Our Capital Market Assumptions (CMAs) provide return, volatility and correlation forecasts for various asset classes, typically over a strategic ten-year investment horizon. They are calculated using a proprietary model which employs quantitative econometric analysis and incorporates a diverse range of inputs, including bottom-up and top-down insights from across our global investment platform. This provides a robust foundation for our strategic asset allocation processes, which play a key role in investment solution design and portfolio construction.

The below summary of expectations applies to our standard ten-year strategic capital market assumptions (CMA) forecast period, from the latest periodic six-month cut-off date of 31 March 2026:

Key takeaways

- AI: We have developed a holistic framework that combines Fidelity’s top-down macro scenario thinking with bottom-up analyst insights, captured regularly through our Analyst Survey. The weighted findings form our base case: somewhat higher long-term GDP growth. This is the first step in an ongoing process - we will evolve the framework as more data becomes available, focusing on labour impacts, investment dynamics, geopolitics and energy resilience.

- Macroeconomics: The effects of geopolitical fragmentation, elevated debt levels, and technological/energy transitions, will keep macroeconomic volatility above its average pre-Covid era level. Inflationary pressures will also remain elevated.

- Equities: Equities remain the key strategic portfolio growth drivers. Expected returns have increased, largely due to the positive effect of AI through the GDP channel. Prevailing margin levels are above our forward-looking estimates across many regions, but the equilibrium level of corporate profit margins has shifted structurally higher, reflecting a more profitable and innovation-driven environment. We will continue to monitor our forecasts in this area closely as the AI revolution could create both tailwinds and headwinds for profitability (e.g. labour productivity gains and policy responses like taxation).

- Fixed income: Bonds remain attractive thanks to higher government yield curves, but bond market volatility and equity-bond correlations will remain elevated. Expected credit returns are appealing, but tight spreads make risk/return trade-offs key. Short-term bonds are attractive shock absorbers and sovereigns should still diversify during recessionary shocks, although the latter may be less reliable during inflationary shocks.

- Private assets: Expected returns remain attractive for investors willing to take on more illiquidity risk. Manager selection will be key to delivering positive outcomes, especially due to the higher rate backdrop and elevated levels of dry powder. There are no clear signs of immediate stress in private credit, but the asset class warrants close monitoring.

- Foreign exchange: The US dollar may not provide the same return tailwinds or safe-haven characteristics as it has in recent decades.

- Portfolio construction: These dynamics call for a thoughtful active investment approach that incorporates greater regional/sectorial diversification and utilises a broader toolkit that includes tactical overlays, credit spectrum diversification, and differentiated sources of risk premia like absolute return or derivative strategies.

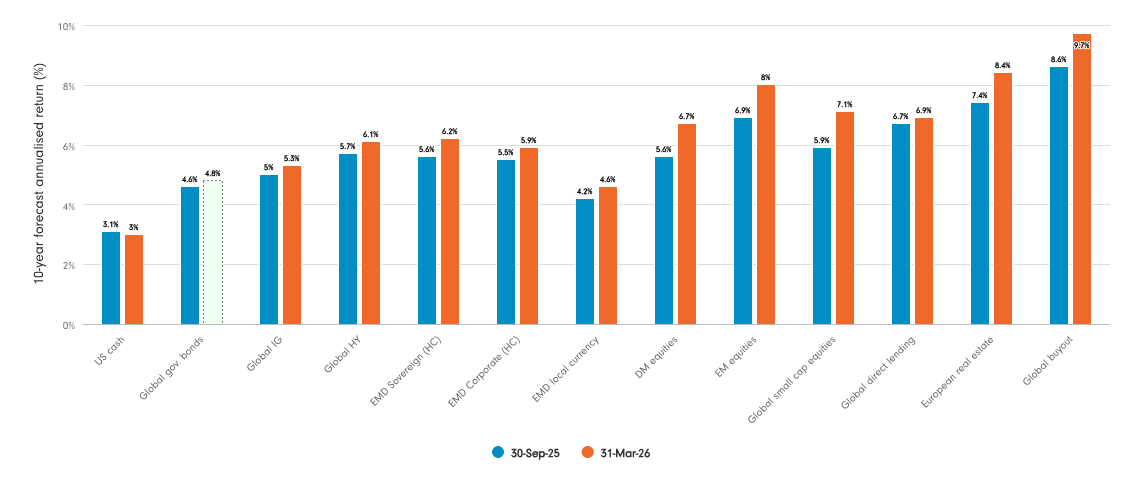

Aggregate long-term return potential remains attractive across asset classes

Projected 10-year average nominal returns, USD

For illustrative purposes only. Assumptions are based on proprietary modelling, reflecting the views of investment professionals at Fidelity International.

Source: Fidelity International, 31 March 2026. IG: investment grade; HY: high yield; EMD: emerging market debt; DM: developed market; EM: emerging market.

Insight into our CMAs (PDF)

Our most recent CMAs (PDF)