28 Mar 2026

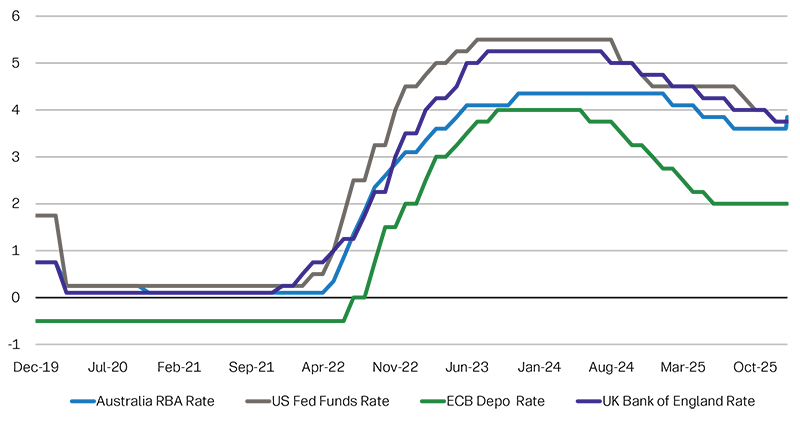

Source: Bloomberg 31 December 2019 to 3 February 2026

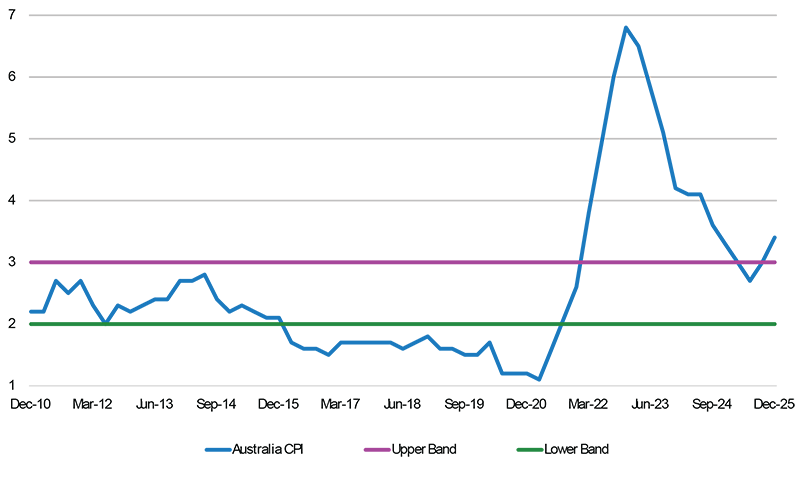

In short, inflation. The RBA’s tolerance for the stubborn level of inflation reached its limit. The latest CPI data showed inflation reaccelerating, pushing it back above the top of their 2-3% target range. Updated inflation forecasts released on 3 February 2026 indicated CPI is expected to remain above target throughout 2026, before easing into 2027. With recent employment data also showing greater resilience, it’s unsurprising that the RBA is signalling the likelihood of higher rates ahead.

Source: Bloomberg 31 December 2010 to 31 December 2025

One immediate consequence of raising rates is that it should further strengthen the Australian Dollar. The currency has already strengthened materially, up 8.5% against the US Dollar since November. A stronger AUD can create macro headwinds by dampening inflation and reducing the demand for exports. Together, these effects can lessen the need for future rate hikes.

The need for further hikes will depend on the currency’s performance in the coming months – particularly relative to Asian currencies where Australian exports are more focussed. Markets are currently pricing in as much as 40bps of cuts from both the US Federal Reserve and Bank of England, while no further tightening is priced for the ECB or the Bank of Canada. Against this backdrop, Australia stands out among its peers, making it one of the key markets to watch this year.

It remains unclear whether this is an early signal that other central banks may soon change direction, or if it simply reflects the desynchronisation of global interest-rate cycles.

Colin Finlayson, CFA

Portfolio Manager

Colin Finlayson, portfolio manager, is a member of the global rates and multi-sector portfolio management teams.