11 Jan 2023

Portfolio Manager James de Bunsen argues why holding investments that can show resilience in the face of multiple, meaningful headwinds, from market volatility to potential stagflation, should give investors confidence in 2023.

Challenging at best, brutal at worst… that was 2022 for most investors. Everyone knows it was as bad as it gets for traditional balanced investors, with bonds offering no offset for plummeting equity markets. Moreover, many alternatives also performed poorly, with the notable exception of broad commodity indices, largely driven by Russia’s conflict escalation in Ukraine.

| YTD | 2021 | |

|---|---|---|

| Private equity | -20.6 | 60.7 |

| Loans | -1.0 | 5.2 |

| Property | -21.1 | 32.6 |

| Infrastructure | -3.6 | 18.8 |

| Renewables | -6.2 | -5.0 |

| Gold | -3.8 | -3.5 |

| Commodities | 19.0 | 27.1 |

| Reinsurance | -4.0 | 4.9 |

| Hedge funds | -3.6 | 2.7 |

| Global equities | -14.1 | 22.4 |

| Global bonds | -11.0 | -1.5 |

Source: Morningstar Direct, Bloomberg, total returns to 30 November 2022. Indices used: LPX Composite TR EUR, Morningstar LSTA US LL TR USD, FTSE EPRA Nareit Global REITs TR USD, FTSE Dvlp Core Infrastructure TR USD, Morningstar Gbl Util – Renewable GR USD, S&P GSCI Gold Spot USD, Bloomberg Commodity TR USD, SwissRe Global Cat Bond TR USD, HFRI-I Liquid Alternative UCITS Index USD, MSCI World GR USD, Bloomberg Global Aggregate TR Hdg GBP. Past performance does not predict future returns.

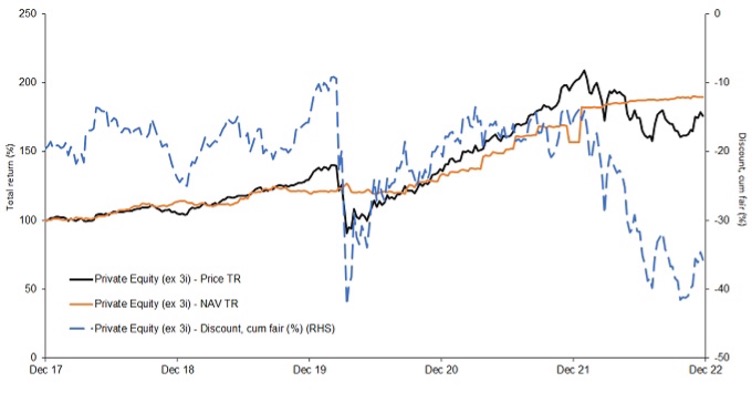

The indices in Exhibit 1 are all liquid, mainly consisting of listed securities, rather than private markets, which – thus far – have seemingly managed to defy these generalised negative moves (according to their own mark-to-model valuations), despite significantly wider NAV discounts (Exhibit 2).

Source: JP Morgan, Refinitiv Datastream, 1 December 2017 to 1 December 2022. TR = total return. Private Equity (ex 3i) – Price TR and Private Equity (ex 3i) – NAV TR (LHS) rebased to 100 at start date. Past performance does not predict future returns. Cum fair discount here includes income and assumes any debt is repaid at current market value.

Historically, we know that while private market valuations are slow to adjust downwards, they get there eventually. This is likely to come through in year-end valuations (published sometime in Q1 2023) and also as companies in the venture capital and growth parts of the market run out of cash and need to carry out further capital raises at lower valuations.

So, what did we learn from 2022? Mainly that all asset classes are impacted by higher interest rates that dictate both the cost of capital and rates at which assets are discounted. The latter is particularly pertinent for long-dated assets, such as those typically found in the infrastructure sector.

On the positive side, specialist areas of credit, such as loans and asset-backed securities tend to have floating rate coupons, which makes them profoundly more attractive than fixed-rate bonds as rates rise. Nevertheless, they are still credit investments and are therefore subject to the same laws around cost of capital.

Reinsurance as an asset class is also generally accessed via debt instruments with floating rate coupons. Until late September, this sector was largely immune to the carnage in mainstream markets. However, this all changed after Hurricane Ian barrelled into Florida, triggering the second-costliest insured loss in history. Being genuinely uncorrelated does not mean that bad things cannot happen!

Finally, hedge funds – as per usual – had a mixed year. Overall, indices were down but there was huge dispersion among and within sub-sectors. The major winners were managed futures and trend-following strategies. Any discretionary macro managers that were ahead of the game in terms of where monetary policy were headed also had an advantage. Bringing the whole sector down, however, were long/short equity funds, which suffered from generally being long biased, and skewed towards growth stocks, which fell most.

While broad renewables indices were negative due to rising bond rates and windfall taxes, there were plenty of winners in the sector. The war in Ukraine caused power prices to spike, turbo-charged the energy transition and hammered home the need for energy security.

By comparing 2022 to 2021, one can easily conclude that active asset allocation can, if done well, really improve returns. Private equity had a stellar year in 2021 but valuation metrics across the markets were flashing red. Investors in 10-year, closed-ended, private funds have no real choice but to sit tight and hope that longer-term numbers recover. By investing in liquid vehicles to access alternative assets, investors can, however, adjust their portfolio’s exposure to interest rates and equity market gyrations. Meanwhile, those with calm heads can take advantage of the inevitable market over-reactions to unexpected events, such as war in Europe or a catastrophically misjudged budget.

The outlook is unclear to say the least. But that does not mean one cannot invest with conviction. Holding investments that can show resilience in the face of multiple, meaningful headwinds, or perform in a backdrop that overwhelmingly looks stagflationary, should give investors confidence.

The battle to tame inflation goes on and thus interest rates have likely not yet peaked, even if longer-term bond yields may have done so. We continue to favour assets with a high degree of inflation linkage such as infrastructure and renewables. Renewable and energy efficiency companies should continue to benefit from the drive to reach net zero. Discount rates have adjusted higher and therefore downside risk on this front looks low.

Elsewhere, listed private equity and property vehicles have already priced in a very severe fall in valuations. This looks particularly overdone in some property sectors where occupational markets look very robust, demand structurally outweighs supply and balance sheets are strong. As mentioned above, private equity valuations must inevitably come down, but discounts of 20-40% in the listed market already discount a prolonged and severe downturn, akin to 2008. There are many aspects of the global economy that are different to the global financial crisis (GFC), most pertinently the strength of the labour market and the fact that corporates have taken advantage of super-low rates to improve their debt profile.

The key risk remains inflation and how much tightening is needed. Investments that can benefit from the volatility associated with monetary policy regime changes, something that favours certain macro hedge fund strategies, are also a key component of a robust alternatives portfolio.

As 2022 demonstrates, genuine diversifiers are rare at certain points in the cycle but, for want of a better phrase, they are worth their weight in gold.

Important Information:

The views presented are as of the date published. They are for information purposes only and should not be used or construed as investment, legal or tax advice or as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. Nothing in this material shall be deemed to be a direct or indirect provision of investment management services specific to any client requirements. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent, are subject to change and may not reflect the views of others in the organization. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. No forecasts can be guaranteed and there is no guarantee that the information supplied is complete or timely, nor are there any warranties with regard to the results obtained from its use. Janus Henderson Investors is the source of data unless otherwise indicated, and has reasonable belief to rely on information and data sourced from third parties. Past performance does not predict future returns. Investing involves risk, including the possible loss of principal and fluctuation of value.

Not all products or services are available in all jurisdictions. This material or information contained in it may be restricted by law, may not be reproduced or referred to without express written permission or used in any jurisdiction or circumstance in which its use would be unlawful. Janus Henderson is not responsible for any unlawful distribution of this material to any third parties, in whole or in part. The contents of this material have not been approved or endorsed by any regulatory agency.

Janus Henderson Investors is the name under which investment products and services are provided by the entities identified in Europe by Janus Henderson Investors International Limited (reg no. 3594615), Janus Henderson Investors UK Limited (reg. no. 906355), Janus Henderson Fund Management UK Limited (reg. no. 2678531), Henderson Equity Partners Limited (reg. no.2606646), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Janus Henderson Investors Europe S.A. (reg no. B22848 at 2 Rue de Bitbourg, L-1273, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier).

Outside of the U.S.: For use only by institutional, professional, qualified and sophisticated investors, qualified distributors, wholesale investors and wholesale clients as defined by the applicable jurisdiction. Not for public viewing or distribution. Marketing Communication.

Janus Henderson, Knowledge Shared and Knowledge Labs are trademarks of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.