01 Apr 2026

Japanese Government Bond yields sharply sold off at the long end following Sanae Takaichi’s landslide victory in the recent Japanese snap election, strengthening her mandate to pursue fiscal expansion. Mike Riddell, Portfolio Manager of the Fidelity Strategic Bond Fund, discusses the potential implications for global fixed income markets - should policy shift further. He also sets out his assessment of the broader macroeconomic backdrop and where he currently sees the main drivers of alpha within the strategy.

Japan’s Prime Minister Sanae Takaichi now has clear political capital to pursue an expansionary fiscal agenda, centred on reducing the sales tax and increasing defence expenditure, which has prompted investors to reassess Japan’s sovereign supply outlook and inflation trajectory. The rise in long dated Japanese yields reflects that shift in expectations, and any acceleration in policy implementation could likely place further upward pressure on global bond markets.

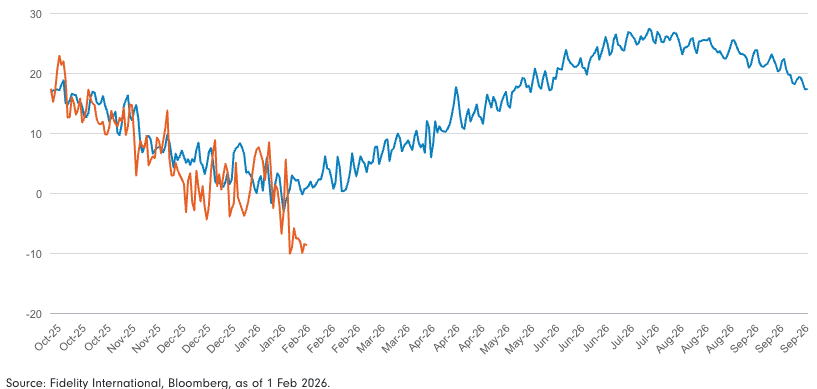

Elsewhere, in the US, recent extreme cold weather is likely to weigh on near term activity, which should become evident in upcoming data releases. Meanwhile in the UK, political uncertainty and concerns over a potential leadership change have unsettled investors and driven weakness at the long end as investors demanded a higher term premium.

Chart of the month

US cold snap likely to cool US economic activity

Overall, we are running an overweight duration position relative to the benchmark, with the fund around 1.7 years longer.

This exposure comes from a combination of Emerging Market Local Currency rates and some selected developed market exposure in Norway, Australia and the UK.

In terms of underweights, we are avoiding duration exposure in Eurozone, Poland and Japanese rates.

We see structural issues with a long US duration position but given recent weather developments we have tactically reduced our underweight, expecting rates to rally as weaker economic data comes out.

One of our long-term duration convictions is a preference for EM markets, where real yields are much more attractive.

We have long exposure to UK and US inflation markets while inflation protection looks cheap, and geopolitics threatens increased pressure on prices.

Two-year forward inflation expectations fell at the end of 2025 but sharply rose in 2026 amid geopolitical volatility. We have used this rally in inflation expectations (which is good for our long exposure) to reduce some risk.

Our core view on inflation is that the market implied risk of inflation rising in the UK and the US is too low, so buying inflation protection is relatively cheap.

In the US, GDP growth is very strong, the Fed is likely to keep cutting rates and tariffs are being imposed on a wide range of imports – all of these factors are likely to add inflationary pressure.

EM currencies remain historically cheap versus developed markets (DM) on a trade-weighted basis, so we prefer to have exposure here. On the other hand, US Dollar (USD) is still historically expensive despite last year’s selloff, so we have some short exposure here.

We have had short USD exposure for over a year, but recently we have taken some profits here, but may look to re-engage if we see an attractive entry point.

Our largest short position is in the British Pound while it trades at pre-Brexit levels on a trade-weighted basis and as political uncertainty has the potential to hurt the Sterling.

Japan’s new fiscal regime is likely to hurt confidence in the Yen while the PM is happy to continue devaluing the currency. Therefore, we have short exposure in JPY.

We maintain an outright short position in credit via CDX US High Yield and iTraxx Crossover instruments.

Short positioning via these indices has proven to be an efficient way to express our credit views, benefiting from the relatively low cost of index protection and the consistent liquidity advantages these instruments offer.

Credit spreads remain around historical tights, leaving limited room for further spread compression. At these levels, we are conscious of the clear asymmetry of payoffs and feel this downside risk warrants caution around credit exposure.

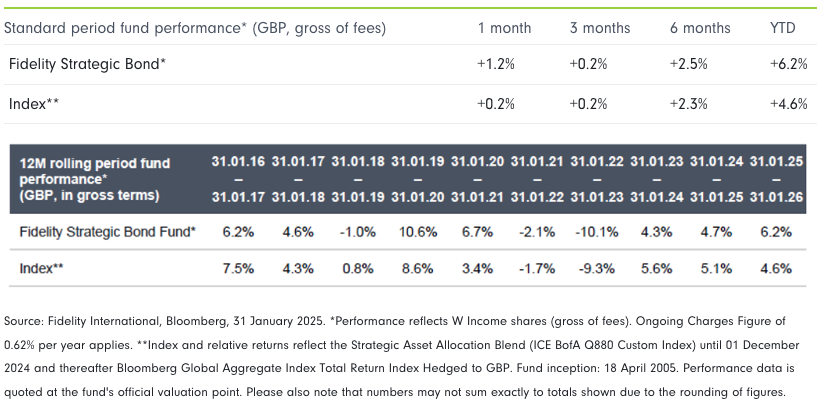

In January 2026, the fund delivered +1.1% gross returns compared with +0.1% for the benchmark, generating 1.0% of alpha over the month. This strong performance reflected long positioning in EM rates and US inflation markets.

Rates: Positioning in rates markets contributed to performance, mainly due to our long exposure in EM local currency rates. Relatively high real rates across Latin American countries like Brazil, Mexico and Colombia provide an attractive valuation point for duration exposure, where we expect to capitalise on more central bank rate cuts as well as the ongoing carry from high real yields in local currency debt markets.

Inflation: Our long inflation positions in both the US and UK contributed to performance in January as markets reversed moves seen in December 2025 due to ongoing geopolitical tensions spiking fears of inflation rising. Particularly in the Middle East, conflict could have considerable impacts on oil and trade, both of which would put pressure on global supply chains.

Currencies: Currency positioning also contributed to performance. Long positions in EM FX performed well, including BRL, MXN, CLP and COP as emerging markets benefited from a rally in commodity prices and broader USD weakness. We are largely long of EM FX versus USD, so this particular trend has worked well as the global economy increasingly looks to diversify from USD. Our long NOK exposure also aided returns as the country’s currency rallied along with oil prices. Our short GBP positioning detracted slightly as in January the Pound posted modest positive returns.

Credit: Our short exposure to credit detracted slightly, as credit spreads continued to tighten. Nonetheless, we view this positioning as asymmetrically attractive, given that volatility remains low and limited spread widening is priced in. The potential upside from a risk-off episode or widening in credit spreads could be significant.

Past performance does not predict future returns

Important information

This information is for investment professionals only and should not be relied upon by private investors. Past performance is not a reliable indicator of future returns. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of investments in overseas markets. Fidelity’s range of fixed income funds can use financial derivative instruments for investment purposes, which may expose them to a higher degree of risk and can cause investments to experience larger than average price fluctuations. The value of bonds is influenced by movements in interest rates and bond yields. If interest rates and so bond yields rise, bond prices tend to fall, and vice versa. The price of bonds with a longer lifetime until maturity is generally more sensitive to interest rate movements than those with a shorter lifetime to maturity. The risk of default is based on the issuers ability to make interest payments and to repay the loan at maturity. Default risk may therefore vary between government issuers as well as between different corporate issuers. Due to the greater possibility of default, an investment in a corporate bond is generally less secure than an investment in government bonds. Reference in this document to specific securities should not be interpreted as a recommendation to buy or sell these securities and is only included for illustration purposes.

UK: The Key Investor Information Document (KIID) is available in English and can be obtained from our website at www.fidelityinternational.com. The Prospectus may also be obtained from Fidelity. Issued by FIL Pensions Management. Authorised and regulated by the Financial Conduct Authority.

FIPM: 9909

Authors:

Mike Riddell

Tim Foster

Ravin Seeneevassen