defensive role in dampening portfolio volatility across market cycles. While bonds may not protect portfolios in every short-term shock, their inclusion within a diversified, risk-rated structure remains an effective way to balance growth assets over time.

A key strength of the Allocator range is its disciplined construction. The strategic asset allocation is informed by long-term capital market assumptions and is designed to blend growth and defensive assets in proportions that align with each risk profile. Regular rebalancing ensures that portfolios do not drift into excessive risk, particularly after periods of equity strength or bond weakness. This systematic approach helps maintain the intended risk characteristics without relying on discretionary judgement.

Cost and transparency are also central to the Allocator proposition. Passive implementation allows investors to access global bond markets efficiently, while rigorous index and vehicle selection helps ensure exposures behave as expected. For many investors, this simplicity and predictability are valuable features, particularly when markets are volatile.

While we acknowledge that the defensive characteristics of bonds are more nuanced than in the past, we believe they remain an important building block within a diversified portfolio. The Open range allows us to adapt defensiveness actively and combine bonds with a broader set of protective tools, while the Allocator range provides a stable, low-cost foundation that continues to serve its purpose over the long term.

Important information

This material is for Institutional Investors and Investment Professionals only, and should not be distributed to the general public or be relied upon by private investors.

This material is provided for information purposes only and is intended only for the person or entity to which it is sent. It must not be reproduced or circulated to any other party without prior permission of Fidelity.

This material does not constitute a distribution, an offer or solicitation to engage the investment management services of Fidelity, or an offer to buy or sell or the solicitation of any offer to buy or sell any securities in any jurisdiction or country where such distribution or offer is not authorised or would be contrary to local laws or regulations. Fidelity makes no representations that the contents are appropriate for use in all locations or that the transactions or services discussed are available or appropriate for sale or use in all jurisdictions or countries or by all investors or counterparties.

This communication is not directed at, and must not be acted on by persons inside the United States. All persons and entities accessing the information do so on their own initiative and are responsible for compliance with applicable local laws and regulations and should consult their professional advisers. This material may contain materials from third-parties which are supplied by companies that are not affiliated with any Fidelity entity (Third-Party Content). Fidelity has not been involved in the preparation, adoption or editing of such third-party materials and does not explicitly or implicitly endorse or approve such content. Fidelity International is not responsible for any errors or omissions relating to specific information provided by third parties.

Fidelity International refers to the group of companies which form the global investment management organization that provides products and services in designated jurisdictions outside of North America. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. Fidelity only offers information on products and services and does not provide investment advice based on individual circumstances, other than when specifically stipulated by an appropriately authorised firm, in a formal communication with the client.

Europe: Issued by FIL Pensions Management (authorised and regulated by the Financial Conduct Authority in UK), FIL (Luxembourg) S.A. (authorised and supervised by the CSSF, Commission de Surveillance du Secteur Financier), FIL Gestion (authorised and supervised by the AMF (Autorité des Marchés Financiers) N°GP03-004, 21 Avenue Kléber, 75016 Paris) and FIL Investment Switzerland AG.

For information purposes only. Neither FIL Limited nor any member within the Fidelity Group is licensed to carry out fund management activities in Brunei, Indonesia, Malaysia, Thailand and Philippines.

This fund uses financial derivative instruments for investment purposes, which may expose the fund to a higher degree of risk and can cause investments to experience larger than average price fluctuations.

ISG6323