11 Aug 2022

Inflation is still stubbornly high, meaning the Fed and the ECB are keeping their feet pressed down on the hawkish pedal for now. However, growth data is turning sharply negative in developed markets as the consumer squeeze and tighter financial conditions bite. Europe must also deal with an impending gas crisis that will deal a hefty blow to industry and consumers alike.

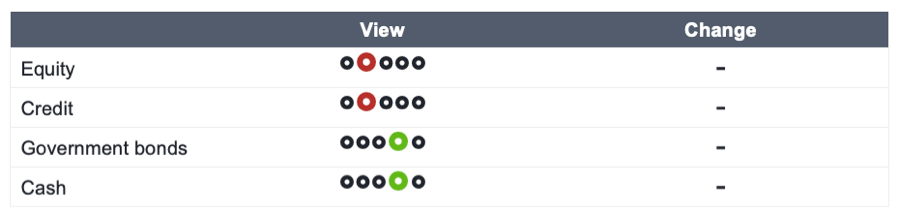

Valuations have adjusted down, but, in our view, not enough to fully reflect the grave outlook. Earnings have yet to be meaningfully revised lower, however, implying risk assets could have further to fall if companies start to report weak performance and a worsening outlook. We are positioned underweight equities and credit.

We remain overweight government bonds as a way of adding protection to portfolios and because fears over slowing growth are beginning to dominate those of inflation. Within government bonds, we prefer Gilts and Bunds to Treasuries and JGBs as we feel that slowing growth is more likely to convince the ECB and BoE to turn dovish sooner.

Within equity regions, we prefer emerging markets. China is easing monetary and fiscal policy and has fewer Covid disruptions for now. Many other EMs have attractive valuations and a less restrictive policy outlook. We remain underweight Europe, where further gas disruptions are casting a long shadow over already weak growth prospects. We stay neutral on the US, UK, Japan, and Asia Pacific equity markets for now.

In credit, we raise conviction on our overweight investment grade position as a defensive move. We keep our underweight to high yield and now go underweight EM hard currency debt too.

Finally in currencies, we maintain our long USD as a safe haven. We move underweight EM FX as we feel there is room for devaluation against the dollar. We also take profit on a long-standing USD GBP trade and close a EUR GBP position. We remain underweight the yen.

Macro outlook

US on the brink of recession

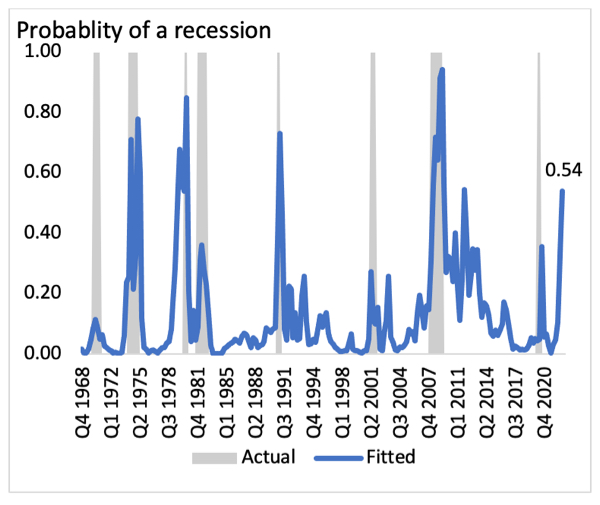

Our proprietary activity trackers indicate that the US will go into recession in Q3 or Q4 this year, in contrast to the current consensus that a recession is most likely to occur in 2023. Our trackers have moved down to levels consistent with historic recessions going back to 1969, while our future activity tracker suggests things will get worse from here. However, markets are yet to fully reflect the imminent recession risk.

The length and depth of the recession will depend on how central banks respond. Policy makers are still trying to rectify last year’s mistake of assuming inflation would subside without intervention. How they will react to a recession is hard to predict. But if central banks continue to prioritise bringing inflation down at any cost, the recession will be severe.

Chart 1: Our future activity tracker points to high likelihood of US recession

Source: Fidelity International, Bloomberg, July 2022.

We expect some relaxation of the supply-side issues that have dogged the global economy since the pandemic. However, conditions here remain restrictive, and improvement will not be enough to offset other problems. The US labour market is still strong, but we view it as a lagging indicator of economic performance. In addition, oil prices remain another swing variable when it comes to assessing the magnitude and duration of the hard landing.

Europe’s future also looks challenging but is more dependent on Russian gas imports. Russia appears to be gearing up to reduce supply through the Nord Stream pipeline. The European Commission has called for a voluntary 15 per cent gas consumption cut from member states.

In the event of a full shutdown leading to large scale rationing, the hit to German GDP alone could be more than 5 percentage points. However, given gas flows from Russia are largely driven by geopolitics, the outlook remains volatile, though actual behavioural changes in terms of gas usage are already starting to take place.

At its July meeting, the ECB finally joined the global hiking cycle with a larger than expected 50bps move. However, the window to hike for the ECB is closing fast as the reality of falling consumer confidence, slowing growth and gas disruptions set in. We believe that the ECB will have to abandon its hiking cycle after the governing council’s September meeting.

The ECB also announced details of its Transmission Protection Instrument (TPI) aimed at keeping periphery spreads in check. However, the tool’s strict conditionality limits its potential usage (although there is room for flexibility in its interpretation) and runs the risk of markets testing its credibility. Indeed, the spreads on Italian debt have widened further since the announcement.

The prospect of a new election in Italy, with far-right parties in the lead, means that Italy is unlikely to meet the conditions, at least in the short term, leading to concerns around whether the ECB will intervene or not. All eyes are now on the ECB’s tolerance for widening spreads and we believe there is reason to be cautious as Italy’s political crisis unfolds.

As widely expected, the Federal Reserve raised interest rates by another 75 basis points in July in what is now the most aggressive sequence of hikes since Paul Volcker was in charge at the US central bank in the early 1980s. Much higher-than-expected inflation remains the key driver together with the ongoing strength in the labour market. Chair Powell kept the option of another 75bps hike at the September meeting on the table but caveated it by highlighting the importance of short-term data. Powell also said the Fed is now in meeting-to-meeting mode with less focus on specific guidance.

We are now entering the phase of the cycle where the Fed has delivered significant tightening in a very short period. The economy is sending conflicting signals with soft data in recessionary territory whilst hard data, especially on the labour market side, is still showing ongoing resilience. With inflation continuing to surprise on the upside, and without a visible slowdown in the job market, the chance of another 75bps hike remains high. The Fed is looking at hard data which is lagging and may be forced into another burst of aggressive tightening. That said, Chair Powell displayed more flexibility at the July meeting than has been the case over the previous two meetings.

Throughout this hiking cycle, we have been of the view that the Fed would end up hiking less than market pricing. At one point, the markets priced in a terminal rate of 4 per cent, which we thought was too high. We agree with the current market expectation for a terminal rate for this cycle at around 3.25 per cent. However, the economy is sending conflicting signals and the strength of lagging hard data on which the Fed is focused may change the near-term trajectory for rates. Our base case remains one of recession in the US over the next six months given the tightening in financial conditions and slump in consumer confidence.

Fidelity’s Global Macro & SAA team contributes to Fidelity Solutions & Multi Asset’s tactical asset allocation process by providing key macro inputs, working alongside the investment team to understand and respond to the macroeconomic drivers of markets.

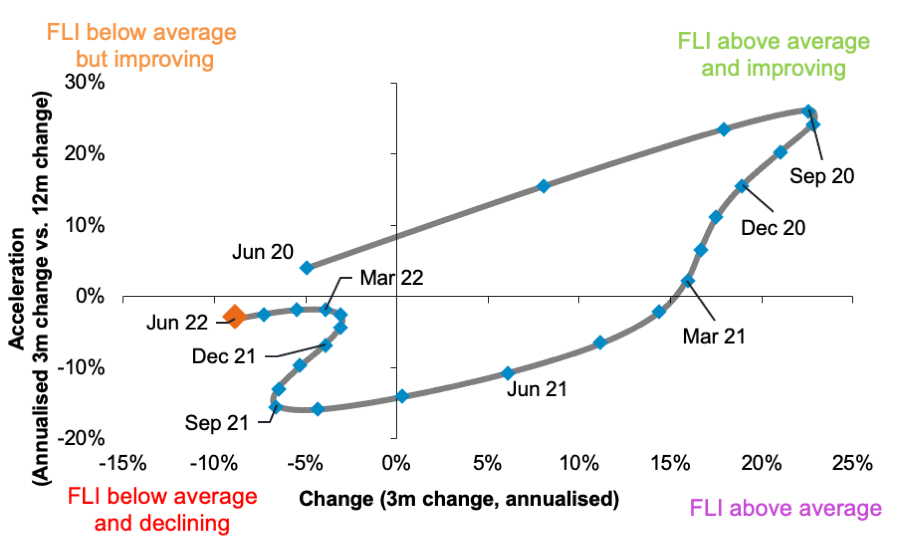

The FLI Cycle Tracker deteriorated further in June, moving deeper into the ‘bottom-left’ quadrant (below average and declining). This was the 11th straight month of the FLI indicating below average and declining activity led by broad-based deterioration across sub-sectors. The deceleration in global activity continues to be driven by the multiple shocks hitting the global economy this year, including the Russia-Ukraine war, China lockdowns, inflation pressures and financial conditions tightening by central banks.

FLI Cycle Tracker

Source: Fidelity International, July 2022.

FLI: 3-month % change versus OECD IP

Source: Fidelity International. July 2022.

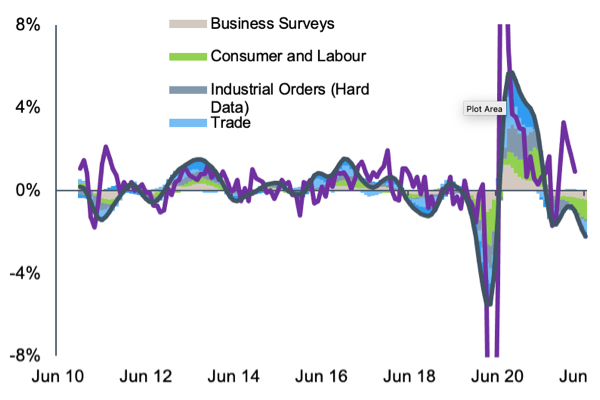

The Consumer and Labour sector moved further into the ‘bottom-left’ quadrant. The decline in Consumer confidence worsened and was broad-based across US, Germany and France, led by inflation pressures. The labour market remained strong with some moderation, with US jobless claims inching marginally higher and France’s vacancies decelerating.

Global trade shifted to the ‘bottom-left’ quadrant (below average and declining), for the first time since November last year (although downward revisions to the previous month’s data showed the shift already occurred in May). Commodities also slipped back into the ‘bottom-left’ quadrant in June, for the first time since January 2022. The move was driven by sharp falls in the Baltic Dry Index, along with more modest declines in Australia’s forward orders.

The FLI is a proprietary quantitative tool, designed to anticipate the direction and momentum of global growth over the coming months, and - importantly for investors - identify its key drivers. In practice, it is designed to lead global industrial production and other global cyclical variables by around three months. Fidelity Solutions & Multi Asset uses this as a common and repeatable reference point through the tactical asset allocation process.

![]()

| Asset class | View | Change | Rationale |

|---|---|---|---|

|

Equities |

|

|

|

|

US |

|

|

Valuations have adjusted meaningfully this year already as a result of multiples contraction, so we are watching Q2 earnings closely. The US could be defensive in what might be a volatile H2 and the dollar should be supportive. |

|

Europe ex. UK |

|

|

The ECB delivered a hawkish surprise in July, raising rates 50bps. Gas supply is highly uncertain and the risk of recession is high. We feel it is prudent to remain underweight for now. |

|

UK |

|

|

Consumer health should deteriorate significantly from here. However, UK equities are relatively cheap and the large cap index benefits from elevated commodity prices, despite their recent weakness. We are monitoring the political uncertainty, although we do not expect major changes whoever becomes prime minister. |

|

Japan |

|

|

The domestic environment and consumer sentiment are weak given the inflation pressures and energy prices. Company earnings are more linked with the global manufacturing cycle and could be impacted by supply chain disruptions and higher input costs. |

|

Emerging markets |

|

|

China’s economic activity is recovering and there is a renewed policy priority on economic growth. However, we are watching closely for possible contagion risk from the real estate market. Latin America is very attractively priced, having benefitted from recent commodity price rises. |

|

Pacific ex. Japan |

|

|

Australia’s housing market could be vulnerable in a rate hiking cycle and domestic consumers are geared to the housing market. Earnings revisions have started to weaken, although elevated commodity prices are still a tailwind. Hong Kong and Singapore are benefiting from reopening. |

|

Credit |

|

|

|

|

Investment grade (IG) bonds |

|

|

Now is the time for defensive positioning. IG valuations, especially in Europe, are more attractive than HY. US IG is only moderately cheaper than historical averages. |

|

Global high yield |

|

|

HY spreads have yet to fully price in the risk of higher defaults in the event of a recession, meaning there is room to widen further from here. |

|

Emerging market debt (EMD, hard currency) |

|

|

Leverage in EMD is much higher than HY. EMD overall is pricing in a very high probability of recession. However, hard currency EM sovereigns are very expensive. |

|

Government bonds |

|

|

|

|

US Treasuries |

|

|

Inflation is also unlikely to cool in Q3 due to base effects which may lead to another peak before easing in Q4. This should provide ammunition for the Fed to hike aggressively in the coming period, exerting curve flattening pressure which is not supportive of this relatively short duration bond index. |

|

Euro core (Bund) |

|

|

Despite a 50bps hike in July, we do not expect a sustained hiking cycle, as is priced in by markets. The high probability of recession and periphery spreads are a significant barrier for the ECB. |

| UK Gilts |

|

|

The BoE might try to front-load rate hikes, but, in common with the ECB, we struggle to see an extended hiking cycle. The UK economy is on the brink of recession, facing double digit inflation and surging energy bills. |

| Japan govt bonds |

|

|

The global growth environment as well as the latest Japanese economic data does not suggest the BOJ will change its policy anytime soon. |

| Inflation linked bonds (US TIPS) |

|

|

The rise in real yields over the last three months has been more led by breakevens than nominal rates. Breakevens are under the shadow of recession pricing and are likely to come under further pressure in a hard landing scenario. We did not have enough conviction to take a view this month. |

|

Currency |

|

|

|

|

USD |

|

|

The Fed has the strongest economic growth cushion to act hawkishly, while the dollar benefits from safe-haven status given high uncertainty. |

|

EUR |

|

|

We are closing our short euro until we have further clarity on the ECBs spread capping mechanism, gas flows into Europe and Italian politics. |

|

JPY |

|

|

The yen is undermined by ultra-loose policy and a weak trade balance. It sold off hard on the merest hint of more Fed hawkishness, a telling sign. |

|

GBP |

|

|

Sterling has weakened significantly. We still have a negative bias given the terrible current account deficit (-8%). |

|

EM FX |

|

|

EM FX looks less stretched than other USD pairs and could be vulnerable to any further falls in commodity prices or a repeat of RMB weakness if the Covid situation in China gets worse. |

Source: Fidelity International, as of July 2022. Change reflects directional difference in view versus previous month. Views reflect a typical time horizon of 12–18 months and provide a broad starting point for asset allocation decisions. However, they do not reflect current positions for investment strategies, which will be implemented according to specific objectives and parameters.

Fidelity Solutions & Multi Asset is a global team, managing portfolios using a wide range of asset classes, including equities, fixed income, real estate, infrastructure and other alternatives. The team specialises in building and managing outcome-focused strategies for clients, combining asset classes to deliver investment objectives through time.

As at 30 June 2022, the team manages over $48bn on behalf of institutional and retail clients across global regions. Our large team includes Investment Management, Global Macro & Strategic Asset Allocation, Research, Client Solutions and Implementation resources, supported by Fidelity’s significant operational infrastructure to deliver investment services to clients. We work with colleagues across Fidelity’s bottom-up investment teams across key asset classes, capturing research from this substantial global research platform.

For further information on Fidelity Solutions & Multi Asset’s strategies and services, please contact your local Fidelity representative.

Download the PDF

Important information

This material is for Institutional Investors and Investment Professionals only, and should not be distributed to the general public or be relied upon by private investors.

This material is provided for information purposes only and is intended only for the person or entity to which it is sent. It must not be reproduced or circulated to any other party without prior permission of Fidelity.

This material does not constitute a distribution, an offer or solicitation to engage the investment management services of Fidelity, or an offer to buy or sell or the solicitation of any offer to buy or sell any securities in any jurisdiction or country where such distribution or offer is not authorised or would be contrary to local laws or regulations. Fidelity makes no representations that the contents are appropriate for use in all locations or that the transactions or services discussed are available or appropriate for sale or use in all jurisdictions or countries or by all investors or counterparties.

This communication is not directed at, and must not be acted on by persons inside the United States. All persons and entities accessing the information do so on their own initiative and are responsible for compliance with applicable local laws and regulations and should consult their professional advisers. This material may contain materials from third-parties which are supplied by companies that are not affiliated with any Fidelity entity (Third-Party Content). Fidelity has not been involved in the preparation, adoption or editing of such third-party materials and does not explicitly or implicitly endorse or approve such content. Fidelity International is not responsible for any errors or omissions relating to specific information provided by third parties.

Fidelity International refers to the group of companies which form the global investment management organization that provides products and services in designated jurisdictions outside of North America. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. Fidelity only offers information on products and services and does not provide investment advice based on individual circumstances, other than when specifically stipulated by an appropriately authorised firm, in a formal communication with the client.

Europe: Issued by FIL Pensions Management (authorised and regulated by the Financial Conduct Authority in UK), FIL (Luxembourg) S.A. (authorised and supervised by the CSSF, Commission de Surveillance du Secteur Financier), FIL Gestion (authorised and supervised by the AMF (Autorité des Marchés Financiers) N°GP03-004, 21 Avenue Kléber, 75016 Paris) and FIL Investment Switzerland AG.

In Hong Kong, this material is issued by FIL Investment Management (Hong Kong) Limited and it has not been reviewed by the Securities and Future Commission.

FIL Investment Management (Singapore) Limited (Co. Reg. No: 199006300E) is the legal representative of Fidelity International in Singapore. This document / advertisement has not been reviewed by the Monetary Authority of Singapore.

In Taiwan, Independently operated by Fidelity Securities Investment Trust Co. (Taiwan) Limited 11F, No.68, Zhongxiao East Road, Section 5, Taipei 110, Taiwan, R.O.C. Customer Service Number: 0800-00-9911

In Korea, this material is issued by FIL Asset Management (Korea) Limited. This material has not been reviewed by the Financial Supervisory Service, and is intended for the general information of institutional and professional investors only to which it is sent.

Fidelity is authorised to manage or distribute private investment fund products on a private placement basis, or to provide investment advisory service to relevant securities and futures business institutions in the mainland China solely through its Wholly Foreign Owned Enterprise in China - FIL Investment Management (Shanghai) Company Limited.

Issued in Japan, this material is prepared by FIL Investments (Japan) Limited (hereafter called “FIJ”) based on reliable data, but FIJ is not held liable for its accuracy or completeness. Information in this material is good for the date and time of preparation, and is subject to change without prior notice depending on the market environments and other conditions. All rights concerning this material except quotations are held by FIJ, and should by no means be used or copied partially or wholly for any purpose without permission. This material aims at providing information for your reference only, but does not aim to recommend or solicit funds /securities.