10 Apr 2026

Please note that this article was originally published on 3 Mar 2026.

Portfolio manager Thomas Hauguaard discusses how emerging markets’ sensitivity to energy prices (net importers or exporters) – could affect those economies if higher prices persist.

As markets assess the conflict in the Middle East, the dominant transmission channel has not been geopolitical escalation itself, but the implications for energy flows. Oil prices moved sharply higher and commercial shipping through the Strait of Hormuz effectively stalled, driven by heightened security risks, tanker incidents, GPS interference and the withdrawal of insurance coverage. To date, markets are pricing in an energy risk premium, rather than a confirmed or permanent loss of supply, but the situation remains fluid.

Whether this is a short-lived geopolitical risk-shock, a structural shock to oil prices or somewhere in between is key as it will determine the impact on the global economy and the resultant winners and losers.

Other channels, including inflation dynamics and potential US Federal Reserve (Fed) interest rate repricing, are secondary and become relevant only if energy prices remain elevated for a sustained period.

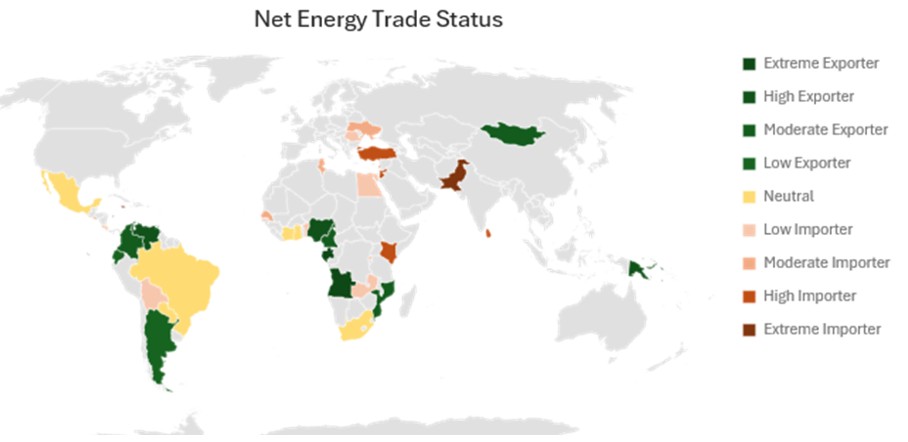

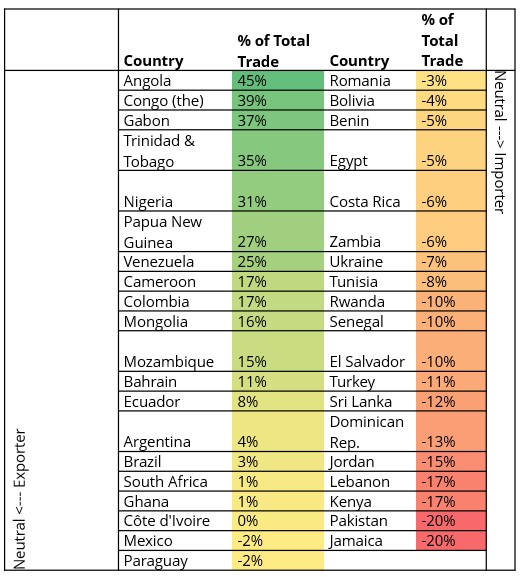

In practical terms, markets will be driven by oil prices and their persistence over time, with clear implications for EM winners and losers:

In short, duration matters more than headlines. The longer energy prices remain elevated, the more macro‑relevant the shock becomes, and the more differentiation we expect to see within EM.

Source: Austrlian Bureau of Statistics, GeoNames, Microsfot, Navinto, Open Places, OpenstreetMap, Overture Maps Foundation, TomTom, Zenrin, as at 2 March 2026.

Source: Stifel, 2 March 2026.

This remains a developing situation, and near‑term outcomes will depend on how quickly energy markets and shipping conditions normalise. We are actively engaging with internal and external research providers, market participants and regional specialists to assess market sentiment, evolving risks and country‑level implications. Our focus is on understanding where energy‑driven pressures are most acute, how sovereign bond markets are responding, and how various EM countries are impacted. So far, the market reaction has been very orderly, with only a modest spread widening and muted safe-haven behaviour.

Sovereign: Typically refers to debt issued by a national government. Sovereign bonds are backed by the country’s creditworthiness and ability to repay.

Emerging market investments have historically been subject to significant gains and/or losses. As such, returns may be subject to volatility.

Sovereign debt securities are subject to the additional risk that, under some political, diplomatic, social or economic circumstances, some developing countries that issue lower quality debt securities may be unable or unwilling to make principal or interest payments as they come due.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets.

Portfolio Manager