09 Jul 2026

When I was growing up, I was always taught that doing the right thing would lead to a better outcome. This guidance has stayed with me throughout my career and, looking back onnearly a quarter of a century of running sustainable funds, the advice seems apt.

A sustainable approach has always seemed the right way go about investing and despite some recent pushback, sustainable investing has worked. True, it has not always enjoyed a smooth path, but challenges have usually been short term in nature.

Recently, these have come in the form of geopolitical issues that have boosted the shares of energy producers and weapons manufacturers.

But the advantage of having more than two decades of returns to examine is that we can step back from such short-term noise and look at what has worked and why?

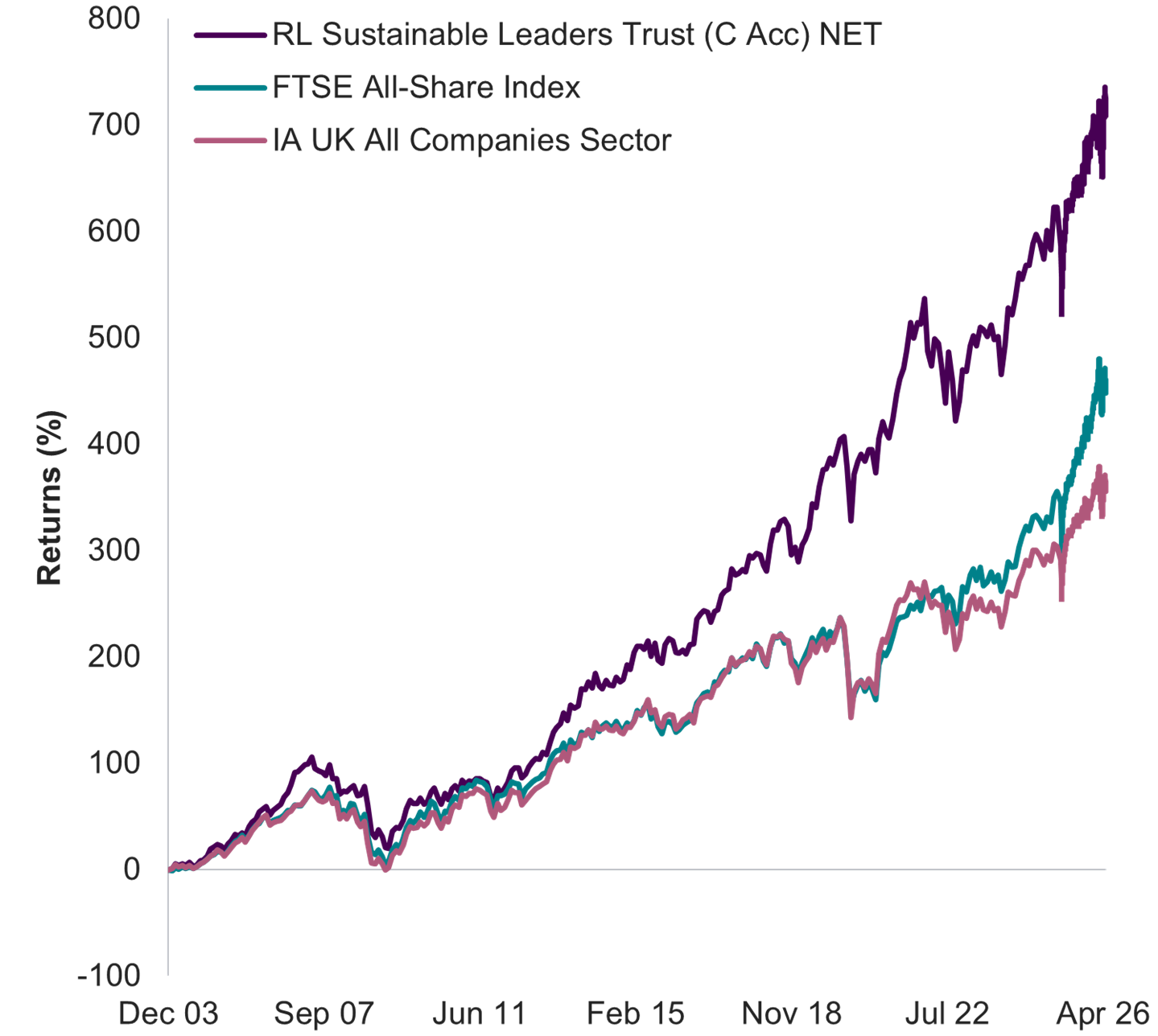

We can see that our flagship sustainable funds, and those of many competitors, have actually performed very well against their peer groups and benchmarks over the past 20+ years. Our Sustainable Leaders fund sits very comfortably ahead of its benchmark and peer group since launch.

Past performance is not a guarantee or reliable indicator of future returns. The impact of fees or other charges including tax, where applicable, can be material on the performance of your investment. The impact of fees reduces your return.

| YTD | 1 Yr | 3 Yr Ann | 5 Yr Ann | S.I Ann* | |

| Quartile Rank | 2 | 2 | 2 | 2 | 1 |

Source: RLAM, Morningstar as at 30 April 2026. Fund performance figures are stated gross of fees and gross of tax, based on mid-day prices in GBP for the Royal London Sustainable Leaders Trust (C Acc). The index for the Fund is FTSE All-Share Index. Index performance is based on close of business prices.

|

31/03/2025 - 31/03/2026 |

31/03/2024 - 31/03/2025 |

31/03/2023 - 31/03/2024 |

31/03/2022 - 31/03/2023 |

31/03/2021 - 31/03/2022 |

|

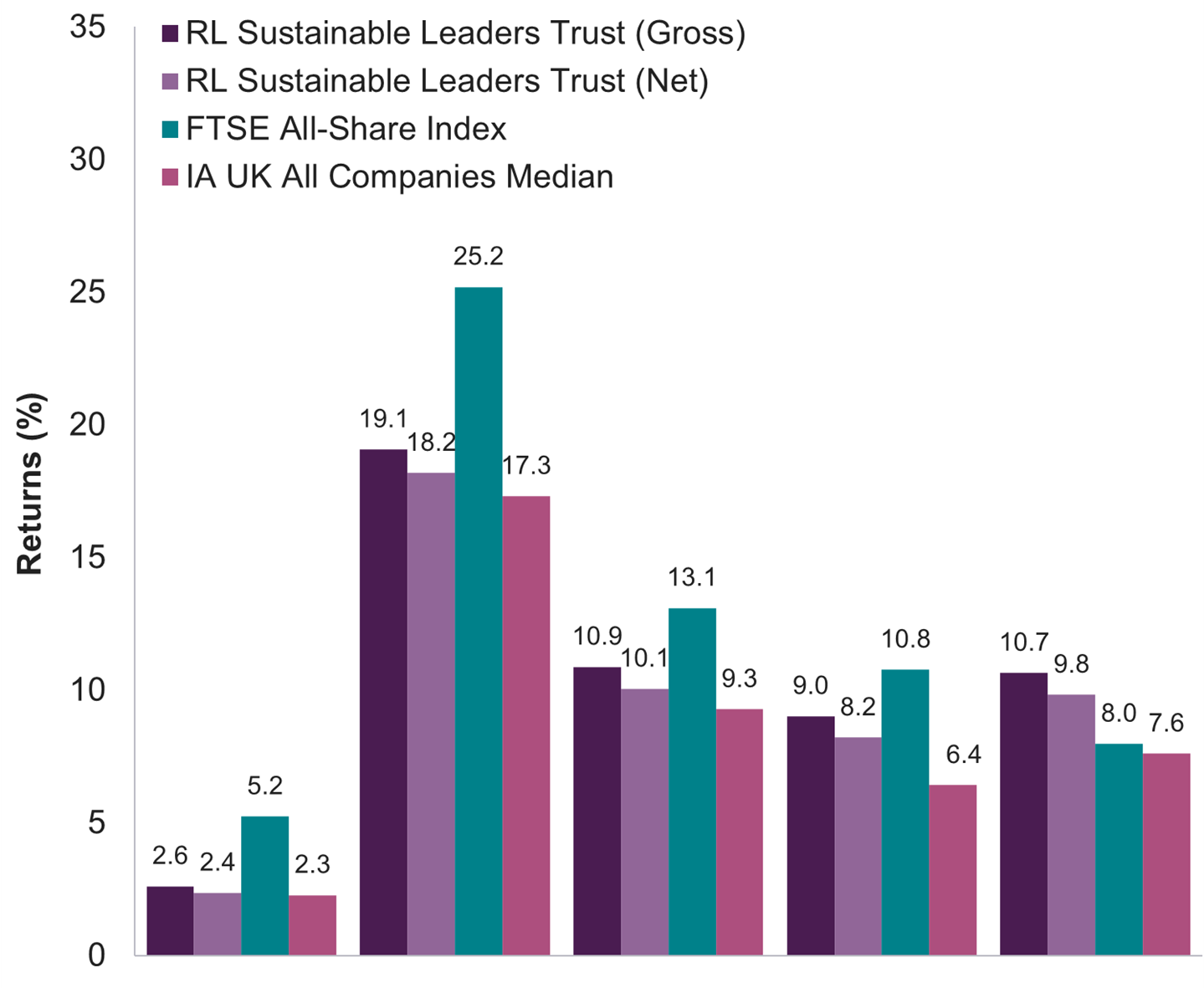

| Share Class | 2 | 3.82 | 11.55 | 1.11 | 14.47 |

Source: Royal London Asset Management as at 31 March 2026.

During this time sustainable strategies have endured numerous style rotations, market cycles and global shocks: from the aftermath of the 11 September attacks, through the global financial crisis, Covid, and today’s unsettled geopolitical environment. These have been periods when markets have rewarded very different investment styles. Yet sustainable funds have come through all of these turbulent times and emerged in good shape.

In my view, this is more than just good fortune. As an investor you can maybe be lucky for a few years, but it’s not possible to be lucky for more than 20 years. Longevity through multiple market environments is a sign that something more structural is at work.

So why has sustainable investing worked? What is it about adopting a sustainable approach that has created this advantage? To answer this, look at the changes that sustainable investing has brought to the wider industry.

Perhaps the most significant change is the sheer amount of information that we now get from companies relating to environmental, social and governance issues. Importantly, the quality of this information has also improved by leaps and bounds.

Looking back, the kind of information that we got from companies 20 years ago would not even merit a ‘poor’ disclosure rating by today’s standards. The superior information now available is highly additive. It allows us to link sustainability to financial outcomes and to better understand risks, while assessing corporate resilience to those risks, and to identify good businesses to invest in.

Those of us running sustainable funds were at the vanguard when it came to requesting more information, but the whole industry has benefited. ‘Traditional’ investors focused on profit and loss, balance sheets and cash flow can also benefit from understanding how labour practices, supply chain management, governance structures or environmental factors affect long term value. This allows everyone to potentially make much better investment decisions.

This is why ESG analysis folded itself into fundamental research. It’s not a separate exercise or a moral overlay. There is no virtue in ignorance of ESG factors when making investment decisions. If better information even occasionally leads to a better outcome, then we believe that this additional level of ‘tyre kicking’ can consistently generate additional alpha.

The second major change over the last 20 years is the amount of influence that we now have over the behaviour of companies. Back in the early 2000s, most sustainable or ethical products were based largely on screening. If you wanted to avoid specific companies or sectors that was possible, but that was where the role of investors ended.

Engagement with companies on ESG issues and opportunities to influence their behaviour were minimal. Yes, we could meet with management to discuss traditional financial issues, but most companies simply would not put environmental or social topics on the agenda.

Compare that to today’s world, where the weight of global sustainable capital in the market means engagement with senior management on issues like climate strategy, working practices, or governance structures is now routine.

We need only look at the recent rebellion by shareholders to BP’s plans to scrap its climate reporting to see the influence that shareholders can now have on big global emitters.

In more recent years, we have seen the growing importance of ‘stakeholder wealth’. This concept asserts that while shareholder returns remain a key focus, they are no longer viewed in isolation. Companies that understand the importance of human capital, environmental capital and broader societal relationships are often better placed to sustain returns over time. In turn, they benefit from lower costs of capital and higher long-term valuations. This concept would have seemed alien to many of my contemporaries in the investment world 20 years ago.

To those that were cynical about the potential benefits of sustainable investing, it’s worth looking at what the world might look like if they had been right, and if doing the right thing really was a worthless pursuit.

It’s true that companies may have made improvements to their operations for financial reasons, for example to avoid fines and lawsuits. And had companies failed to respond to sustainability issues, governments may have stepped in more forcefully. But history suggests that increased regulation is not always the most efficient route to better outcomes. Investor-led change has often proved more flexible, more targeted and more effective.

The absence of sustainable investors would mean that many of the benefits we have gained from increased corporate disclosures would have been missing. Given that lower quality outputs, in my view, the lack of this information would probably have manifested itself in lower long-term returns for clients.

The effect on customer choice would also have been negative. Without sustainable investment options, many individuals would have had nowhere to invest their long-term savings in a way that aligns with their values. Encouraging people to invest is one of our industry’s major challenges. Removing options would only have alienated more people from the benefits investing can provide.

As we can see, sustainable investing today looks very different to crude exclusions-based approaches of 20-odd years ago. The push for more data, better disclosures and improved corporate accountability has helped deliver benefits for those of us that have always cared about sustainability issues, alongside clients more widely.

So having spent all these years doing the right thing when it comes to investing, it’s very encouraging that it does indeed seem to have resulted in better outcomes, both for clients and for society.