Our Multi Asset team's views on which asset classes and markets are presenting the greatest opportunities and risks.

What has changed?

- Move overweight risk: As the conflict moves towards a messy resolution, we believe market participants will increasingly look towards still resilient medium-term fundamentals.

- Traditional safe havens less reliable: Commodities, particularly energy, are proving more effective hedges together with cash than duration or gold in the current supply-shock environment.

What has stayed the same?

- Growth resilient for now: The global economy entered the year from a position of strength, supported by earnings and fiscal policy.

- Equities preferred to credit: Equity valuations are now more attractive in some areas, whereas credit spreads still offer limited compensation for the risk.

- Fragmentation a key theme: Geopolitics and policy divergence continue to drive dispersion across regions and asset classes.

What are we watching?

- Energy market developments: The duration and severity of the shock will be key for inflation, policy, and growth.

- Central bank response: Whether higher energy prices delay or limit easing cycles.

- Shift back to fundamentals: As the conflict moves towards a messy resolution, whether markets focus on earnings and growth.

Source: Fidelity International, April 2026. Views reflect a typical time horizon of 12–18 months and provide a broad starting point for asset allocation decisions. However, they do not reflect current positions for investment strategies, which will be implemented according to specific objectives and parameters.

Cycle gauges

Source: Fidelity International, April 2026.

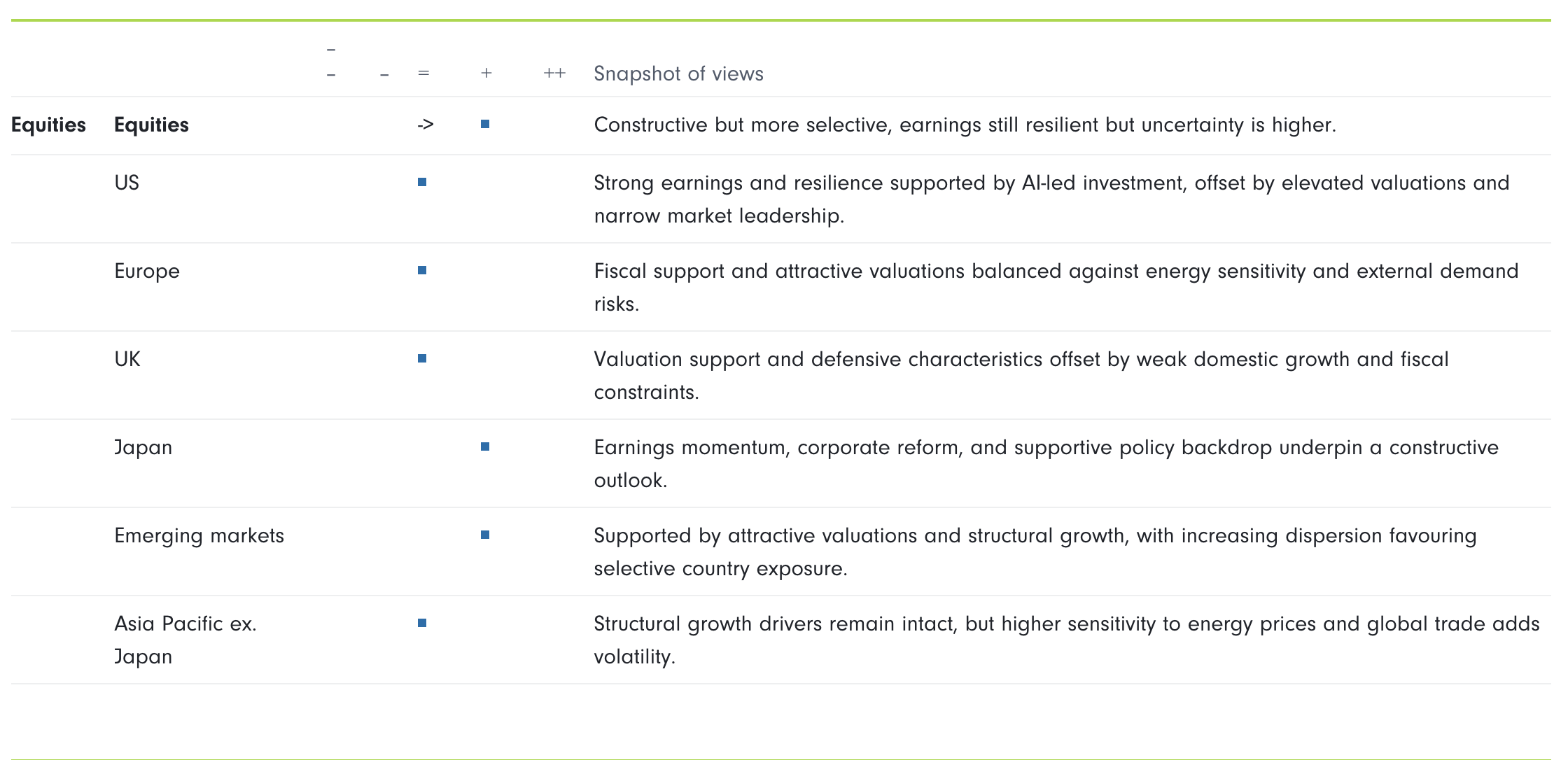

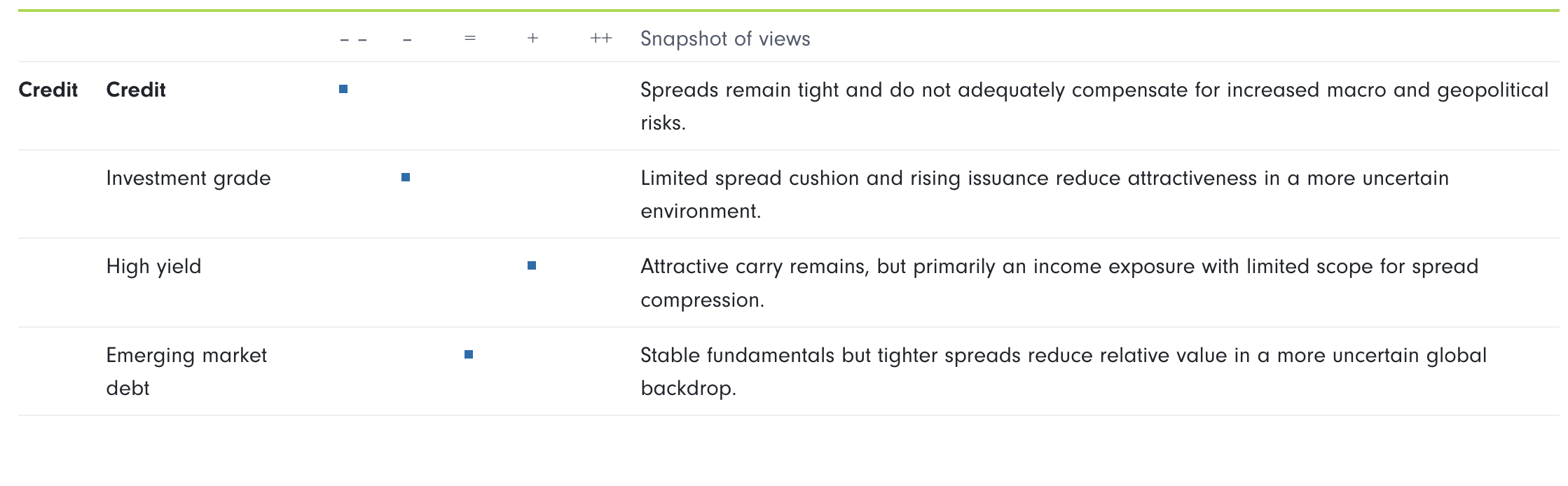

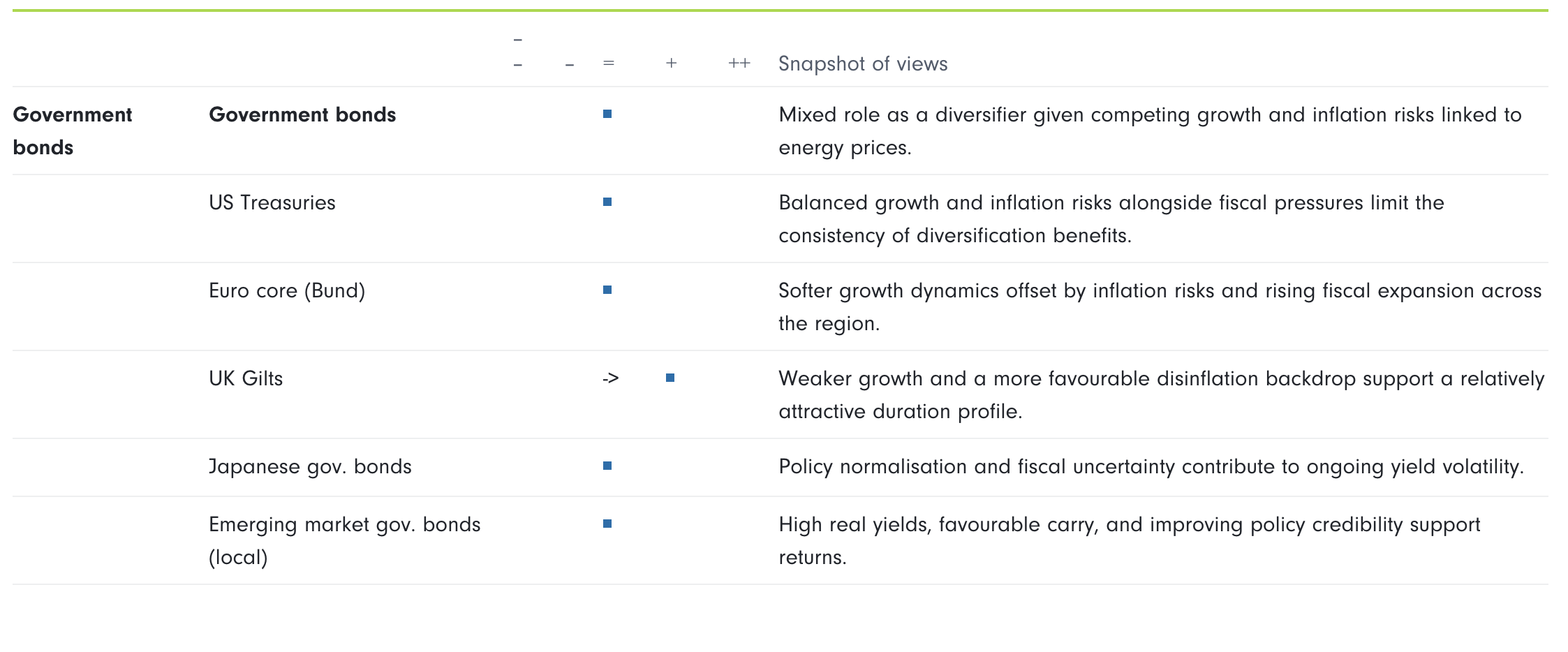

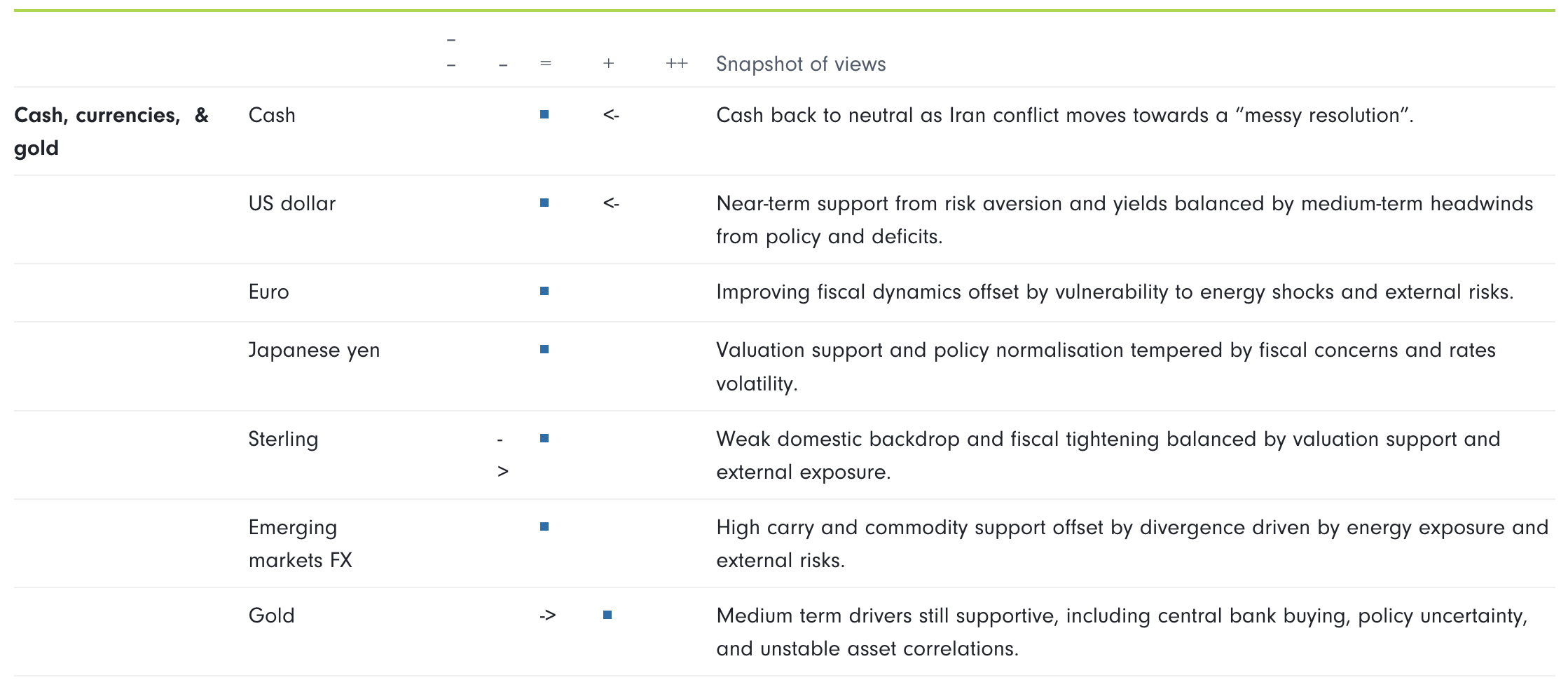

TAA views summary

Source: Fidelity International, April 2026. Views reflect a typical time horizon of 12–18 months and provide a broad starting point for asset allocation decisions. However, they do not reflect current positions for investment strategies, which will be implemented according to specific objectives and parameters. Regional equity views use universes defined by MSCI indices.

Best ideas for investment outcomes

Growth

- Japan and EM equities preferred, particularly Korea, South Africa, and Brazil, supported by structural tailwinds, earnings momentum, and attractive valuations.

- Thematic equities related to the grid upgrade benefit from idiosyncratic return drivers as the US and EU look to accommodate greater demand and more renewable energy.

Income

- Emerging market bonds in select local markets continue to look attractive given elevated yields and commodity-exporting fundamentals.

- Quality income equities provide relative defensiveness and stability, particularly in an environment of higher uncertainty. Dividend growth and strong balance sheets remain key filters.

Capital preservation

- Commodities, particularly energy exposure, have proven to be the most effective hedge in the current environment, providing protection against geopolitical risk and inflation.

- Gold remains a medium-term diversifier, however its behaviour has been less consistent as a hedge during the recent volatility.

- We remain positive on selected real assets, particularly transition materials such as copper, supported by structural demand from electrification, reshoring, and AI demand.

Uncorrelated returns

- Absolute return strategies, driven by active investment decisions and incorporating idiosyncratic sources of risk – particularly those with a focus on tail risk mitigation.

Source: Fidelity International, April 2026. Views reflect a typical time horizon of 12–18 months and provide a broad starting point for asset allocation decisions. However, they do not reflect current positions for investment strategies, which will be implemented according to specific objectives and parameters.

Key views

- Re-engaging with risk as fundamentals hold up: Markets are beginning to look through near-term geopolitical volatility towards resilient earnings and ongoing fiscal support.

- Selectivity key as dispersion rises: Higher uncertainty and less stable correlations are driving greater divergence across regions and sectors, favouring active positioning over broad exposure.

- Preference for Japan and emerging markets: Attractive valuations, improving earnings dynamics, and, in some cases, support from commodity exposure underpin our regional preferences.

- Energy and geopolitics shaping outcomes: Higher oil prices and supply disruption are creating both risks and opportunities, particularly across energy-linked sectors and regions.

Shareholder returns in Japan are rising

Source: Fidelity International, April 2026. Views reflect a typical time horizon of 12–18 months and provide a broad starting point for asset allocation decisions. However, they do not reflect current positions for investment strategies, which will be implemented according to specific objectives and parameters. Regional equity views use universes defined by MSCI indices. Chart source: Fidelity International, Bloomberg, April 2026.