09 Apr 2026

Marcel Stötzel, Co-Portfolio Manager of the Fidelity European Fund and Fidelity European Trust PLC, explores the structural changes driving a stronger backdrop for Europe. He outlines why a disciplined, quality‑focused investment approach is key to capturing opportunities emerging across the region.

Our investment process is anchored in three core philosophies that guide portfolio construction and management. Firstly, we employ a bottom-up stock picking approach, with the aim that the majority of the portfolio’s risk and return is driven by stock selection rather than macro factors, sector allocation or currency positioning.

Secondly, we maintain a long-term perspective, typically holding positions for three to five years. This approach aligns with our expertise and reduces transaction costs, which is crucial as excessive trading consistently erodes returns in asset management.

Finally, we prioritise capital preservation through three key mechanisms: maintaining sector exposures within ±5% bands relative to the benchmark, running an ungeared portfolio beta consistently below 1.0, and focusing rigorously on downside scenarios for individual holdings before considering upside potential.

Our investment process focuses on companies that consistently grow their dividends, as our research shows that these companies significantly outperform those that cut or merely maintain their dividends. We focus on businesses that exhibit strong fundamentals: disciplined capital allocation, structural growth drivers, cash generation capabilities and robust balance sheets.

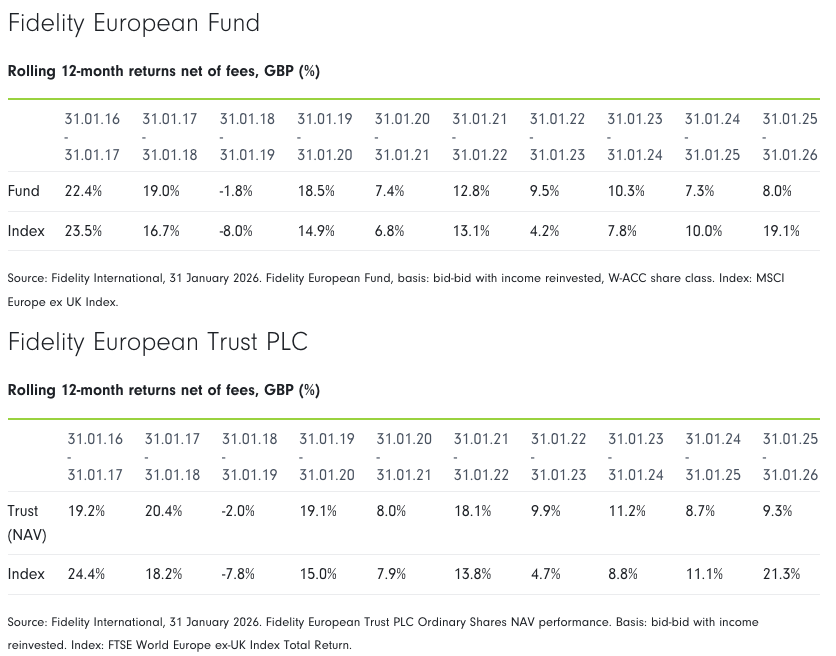

Long‑term performance remains aligned with the strategy’s objective of delivering 1-2% annual outperformance net of fees, while maintaining a cautious risk profile designed to protect on the downside. Historically, the strategy has performed particularly well in weak markets, outperforming in all major down years and more than 70% of down months. However, the most recent period has posed headwinds. The recent market strength has been characterised by sharp, value-led rallies similar to the environment following the Covid vaccine announcements in late 2020. Typically, such rapid, cyclically-driven bull markets have tended to be challenging for us to keep pace.

Part of the recent underperformance stemmed from a handful of stock‑specific disappointments after many years of strong stock selection. Names such as Novo Nordisk, Symrise and Dassault Systèmes detracted.

Beyond that, lack of exposure to defence stocks was a drag on performance. We have deep experience analysing the sector, and defence companies have historically displayed weak capital discipline and inconsistent execution, making them less attractive. German defence names in particular rerated extremely quickly, leaving little opportunity to build positions at valuations that aligned with our disciplined approach.

Our long‑term underweight to Germany also detracted. The portfolio is broadly aligned with the domestic German recovery story, holding positions such as Deutsche Börse and SAP. What we did not own were the large global industrial names within the DAX that have little domestic exposure but nevertheless rerated strongly.

We remain underweight in peripheral banks. Our exposure has largely favoured continental European institutions, a position that has been a relative drag given the strong performance of peripheral economies and their banks. This was not a deliberate strategic stance, but the result of bottom‑up stock selection. We do, however, hold names such as Intesa Sanpaolo and Bankinter, which have performed well, and we expect to continue to do so.

Finally, rising long‑term interest rates have created a difficult backdrop for quality stocks more broadly, as companies with stable growth and strong balance sheets lagged sharply. While this environment was challenging, we do not expect the same rate‑driven headwinds to persist at the magnitude seen over the last few years.

Past performance does not predict future returns. The fund’s returns may increase or decrease as a result of currency fluctuations.

The portfolio remains fundamentally defensive in construction. Beta remains below 1.0, reflecting the focus on companies with strong balance sheets, steady cash generation and the ability to grow dividends sustainably. Even within more cyclical sectors, we are focused on businesses offering the greatest resilience.

Recent positioning changes reflect both valuation opportunities and growing optimism towards the European economic backdrop. We have increased exposure to domestic Europe, adding positions in companies such as Ryanair and Inditex. Both names provide access to improving consumer dynamics across the region.

We exited Sanofi following concerns about US policy impacts on vaccines and challenges within the pipeline. A more notable shift was the move from LVMH to Richemont within the luxury sector. While LVMH has been a longstanding holding, the company’s aggressive post‑Covid pricing strategy risked alienating both aspirational and high‑net‑worth customers. Richemont, with its focus on hard luxury, offers what we consider as a more attractive long‑term position.

We are growing increasingly optimistic about Europe’s prospects. Several structural developments that once seemed unlikely have begun to materialise, including substantially higher defence spending across the continent and the lifting of Germany’s fiscal brake. These shifts suggest political willingness to address long‑standing constraints on growth and competitiveness.

We believe further positive developments are now more possible, such as tighter Europe-wide integration and reducing red tape, allowing for more pro‑business regulatory frameworks. Another significant opportunity lies in mobilising Europe’s high household savings rate. European households save more than their US counterparts but invest disproportionately in unproductive assets such as fixed deposits and life insurance products. Even modest progress in redirecting these savings into the real economy could act as a long‑term structural tailwind.

Overall, while the last year has been testing, the strategy remains grounded in the same principles that have driven strong long‑term outcomes: bottom-up stock selection, a long-term perspective and a focus on capital preservation. With growing signs of structural improvement across Europe, we see reason to be optimistic as we look ahead.