05 Apr 2026

The Supreme Court struck down President Trump’s 2025 sweeping global tariffs in a 6-3 ruling on Friday. The decision covers all of the country-wide reciprocal tariffs in the International Emergency Economics Power Act (IEEPA), including the fentanyl tariffs on China, and the border emergency tariffs on Canada and Mexico. Other measures, including pre-existing tariffs on China and sectoral tariffs on the likes of steel, aluminium, and autos, remain in place.

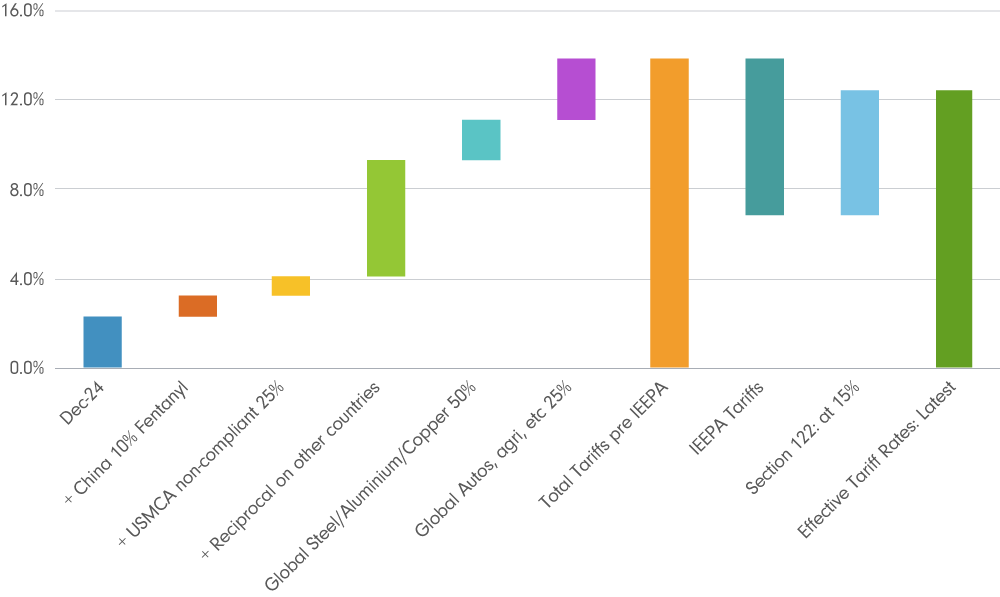

As anticipated, the administration moved quickly to invoke Section 122, which allows a 10 per cent temporary tariff on all countries but which President Trump has said on social media would be set at 15 per cent for all countries for up to 150 days. The untested law requires congressional approval for anything beyond that timeframe. The measure applies to goods shipped after tomorrow (24th February) or received by importers after Friday (February 28th) and replaces nearly 80 per cent of the IEEPA tariffs. Based on prior guidance from US officials, the administration is likely to reconstruct the previous tariff architecture through alternative measures. In essence, and notwithstanding additional legal and administrative hurdles, the IEEPA ruling does little to disrupt the current trade policy. Tariffs are here to stay.

That said, there is a modest appeasement of the policies, at least in the near term until the prior structures get rebuilt. As per our estimates, the combination of the IEEPA ruling and the new 15 per cent Section 122 tariff lowers the effective tariff rate (ETR) by about 1.5 percentage points to 12.4 per cent. We are still reviewing the exemptions outlined in the executive order but currently assume they broadly mirror those under IEEPA.

This paints a relatively benign outcome in the near term. If sustained, these levels would lower our inflation forecast by roughly 10-15 basis points and cut customs revenues by around USD $40-50 billion per annum. Consequently, the reduction in tariff drag should provide a modest lift to growth and a corresponding deterioration in fiscal deficit by around 0.1 per cent of GDP, all things being equal.

But Section 122 is only a temporary measure. After the 150-day window expires, there is considerable uncertainty around the rebuilding of the tariff wall (likely through new implementation of Sections 301 and 302 of the US Trade Act which relate to countries and sectors respectively). We expect the effective tariff rate to settle in the 12-14 per cent range although the composition is likely to remain in flux.

A larger one-time macro effect may stem from refunds of previously collected IEEPA tariffs, which we estimate at more than $150bn as of January 2026. The Supreme Court ruling did not explicitly address this issue, but the Court of International Trade (CIT) could begin adjudicating claims. Nearly 1000 companies have filed suit for refunds (comprising some 50-70 per cent of the tariff value) and this number could increase further in coming days. A full recoup of IEEPA tariff costs by corporates, assuming they absorbed the burden, would lift corporate cash flow and profits by around 0.5 per cent of GDP, with a corresponding one-off hit to government revenues and the fiscal deficit. Legal and bureaucratic delays are likely to make the process more protracted, however.

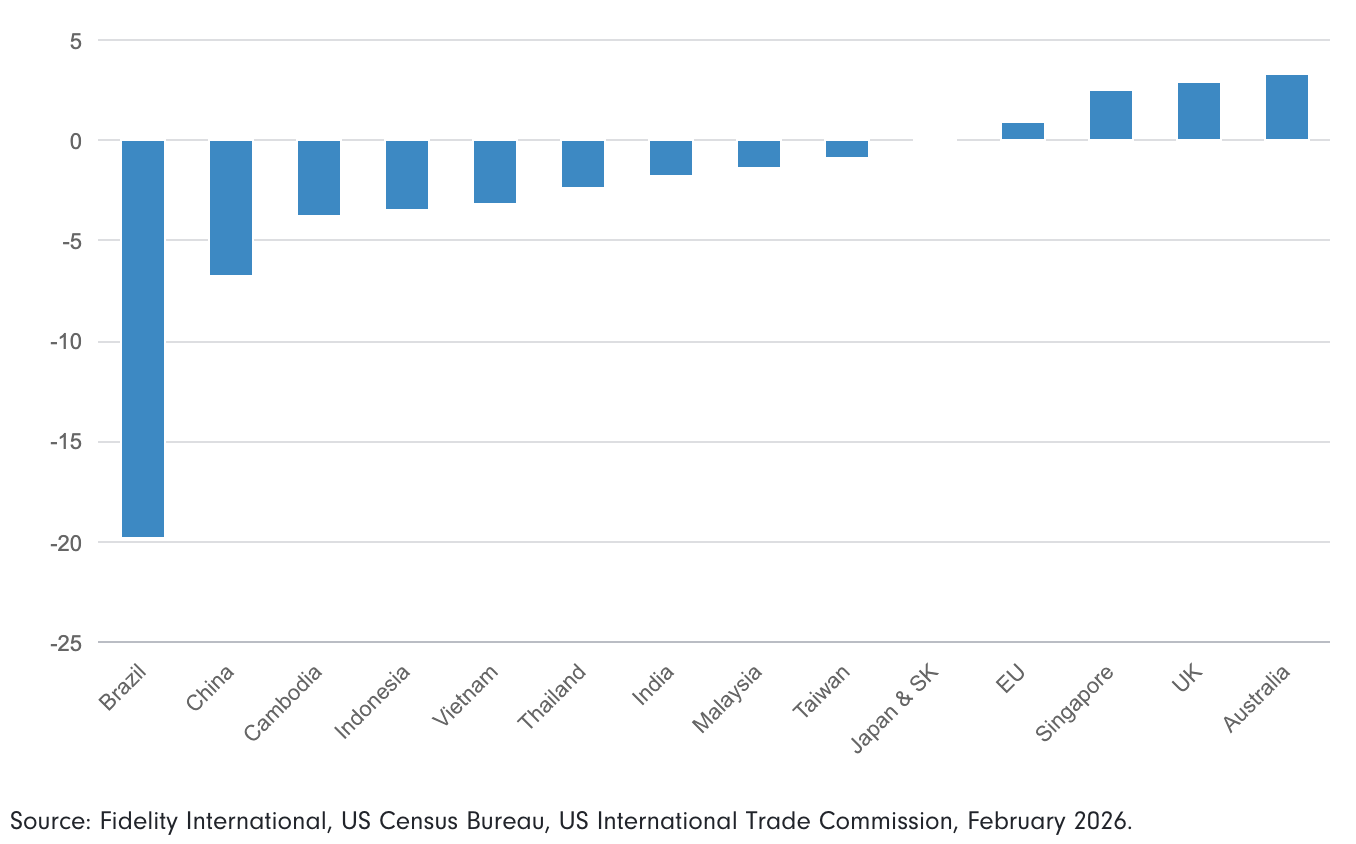

From a country level-perspective, the clear winners from the IEEPA ruling include Brazil, China, Cambodia, and Indonesia. Countries such as the EU, Australia, UK, and other smaller nations that had a 10 per cent existing tariff rate lose ground. Notably, there is not yet any formal documentation supporting President Trump’s post about raising the Section 122 tariffs to 15 per cent. It should be straightforward for the administration to retain 10 per cent for smaller economies, particularly allies such as the UK and Australia that negotiated a deal, while applying 15 per cent more broadly elsewhere. This creates downside risk to our current effective tariff rate estimate of 12.5 per cent. If a revised order applies 15 per cent only to a subset of countries, the aggregate rate would move lower.

China: China is a relative near-term beneficiary of the IEEPA rollback and shift to a temporary 15 per cent Section 122 regime, with estimates suggesting its average tariff burden declines by some 7 percentage points. This reduces immediate escalation risk ahead of the Trump–Xi meeting scheduled for the end of March. However, follow-up actions remain likely, and broader tensions over export controls, supply chains and technology persist.

Japan, Korea, Taiwan: The potential interim 15 per cent flat regime is broadly neutral although these countries have committed sizable US investment pledges (Japan $550bn; Korea $350bn; Taiwan $250bn). Sectoral exposure - autos, semiconductors, steel, and aluminium - leaves them vulnerable to renewed policies. However, given their strategic alignment with the US, these countries are likely to be given exemptions and will stick with existing commitments.

Asean: Effects are mixed. Economies previously facing higher country-specific rates – Indonesia and Malaysia, for example - see relative relief under a uniform 15 per cent structure. Those closer to the prior baseline, such as Singapore, face a modest increase. The narrower tariff differential with China may reduce transshipment incentives and test export competitiveness.

Market reaction to the announcement was modest as the decision was widely expected. US equities edged higher on improved risk backdrop, while bonds sold off marginally, reflecting fiscal concerns. The dollar remains under pressure given the elevated policy uncertainty and we await more clarity on the rebuilding of tariff walls and IEEPA refunds process.

Asian equities were broadly in the green on Monday morning with relative outperformance in Hong Kong, Indonesian, and Indian equities. China markets remained shut for the Lunar New Year holidays but we expect the tactical outperformance to continue once markets reopen. In the near term, the backdrop for Asian equities looks constructive. Tariff rates are easing at the margin and expectations of relative stability in the run-up to the Trump-Xi meeting are supportive. However, greater clarity is needed on the rebuilding of tariff walls and the IEEPA refund process before medium-term winners and losers emerge. We are also closely monitoring geopolitical risks, particularly around Iran, alongside the ongoing rotation within equity markets. In this environment, we continue to advocate diversification in portfolio construction.

Important Information

This material is for Institutional Investors and Investment Professionals only, and should not be distributed to the general public or be relied upon by private investors.

This material is provided for information purposes only and is intended only for the person or entity to which it is sent. It must not be reproduced or circulated to any other party without prior permission of Fidelity.

This material does not constitute a distribution, an offer or solicitation to engage the investment management services of Fidelity, or an offer to buy or sell or the solicitation of any offer to buy or sell any securities in any jurisdiction or country where such distribution or offer is not authorised or would be contrary to local laws or regulations. Fidelity makes no representations that the contents are appropriate for use in all locations or that the transactions or services discussed are available or appropriate for sale or use in all jurisdictions or countries or by all investors or counterparties.

This communication is not directed at, and must not be acted on by persons inside the United States. All persons and entities accessing the information do so on their own initiative and are responsible for compliance with applicable local laws and regulations and should consult their professional advisers. This material may contain materials from third-parties which are supplied by companies that are not affiliated with any Fidelity entity (Third-Party Content). Fidelity has not been involved in the preparation, adoption or editing of such third-party materials and does not explicitly or implicitly endorse or approve such content. Fidelity International is not responsible for any errors or omissions relating to specific information provided by third parties.

Fidelity International refers to the group of companies which form the global investment management organization that provides products and services in designated jurisdictions outside of North America. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. Fidelity only offers information on products and services and does not provide investment advice based on individual circumstances, other than when specifically stipulated by an appropriately authorised firm, in a formal communication with the client.

Europe: Issued by FIL Pensions Management (authorised and regulated by the Financial Conduct Authority in UK), FIL (Luxembourg) S.A. (authorised and supervised by the CSSF, Commission de Surveillance du Secteur Financier), FIL Gestion (authorised and supervised by the AMF (Autorité des Marchés Financiers) N°GP03-004, 21 Avenue Kléber, 75016 Paris) and FIL Investment Switzerland AG.

UAE: The DIFC branch of FIL Distributors International Limited is regulated by the DFSA for the provision of Arranging Deals in Investments only. All communications and services are directed at Professional Clients and Market Counterparties only. Persons other than Professional Clients and Market Counterparties, such as Retail Clients, are NOT the intended recipients of our communications or services. The branch is established pursuant to the DIFC Companies Law, with registration number CL2923, as a branch of FIL Distributors International Limited, registered in Bermuda. FIL Distributors International Limited is licensed to conduct investment business by the Bermuda Monetary Authority.

In Hong Kong, this material is issued by FIL Investment Management (Hong Kong) Limited and it has not been reviewed by the Securities and Future Commission.

FIL Investment Management (Singapore) Limited (Co. Reg. No: 199006300E) is the legal representative of Fidelity International in Singapore. This document / advertisement has not been reviewed by the Monetary Authority of Singapore.

In Taiwan, Independently operated by Fidelity Securities Investment Trust Co. (Taiwan) Limited 11F, No.68, Zhongxiao East Road, Section 5, Taipei 110, Taiwan, R.O.C. Customer Service Number: 0800-00-9911.

In Korea, this material is issued by FIL Asset Management (Korea) Limited. This material has not been reviewed by the Financial Supervisory Service, and is intended for the general information of institutional and professional investors only to which it is sent.

Issued in Japan, this material is prepared by FIL Investments (Japan) Limited (hereafter called “FIJ”) based on reliable data, but FIJ is not held liable for its accuracy or completeness. Information in this material is good for the date and time of preparation, and is subject to change without prior notice depending on the market environments and other conditions. All rights concerning this material except quotations are held by FIJ, and should by no means be used or copied partially or wholly for any purpose without permission. This material aims at providing information for your reference only but does not aim to recommend or solicit funds /securities.

For information purposes only. Neither FIL Limited nor any member within the Fidelity Group is licensed to carry out fund management activities in Brunei, Indonesia, Malaysia, Thailand and Philippines.

FIL Investment Management (Australia) Limited (ABN 34 006 773 575, AFSL No. 237865) and FIL Responsible Entity (Australia) Limited (ABN 33 148 059 009, AFSL No. 409340) are the legal representatives of Fidelity International in Australia. This is intended as general information for a person who is a 'wholesale client' under section 761G of the Corporations Act 2001 (Cth) and has been prepared without taking into account any person’s objectives, financial situation or needs. Not for distribution to or use by retail clients.

GCT250248GLO

Ashray Ohri is a Macro Strategist in Fidelity’s Global Macro & Strategic Asset Allocation team. He joined Fidelity in 2022 and is based in Hong Kong. Prior to Fidelity, Ashray worked as an Economist at ICICI Bank and DMI Finance. He holds a Master’s degree in Economics from the Delhi School of Economics and a Bachelor’s degree (Hons) in Economics from the University of Delhi.

Peiqian Liu is the Asia Economist in Fidelity’s Global Macro & Strategic Asset Allocation team. Based in Singapore, Peiqian leads our Asia-focused macroeconomic research. She brings her deep experience in economist roles across the industry, including at Commerzbank and SEB AB, as well as most recently at NatWest Markets where she was Chief China Economist. Peiqian obtained a Bacholor Degree (with Honours) in Economics from Nanyang Technological University, Singapore, in 2013.