11 May 2026

Amid increased uncertainty over the future path of policy rates, including renewed inflation risks linked to higher energy prices and geopolitical tensions, the role of money market funds has come back into focus. In this environment, our investment team highlight why money market funds offer a disciplined framework for navigating a higher-rate world.

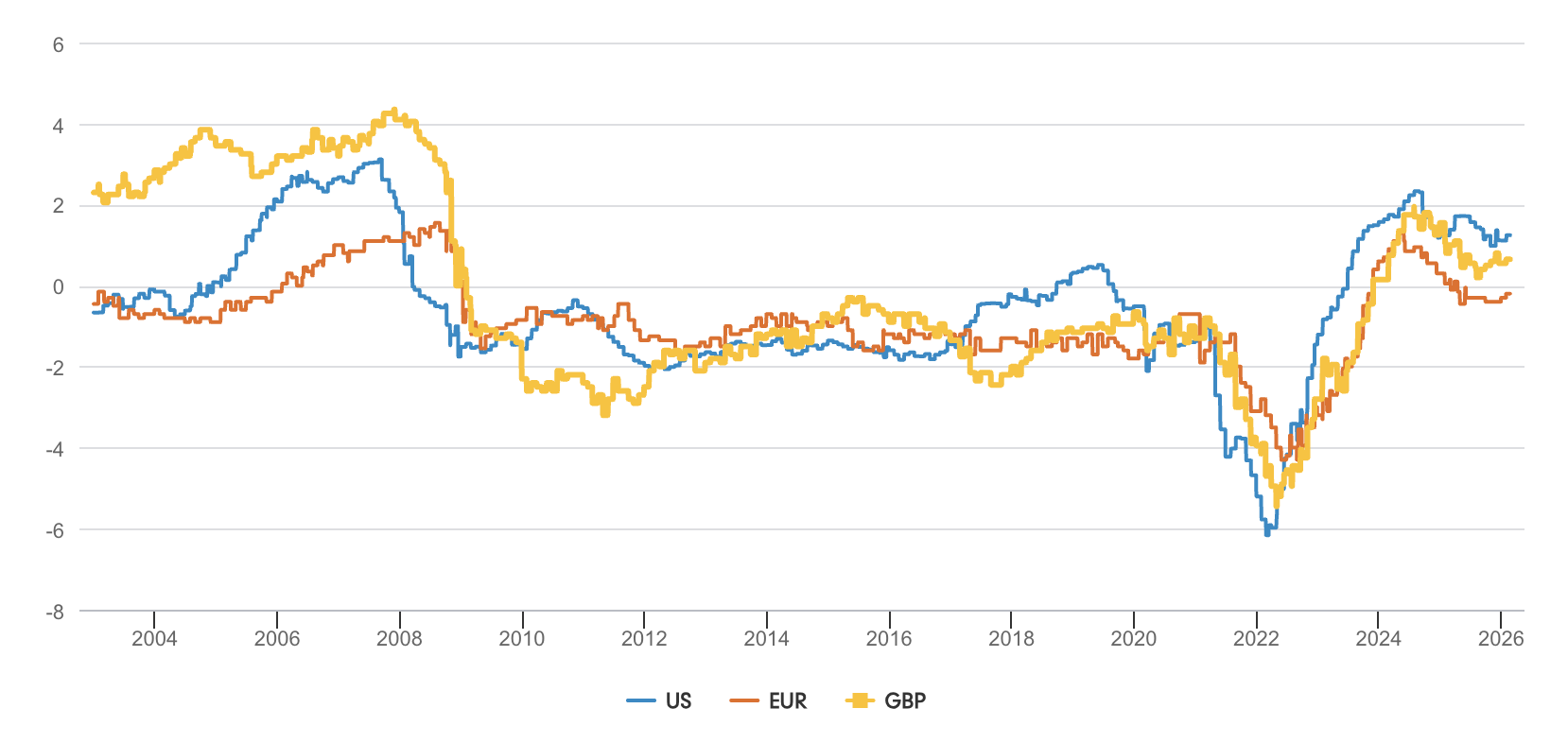

Over the past year, it has become increasingly clear that the global economy is not returning to the pre-Covid environment of near-zero interest rates. The inflation shock of recent years has reset monetary policy, lifting estimates of neutral rates across developed markets. While central banks have cut rates over the last couple of years, policy remains tight while rates are well above the norms that prevailed for much of the previous decade.

In the United States, the scope for further easing from the Federal Reserve appears limited, with markets now pricing no further cuts this year. The case for aggressive easing remains unconvincing. Economic growth has proved resilient, fiscal support remains material and business surveys continue to point to underlying momentum. Labour market conditions are softening only gradually, reducing the urgency for a decisive policy shift. At the same time, renewed inflation risks from the conflict in Iran, alongside core PCE inflation that remains above target and has already shown signs of re-acceleration, have further complicated the outlook for policy.

In Europe, the outlook has become more fluid. Recent increases in energy prices have pushed inflation expectations higher and led markets to reprice the path of policy rates. Investors now anticipate higher rates, with markets currently pricing three rate hikes from the European Central Bank this year. This reflects concerns that the euro area’s reliance on natural gas could amplify inflation pressures. With monetary policy broadly seen as close to neutral, the ECB may have greater scope to respond if inflation proves more persistent than expected.

Meanwhile, the Bank of England sits in a slightly different position. Markets are currently also pricing around three rate hikes, reflecting similar concerns around energy-driven inflation and the UK’s exposure to gas prices. At the same time, UK monetary policy is already viewed as somewhat restrictive relative to the euro area, which may limit the need for a sustained tightening cycle. As a result, the outlook remains finely balanced, with policymakers weighing persistent inflation risks against signs of gradual cooling in parts of the economy.

Against this backdrop, our base case for policy in 2026 has shifted. While recent hawkish commentary from both the Bank of England and the ECB reflects heightened inflation concerns, the case for aggressive tightening in response to a potentially temporary supply shock remains less clear. We believe market pricing may overshoot in the near term, which could create opportunities to add duration at more attractive levels.

In the United States, by contrast, political pressures and the Federal Reserve’s dual mandate may support a relatively more accommodative stance than in other major economies.

Real policy rates still well above post-2010 levels

Source: Fidelity International, Bloomberg, February 2026. Real policy rates are calculated as policy rates deflated by core CPI (US, UK) and core HICP (euro area).

This environment has clear implications for portfolio construction. Against resilient growth and elevated policy rates, the risk-reward profile of longer-duration assets has become less attractive. Heavy sovereign issuance, particularly across developed markets, has structurally altered bond market dynamics, weakening the traditional defensive role of long-dated government bonds.

As a result, the focus has shifted away from capital gains driven by falling yields and toward income, liquidity and flexibility. For money market portfolios, this means maintaining discipline rather than wholesale repositioning. Our approach remains centred on short-duration and high-quality exposure, supported by selective and measured adjustments.

From a positioning perspective, we reduced the weighted average maturity of our EUR funds significantly in February, largely on valuation grounds, and continued to reduce the WAM of all of our funds in the early part of March. In recent days, however, we have begun to extend maturities again modestly as the risk-reward at the front end of the curve has improved.

Overall, the emphasis remains on resilience. Portfolio construction is designed to perform across a range of outcomes, including scenarios where rates remain higher for longer or where volatility in risk assets resurfaces.

Against this backdrop, the case for money market funds remains compelling. Investors can earn a meaningful yield while preserving capital and maintaining daily liquidity. With many risk assets appearing expensive, money market funds combine income with the flexibility to redeploy capital when opportunities arise.

This positioning becomes particularly valuable in periods when inflation shocks or geopolitical developments push yields higher, as shorter-duration strategies are less exposed to the resulting volatility.

Investor expectations around the path of yields have shifted, reducing the pressure to lock into longer-dated assets in pursuit of income. With policy rates still elevated, money market fund yields continue to reflect a higher-rate backdrop, preserving portfolio flexibility.

Beyond income considerations, money market funds play an important structural role within portfolios. They act as stabilisers at a time when policy uncertainty, geopolitical risk and the potential for risk-asset volatility remain elevated. Periods of market stress often create sudden liquidity needs, and in those moments access to capital matters as much as return. Money market funds provide that flexibility, allowing investors to redeploy capital efficiently as opportunities emerge.

In a higher neutral-rate world, money market funds play a more strategic role within portfolios. They represent an active allocation choice. For institutional investors seeking income, liquidity and resilience amid uncertain rate paths, they remain a compelling solution.