30 Jun 2026

While the last technology cycle was consumer led, the AI cycle is shaping up to be more enterprise-focussed. Marcel Stötzel, Portfolio Manager of the Fidelity European Fund and Fidelity European Trust, explains why Europe could prove to be one of the most overlooked AI exposures in global equities, with strengths in sectors such as financials, industrials and healthcare positioning it well for the next phase of AI driven growth.

The last technology cycle was consumer-led. Streaming, social media, smartphones, and electric vehicles transformed daily life, creating enormous value for companies that captured users, attention, and engagement at scale. AI looks different. While consumers will benefit, the biggest economic gains are likely to accrue to businesses using AI to automate workflows, boost productivity, and improve decision-making across the real economy.

That shift has important implications for investors. Europe is often viewed as lacking AI exposure because it has fewer consumer technology champions than the US. But Europe’s strength in banks, insurance, industrials, and pharmaceuticals may make it uniquely positioned for a more enterprise-led AI cycle. As markets move beyond AI model developers and infrastructure providers toward the long-term beneficiaries of adoption, Europe could prove to be one of the most overlooked AI exposures in global equities.

One of the defining features of the last technology cycle was its consumer centricity. The dominant winners of the 2010s - social media platforms, streaming services, smartphones, and electric vehicles - were fundamentally business-to-consumer stories.

Technology delivered more engaging digital experiences, better entertainment, and innovative consumer products, with much of the economic spillover accruing directly to individuals. The next technology cycle, underpinned by AI, is shaping up differently. While consumers will certainly benefit from AI-powered services, the larger economic impact is likely to be felt by enterprises. This cycle is increasingly about businesses becoming more productive, automated, and efficient, shifting the primary spillover beneficiaries from households to companies themselves.

This distinction matters for investors because it changes where value is likely to accrue. It also challenges the simplistic view that Europe lacks meaningful AI exposure. Europe’s deep and diverse base of industrial, financial, healthcare, and infrastructure companies leave it well positioned to benefit from broad-based enterprise adoption of AI.

The previous technology cycle was built around user acquisition and engagement. Companies succeeded by attracting vast consumer audiences and monetising them through subscriptions, advertising, or direct product sales.

Netflix, for example, transformed media consumption through recurring subscriptions, while social media platforms monetised user attention through targeted advertising and powerful network effects. Apple and Tesla combined technology with branding to create highly aspirational consumer products.

Across these businesses, the formula was broadly similar: growth driven by consumer adoption, monetisation through subscriptions, advertising, or product sales, and competitive advantages built on brand strength and network effects. At their core, these were fundamentally consumer-focused business models.

AI is creating a different economic architecture. While consumer-facing applications attract most of the headlines, the larger long-term opportunity may lie in enterprise adoption.

Value in the AI ecosystem can broadly be split into three groups:

So far, investors have overwhelmingly rewarded the first two groups. Share prices of model developers and infrastructure enablers have risen sharply as markets price in accelerating demand and expanding earnings potential. Enterprise beneficiaries, by contrast, have seen far less enthusiasm, creating an inconsistency in the broader AI narrative.

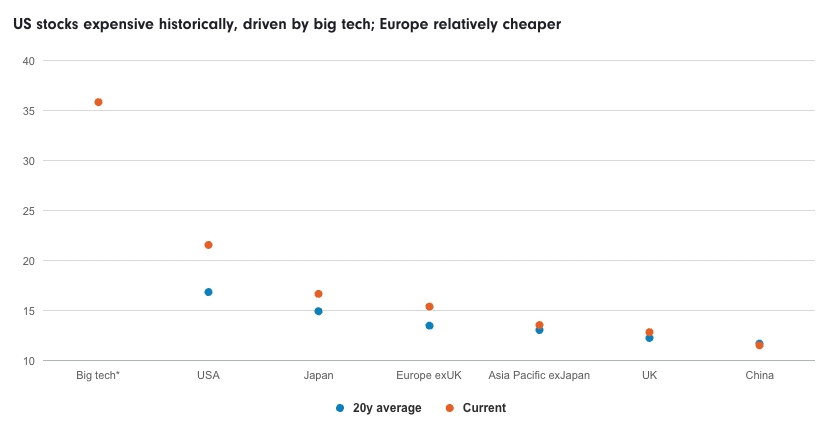

US stocks expensive historically, driven by big tech; Europe relatively cheaper

Source: Fidelity International, LSEG DataStream, May 2026. MSCI indices.

*Big tech (cap weighted) = Nvidia, Alphabet, Apple, Microsoft, Amazon, Broadcom, Tesla, Meta, Micron, Intel, Oracle, Cisco.

If companies are collectively spending hundreds of billions on AI infrastructure and models, it follows that meaningful productivity gains should eventually emerge for the businesses deploying these systems. Yet while providers and enablers have enjoyed both earnings upgrades and multiple expansion, most enterprise users have not.

This incongruence is largely explained by scepticism. Investors want tangible proof that AI adoption will translate into materially stronger earnings for enterprise users before re-rating these businesses accordingly.

Investors have heard promises of digital transformation and process improvement for years, particularly in sectors with legacy systems such as banking and insurance. As a result, there is understandable reluctance towards broad claims around AI-driven productivity.

Many of the most important AI applications are still in their infancy and have yet to meaningfully impact earnings. Most enterprise-grade agentic AI solutions - systems capable of automating entire workflows rather than simply assisting with tasks - have existed for less than six months. It is therefore too early for large-scale benefits to be clearly reflected in reported numbers.

That said, there are already tangible signs of where AI could drive meaningful change. Banks are increasingly discussing the ability of AI to automate customer servicing, compliance, onboarding, and internal operations. Insurance companies are using AI to improve pricing and risk assessment, while AI-driven weather prediction tools are already helping agricultural insurers and farmers make better decisions, with clear implications for reinsurers. Across professional services, AI has the potential to materially increase the amount of work that can be completed with existing employee bases.

Crucially, the benefit of AI does not necessarily require companies to reduce headcount. The more important opportunity may be allowing businesses to take on more clients, process more work, and improve service quality without proportionally increasing labour costs. In this sense, AI has the potential to become a major productivity multiplier across large parts of the economy.

Other sectors may take longer to realise these gains. Pharmaceuticals, for example, face long and complex drug development cycles, but AI still has significant potential to improve discovery, clinical trial design, and data analysis over time.

The key question no longer appears to be whether viable use cases for agentic AI exist, but rather how quickly these solutions can be deployed at scale across organisations.

This shift toward enterprise and industrial beneficiaries is important for Europe. A common perception is that Europe lacks meaningful AI exposure because it does not possess the same concentration of mega-cap technology companies as the US or parts of Asia. However, this view misunderstands where the AI opportunity is increasingly emerging.

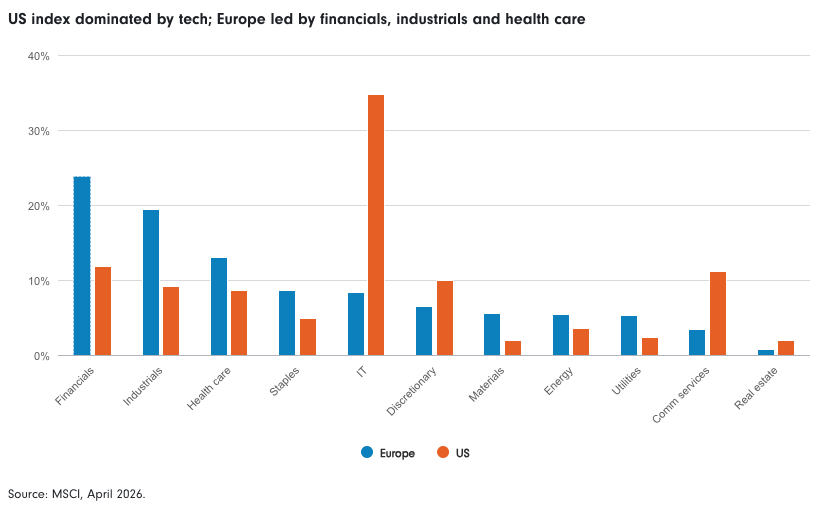

European equity markets are structurally different from those in the US. They are less dominated by consumer internet platforms and far more exposed to sectors likely to benefit from enterprise AI adoption, including financials, energy and power infrastructure, pharmaceuticals, industrial automation, and engineering. In many respects, Europe’s market composition is naturally aligned with a more enterprise-driven AI cycle.

US index dominated by tech; Europe led by financials, industrials and health care

Europe also possesses a deep industrial backbone that is critical to scaling AI infrastructure globally. European companies are global leaders in semiconductor manufacturing equipment, electrical systems, power management, cooling technologies, thermal solutions, industrial automation, and precision engineering. These businesses form part of the enabling layer of AI, supplying the physical infrastructure required to support increasingly compute-intensive systems.

Power is key area of exposure. AI is highly energy intensive, placing electricity generation, grid investment, and energy efficiency at the centre of the investment case. Europe’s providers in these areas therefore stand to benefit directly from rising AI deployment and data centre demand.

Yet the most underappreciated opportunity may lie not with the enablers, but with Europe’s enterprise users themselves. As AI adoption broadens across industries, Europe’s banks, insurers, industrial companies, and healthcare businesses could become some of the largest long-term beneficiaries of AI-driven productivity gains.

We have analysed the opportunity set company by company across Europe and estimate that approximately 20% of MSCI Europe constituents have direct revenue exposure to AI. At a sector level, exposure is particularly high within IT (70%), industrials (35%), and communication services (15%).

Despite this, many enterprise beneficiaries have yet to see their AI potential reflected in share prices - a disconnect that is unlikely to persist indefinitely. Historically, markets tend to reward infrastructure providers early in a technology cycle because capital expenditure is immediately visible in revenues and earnings. The productivity benefits for end users typically emerge later, once adoption becomes widespread and operational improvements begin to flow through to financial results. That pattern appears to be unfolding again.

The first phase of the AI cycle rewarded the builders: semiconductor companies, model developers, and infrastructure suppliers. The next phase may increasingly reward the adopters - companies capable of translating AI into higher productivity, stronger margins, improved customer retention, and faster growth. This is an area where Europe may contain many of the market’s future winners.

The last technology cycle was consumer-led. Smartphones, streaming, digital payments, social media, and cloud software transformed convenience, entertainment, and connectivity for individuals. Companies created enormous value by capturing users, monetising attention, and building powerful consumer brands.

The AI cycle is likely to evolve differently. While consumers will still benefit, the potentially larger and more durable economic gains may accrue to enterprises through productivity improvements, workflow automation, and better decision-making. That distinction matters because it changes where investors should look for long-term value creation. Rather than focusing solely on consumer technology platforms, investors increasingly need to consider the broader ecosystem - particularly the enterprise users capable of deploying AI effectively at scale.

Europe is well positioned for this shift. Its enterprise-heavy market structure means it is far more exposed to AI than conventional wisdom suggests. The market has already rewarded the builders of AI. The next question is whether it is beginning to underestimate the long-term beneficiaries who will ultimately use it most effectively.

Important Information

This information must not be reproduced or circulated without prior permission.

This material is for Institutional Investors and Investment Professionals only, and should not be distributed to the general public or be relied upon by private investors.

This material is provided for information purposes only and is intended only for the person or entity to which it is sent. It must not be reproduced or circulated to any other party without prior permission of Fidelity.

This material does not constitute a distribution, an offer or solicitation to engage the investment management services of Fidelity, or an offer to buy or sell or the solicitation of any offer to buy or sell any securities in any jurisdiction or country where such distribution or offer is not authorised or would be contrary to local laws or regulations. Fidelity makes no representations that the contents are appropriate for use in all locations or that the transactions or services discussed are available or appropriate for sale or use in all jurisdictions or countries or by all investors or counterparties.

This communication is not directed at, and must not be acted on by persons inside the United States. All persons and entities accessing the information do so on their own initiative and are responsible for compliance with applicable local laws and regulations and should consult their professional advisers. This material may contain materials from third-parties which are supplied by companies that are not affiliated with any Fidelity entity (Third-Party Content). Fidelity has not been involved in the preparation, adoption or editing of such third-party materials and does not explicitly or implicitly endorse or approve such content. Fidelity International is not responsible for any errors or omissions relating to specific information provided by third parties.

Fidelity International refers to the group of companies which form the global investment management organization that provides products and services in designated jurisdictions outside of North America. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. Fidelity only offers information on products and services and does not provide investment advice based on individual circumstances, other than when specifically stipulated by an appropriately authorised firm, in a formal communication with the client.

Europe: Issued by FIL Pensions Management (authorised and regulated by the Financial Conduct Authority in UK), FIL (Luxembourg) S.A. (authorised and supervised by the CSSF, Commission de Surveillance du Secteur Financier), FIL Gestion (authorised and supervised by the AMF (Autorité des Marchés Financiers) N°GP03-004, 21 Avenue Kléber, 75016 Paris) and FIL Investment Switzerland AG.

UAE: The DIFC branch of FIL Distributors International Limited is regulated by the DFSA for the provision of Arranging Deals in Investments only. All communications and services are directed at Professional Clients and Market Counterparties only. Persons other than Professional Clients and Market Counterparties, such as Retail Clients, are NOT the intended recipients of our communications or services. The branch is established pursuant to the DIFC Companies Law, with registration number CL2923, as a branch of FIL Distributors International Limited, registered in Bermuda. FIL Distributors International Limited is licensed to conduct investment business by the Bermuda Monetary Authority.In Hong Kong, this material is issued by FIL Investment Management (Hong Kong) Limited and it has not been reviewed by the Securities and Future Commission.

In Hong Kong, this material is issued by FIL Investment Management (Hong Kong) Limited and it has not been reviewed by the Securities and Future Commission.

FIL Investment Management (Singapore) Limited (Co. Reg. No: 199006300E) is the legal representative of Fidelity International in Singapore. This document / advertisement has not been reviewed by the Monetary Authority of Singapore.

In Taiwan, Independently operated by Fidelity Securities Investment Trust Co. (Taiwan) Limited 11F, No.68, Zhongxiao East Road, Section 5, Taipei 110, Taiwan, R.O.C. Customer Service Number: 0800-00-9911.

In Korea, this material is issued by FIL Asset Management (Korea) Limited. This material has not been reviewed by the Financial Supervisory Service, and is intended for the general information of institutional and professional investors only to which it is sent.

In China, Fidelity China refers to FIL Fund Management (China) Company Limited. Investment involves risks. Business separation mechanism is conducted between Fidelity China and the shareholders. The shareholders do not directly participate in investment and operation of fund property. Past performance is not a reliable indicator of future results, nor the guarantee for the performance of the portfolio managed by Fidelity China.

Issued in Japan, this material is prepared by FIL Investments (Japan) Limited (hereafter called “FIJ”) based on reliable data, but FIJ is not held liable for its accuracy or completeness. Information in this material is good for the date and time of preparation, and is subject to change without prior notice depending on the market environments and other conditions. All rights concerning this material except quotations are held by FIJ, and should by no means be used or copied partially or wholly for any purpose without permission. This material aims at providing information for your reference only but does not aim to recommend or solicit funds /securities.

For information purposes only. Neither FIL Limited nor any member within the Fidelity Group is licensed to carry out fund management activities in Brunei, Indonesia, Malaysia, Thailand and Philippines.

FEEP200300