19 Jun 2019

The suspension of the Woodford Equity Income fund was announced on the 3rd June, following which we issued a brief research note. Given the continued negative press surrounding this, we thought it would be useful to provide our current views on the fund and the wider Woodford Investment Management business.

This more detailed research note explains some of the background leading up the fund suspension, the information we currently have, how we will be monitoring the situation and our overall opinion.

We have recently met with Neil Woodford and followed this up with a further conference call to get more detail on the current situation and to discuss some of our concerns. The output and conclusion from these meetings is contained within this update.

As a first comment, I think it is fair to say that Neil Woodford has been a very high profile fund manager for a number of years and justifiably so based on his long-term performance record. This worked in his favour for quite some time, but his profile - and the associated press attention he has received has certainly been a negative factor in the fund’s recent history given some of the factors mentioned below.

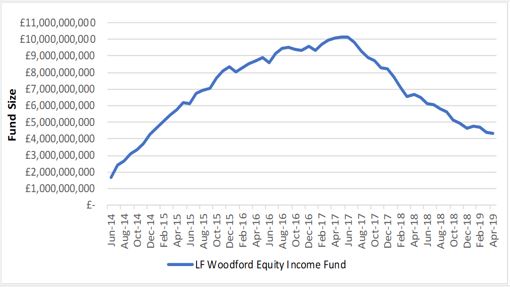

The LF Woodford Equity Income fund was launched in June 2014 and, mainly due to his excellent long-term performance record whilst at Invesco, it attracted a significant amount of assets very quickly, reaching over £6 billion in the first 12 months and rising to over £10 billion at its peak in early 2017. Since that time the fund has experienced significant outflows, falling to below £4 billion at the end of May 2019 just before the fund suspension when further large outflows were expected, including one large redemption request from an institutional investor. This is illustrated in the chart below:

Chart 1 – Fund Size June 2014 to April 2019

Source Morningstar Direct

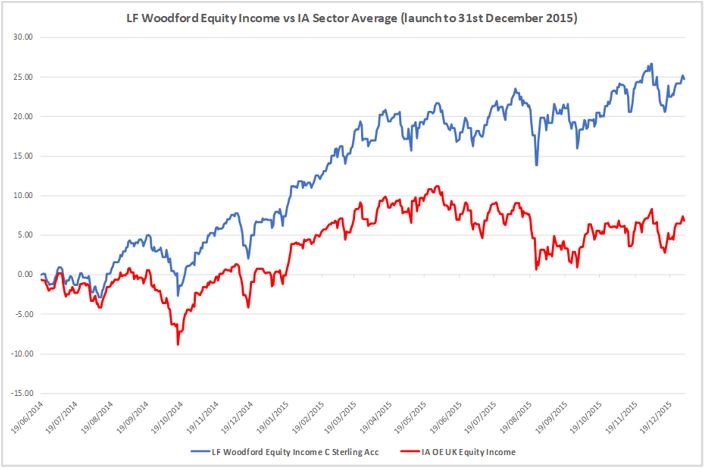

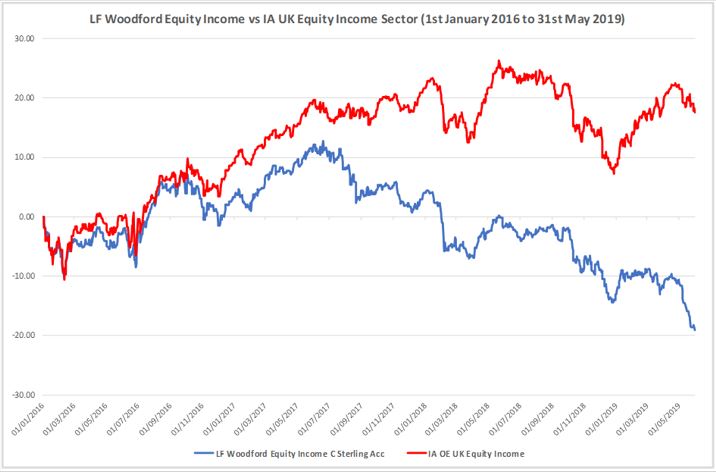

Undoubtedly one of the key reasons for the fall in assets has been fund performance. Neil Woodford’s long-term performance at Invesco was extremely strong and many investors expected this to continue at his new home. The charts below illustrate performance since launch of the Woodford fund, breaking this period down into the first 18 months from launch, which was a very strong period for both absolute and relative performance, and the subsequent period to the end of May 2019, which saw the fund significantly underperform.

Chart 2 – Performance from launch to 31.12.2015

Source Morningstar Direct

Investors who had backed Woodford at launch would have been very pleased with this initial performance and this undoubtedly contributed to the significant increase in the fund size. The fund size peaked approximately 1 year after the peak in relative performance.

Chart 3 – Performance from 1.1.2016 to 31.5.2019

Source Morningstar Direct

As Neil Woodford has highlighted, the market environment of low interest rates, low inflation, steady but low economic growth with pockets of stronger growth overseas has been very favourable for growth stocks and particularly stocks deemed to be ‘quality’, many of which have significant overseas revenues. This has been a difficult environment for income-orientated managers generally but Woodford’s investment strategy of investing in fundamentally undervalued stocks has been a further headwind, as this has led to significant exposure to UK domestic stocks, which have been hit by the uncertainty surrounding Brexit.

Recently, commentary has almost completely focused on the fund’s unquoted and illiquid companies, which is discussed below, but the fund has seen a number of stocks in the portfolio suffer significant falls over the last couple of years. Examples that have hit the press include Provident Financial, Allied Minds, IP Group, Purplebricks, Capita, the AA and more recently Keir Group, each of which fell over 50%. Woodford stated within our recent conversations that the profit warnings that he has been exposed to within his quoted stocks have been less frequent than in his previous 20 years of managing money, but the associated stocks have seen significant falls as a result of their profit warnings. As these have been among the larger positions in the portfolio, this has meant they have been significant contributors to the underperformance.

Recent press commentary has been almost exclusively focussed on the fund’s unquoted stocks and illiquidity, but we believe some of this has been misrepresented.

The rules for a fund such as LF Woodford Equity Income allow a portfolio to have up to 10% in unquoted securities and the fund cannot hold over 10% for any extended period. It is the responsibility of the ACD (in this case Link) to monitor this. It is important to stress that this rule has not been broken and the manager has been taking action to maintain this position. Some of the actions taken have received some very negative press, particularly the share swap in February where 5 of the fund’s unquoted companies, totalling £79m, were swapped for shares in the Woodford Patient Capital Investment Trust. The listing of a small number of the fund’s unquoted stocks on the Guernsey stock exchange, thereby removing them from the unquoted allocation, was another controversial decision but was within the rules. This, however, did not improve their liquidity and this leads on to the next point.

The liquidity of a portfolio does not solely depend on whether a stock is listed or not listed (unquoted). Unquoted stocks are typically very illiquid, as there are very few, if any, active traders in these stocks except for specialists such as private equity and venture capitalists. Quoted stocks, particularly non-large cap stocks, can prove to be illiquid if there is a lack of active traders and this can happen at any time. Even large cap stocks can prove to be illiquid at times, if there is a relative absence of active traders. Liquidity management is primarily the responsibility of the fund/investment management company and is a key part of the risk management process with oversight from the ACD. Due to the speed and size of the fund outflows, the easiest way to meet these redemptions has been to sell/reduce some of the more liquid positions but this, in turn, naturally increases the relative size of the illiquid portion. There have to be questions as to how robust the liquidity/risk management process has been over this period. We should however note that the FCA have been monitoring the position through the ACD Link Fund Solutions since February 2018.

Trading in the fund is suspended, so no-one can sell or buy shares in the fund, but the fund will continue to be daily priced. Neil Woodford has stated that, during the suspension, he will be looking to sell all his unquoted stocks and reinvest this into larger, more liquid companies, thereby changing the overall shape of the portfolio but without changing the overall investment strategy. He will also be looking at his less liquid holdings and may choose to sell all or most of this. At the time of our meeting he had already sold 2 of his more illiquid stocks to raise around £100m. This will be a slow process.

Due to the significant fund outflows, not just from this fund but also from the Woodford Income Focus fund, and the decisions by St James Place and Openwork to switch their investment mandates away from Woodford, the wider Woodford Investment Management business has seen significant changes in the last few weeks. The cost base of the company has been cut in half, including making staff redundant and cuts in salaries for remaining employees. At the moment, there have been no changes to the investment management or risk management teams, but these cannot be ruled out in the future, which leads on to the next point.

There is currently a large degree of uncertainty surrounding the wider business, especially the level of assets that will remain with the firm. Unlike the situation with direct UK commercial property funds in 2016, all investor redemption requests that were submitted prior to the fund suspension have been cancelled and any investors still wishing to redeem must submit their requests when the fund re-opens, so we have no idea what the queue for redemptions was or what the future level of redemption requests will be. Assets in the Income Focus fund have fallen below £350m and may continue to fall, particularly as Hargreaves Lansdown have removed their support. The board of the Woodford Patient Capital trust are supportive of Neil Woodford at the moment, but they will be continually assessing their position. Woodford has stated that the business has a sustainability plan which assumes a very conservative level of assets, but they have not released this figure and there has to be a chance that this will be underestimated.

As of the 18thof June 2019 the FCA announced an investigation into the events that lead to the suspension of the Equity Income fund in June this year. The FCA have been closely monitoring the fund since February 2018 when the first of two breaches of the 10% unlisted holdings rule took place.

Neil Woodford has a significant amount of work on his hands over the coming months, not just in terms of re-shaping the portfolio - selling his unquoted assets, reducing his illiquid exposure, reinvesting into larger companies and raising cash, all of which is likely to take several months - but also in persuading existing investors they should remain invested when the fund re-opens. We do not have any special insights on this but if investors are influenced by the negative press coverage, particularly those who invested without advice, the outflows could be significant. Should a significant number of investors choose to redeem their fund holdings then he will need to raise cash, severely limiting his ability to execute his strategy.

One way that Woodford might help stem the outflows would be through improved fund performance. His current focus on undervalued, domestically-focused UK companies could prove to be a successful strategy over the longer-term given current valuation levels, but a lot of uncertainty remains, particularly surrounding Brexit and the current Tory leadership election, so it may be some time before there is a catalyst for this value to be realised. Any sort of Brexit clarification is likely to be helpful but, again, the timescales are unknown. Even if Woodford is proven right at some point, he may not have the luxury of time to benefit from this.

We will be monitoring the situation very closely over the coming days, weeks and months, including progress on the sale of unquoted and illiquid holdings and reinvestment into larger, more liquid stocks, any changes to the business, including key personnel, and fund performance, but there is very little clarity at this stage.

We would also remind advisers and clients that although the Woodford team manage the portfolio the trustees have oversight and responsibility for the assets of the fund. The separation of the management of the fund's assets from their ownership is the most fundamental element of investor protection provided by authorised funds. This defends the interests of the incoming, outgoing and continuing investors in the fund.

As a result, the LF Woodford Equity Income fund rating remains Under Review until there is much further clarity and we are able to make a fully informed decision.