25 Jan 2019

A decade after the global financial crisis peaked in 2008, financial markets have only just begun to correct the asset price distortions that were created by the US Federal Reserve’s (Fed’s) massive quantitative easing (QE) program. QE was originally deployed to stabilize financial markets during the crisis, but instead of being a limited intervention to restore markets over a few years, it expanded and became an ongoing endeavour. It succeeded in pushing down bond yields and pushing up asset prices, steering many investors toward riskier assets while also keeping the costs of capital artificially suppressed. But continuous QE also led to ongoing price distortions in bonds and equities, while incentivizing leverage and rewarding complacency among investors who appeared to view persistently low yields and the Fed’s “buyer of last resort” role as a permanent arrangement.

However, those conditions are neither normal nor permanent, in our view, and we expect the reversal of QE to have significant impacts on bond and equity markets alike in the upcoming year. Just this past fall (October 2018), we saw bond and equity markets in the US decline concurrently as rates rose. That may seem anomalous, but because bonds and equities were equally propped up by Fed intervention, they have been equally vulnerable to the opposite effect as Fed policy unwinds. These are the types of valuation corrections we expect to see as the artificial effects of prolonged monetary accommodation are dismantled. Investors that are not prepared for concurrent price corrections in US Treasuries (USTs) and other asset classes in 2019 may be exposed to unintended risks.

Three key factors are lining up to drive UST yields higher, in our assessment: increased borrowing needs from the US government, a decline in UST buying from the Fed and other governments and rising inflationary pressures. The first storm on the horizon is the growing fiscal deficit. Increased spending from the Trump administration, along with tax cuts, and ongoing mandatory spending are projected to drive the fiscal deficit toward 5% of GDP (gross domestic product), in our analysis. That increases the already high borrowing needs of the government. The second storm is the diminished official buying demand, both domestically from the Fed as it unwinds QE, as well as externally from foreign governments. This leaves a large funding gap that will need to be filled by price-sensitive investors, who would need to roughly triple their current levels of buying to fill the void. Less buying volume and more supply volume means yields need to rise to find new clearing levels.

Those two dynamics alone would probably be enough to drive yields higher. But a third storm is brewing in the form of inflation. Wage pressures have been rising on exceptional strength in the US labour market, along with a lack of skilled and unskilled labour in certain sectors. The labour pools have been further constrained by restrictions on both legal and illegal immigration from the Trump administration.

Additionally, late-cycle fiscal stimulus, deregulation and tax cuts have added fuel to an already strong economy. Sector tariffs are also expected to raise costs for consumers. Each of these conditions has inflationary implications, in our assessment. Given the current environment, we expect the Fed to continue hiking rates toward the neutral rate in 2019. Taken together, all of the aforementioned factors form a perfect storm of rate pressures that we expect to drive UST yields higher in the upcoming year.

Another risk that investors may be overlooking is the growing political and structural risks across Europe. Five years ago, European voters were focused on traditional issues such as the economy, fiscal spending and unemployment. Today, European Commission surveys indicate much stronger voter concern for immigration and terrorism. That shift in focus has been reflected in the political landscape. Support for far-right nationalist parties has grown in several eurozone countries, notably including France, Germany, Italy and Austria, among others. Outside of the eurozone, countries like Hungary, Poland and the Czech Republic have slid even further toward protectionism and far-right nationalism, building barriers and increasingly emulating the Russian approach to governance rather than the European Union’s (EU’s). This is a worrying trend for European integration, in our view, as inward-looking governments are less likely to work together in a time of crisis.

Currently, European political and structural risks can be most acutely seen in Italy, where disparate political parties in the governing coalition share common ground on Euroscepticism, protectionism and increased fiscal spending. Of primary concern for Europe is the risk that Italian debt would become unsustainable at a 10-year yield around 3.6%, in our analysis. While a crisis is not imminent, the likelihood that the EU would come together to bail out Italy as it did for Greece in 2011 appears far less likely today. In 2011, there was barely enough political cohesion to hold the union together, but leaders at the time saw the greater good of doing so. Today, fewer people in power share that same thinking. On the whole, investors may be underappreciating the full scope of potential risks in Europe, in our opinion. We think the euro will remain vulnerable to unresolved structural and political risks in the upcoming year.

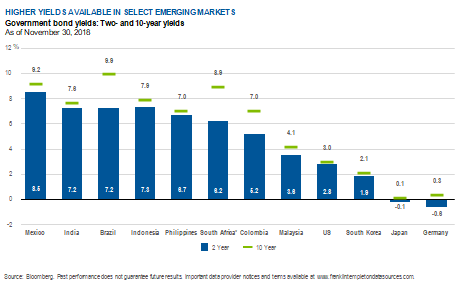

Local-currency emerging markets show the highest level of undervaluation across the global fixed income markets, in our assessment. But it’s important to recognize that the asset class is not uniform. Individual countries are far more distinct than they were decades ago. Several countries have diversified their economies, significantly broadened their local-currency debt markets, expanded their domestic investor bases and built up resiliencies to external shocks. Others continue to have persistent structural imbalances, unreliable institutions and fragile economies. It’s crucial to accurately identify those differences. In 2019, it will be increasingly important to identify countries that offer idiosyncratic value that is less correlated to broad-based beta (market) risks, in our view, as rising rates in the US should impact individual countries in starkly different ways. Countries with low rate environments, or large structural imbalances and economic soft spots, could be vulnerable to external rate shocks. However, countries with stronger economies, balanced current accounts and relatively higher yields should be in a stronger position to absorb rate shifts of 100 basis points or higher.

Overall, we think it’s important to recognize that the state of the world that investors have become accustomed to for the last decade is not going to continue indefinitely. In 2019, we expect UST yields to rise and various asset classes to endure price corrections as monetary accommodation unwinds. The challenge for investors will be that the traditional diversifying relationship between bonds and equities may not hold true as UST yields rise. We have already seen periods in 2018 when risk assets declined as the “risk-free” rate (UST yield) ratcheted higher. Those types of simultaneous declines across bonds, equities and global risk assets have the potential to recur, in our view, as markets exit an unprecedented era of financial market distortion. These are the types of risks and opportunities we think global fixed income investors need to prepare for in 2019, not only to defend against current risks in multiple asset classes, but to look for ways to potentially benefit as rates rise.

Author - Michael Hasenstab, Chief Investment Officer - Templeton Global Macro.

WHAT ARE THE RISKS?

WHAT ARE THE RISKS? All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of the publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Authorised and regulated in the United Kingdom by the Financial Conduct Authority.