18 Jun 2018

In this multimedia feature, we tackle the thorny issue of growth vs value. On a global level, value stocks have struggled on a relative basis since the crisis over a decade ago. Why has this happened and is this trend finally showing signs of reversing? Expert insight is provided by Fidelity Global Special Situations Fund manager Jeremy Podger

In the last in a series of four articles on market leadership, Jeremy Podger tackles the thorny issue of growth vs value. On a global level, value stocks have struggled on a relative basis since the crisis over a decade ago. Why has this happened and is this trend finally showing signs of reversing?

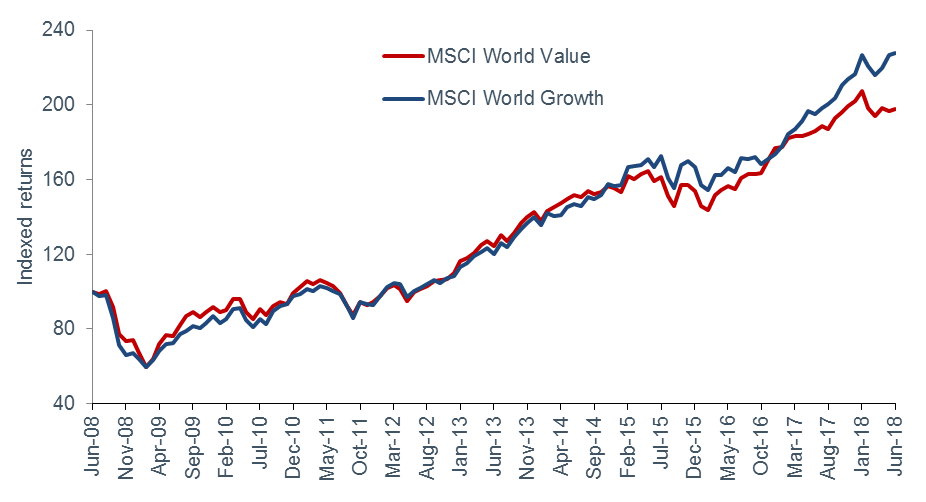

Academics have trawled the data from the past century or more to demonstrate that value has outperformed growth over the long run. But it has been in a prolonged and unprecedented bear phase since the financial crisis 10 years ago.

The cycles of growth and value performance have in the past largely followed interest rate cycles - and we haven’t really seen an interest rate cycle in the past decade. But, as for quality shares, growth has been helped by declining bond yields (effectively making future earnings more important in present value terms).

Performance of growth vs value stocks over the last 10 years

| Apr 13 - Apr 14 | Apr 14 - Apr 15 | Apr 15 - Apr 16 | Apr 16 - Apr 17 | Apr 17 - Apr 18 | |

|---|---|---|---|---|---|

| MSCI World Growth | 17.6% | 19.1% | -3.1% | 17.6% | 14.8% |

| MSCI World Value | 16.0% | 10.9% | -5.3% | 18.9% | 7.9% |

Past performance is not a guide to the future.

Source: Datastream, 30 April 2018. Based on total return in local currency terms.

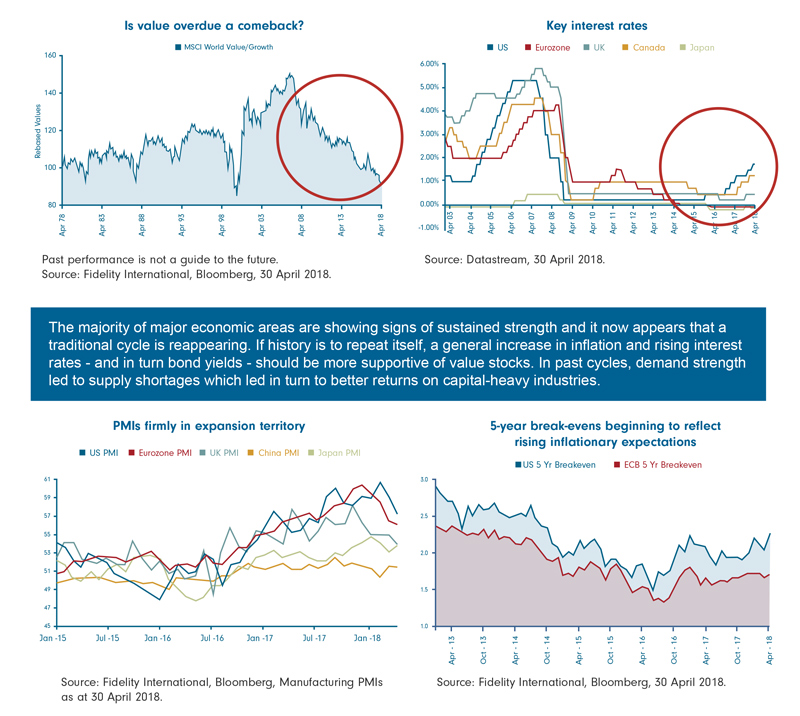

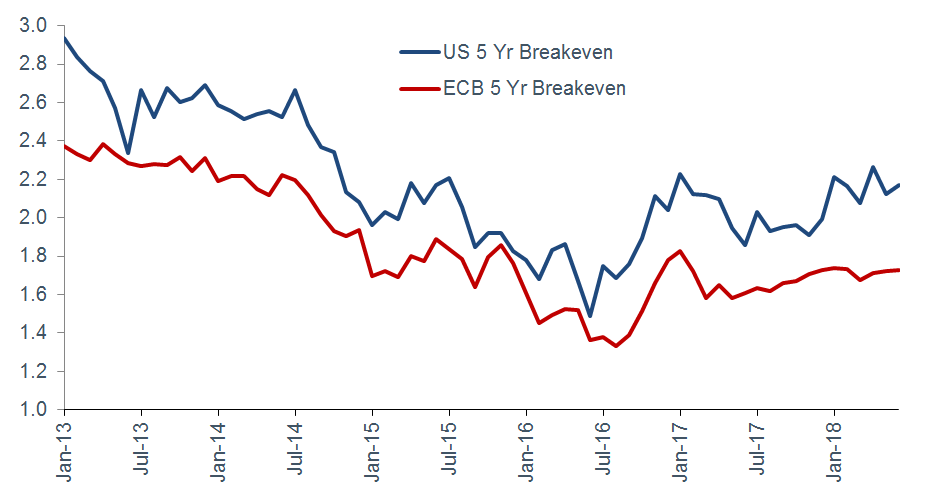

What seems certain is a general rise in inflation and rising bond yields should be more supportive of value stocks. We saw this in the brief value rebound in the second half of 2016 - but all those relative gains have been given back.

Inflationary forces could test the growth vs value dynamic

Fidelity International, Bloomberg, 30 April 2018.

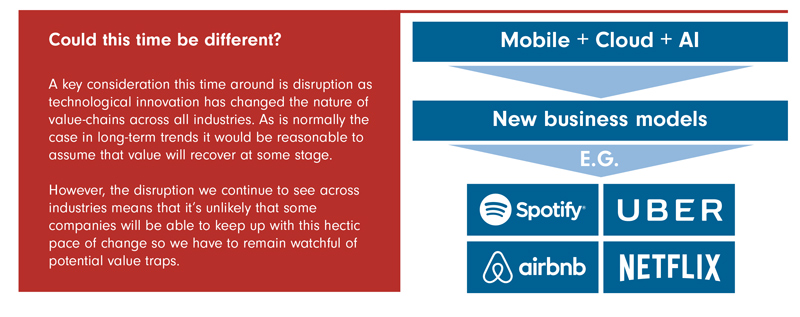

What is going on here? A lot has to do with the extraordinary pace of disruption caused by technology innovation in all sectors of the economy. It is better to be smart than to throw tangible assets at problems these days. And in any case, a huge amount of the investment in really capital-intensive manufacturing has been in Asia where competition remains fierce.

In past economic cycles, demand strength led to supply shortages which led in turn to better returns on capital-heavy industries. Disruption and the changed nature of value chains across all industries mean that it is probably wrong to wait for a rising tide to lift all boats but rather, to mix metaphors, to fear that the devil will take the hindmost. In other words, beware of ‘value traps’.

As is normal in long trends such as this, we would have to say that value will probably recover after most people have finally pronounced the last rites. In some respects it feels as if we are close to this point - but it is not worth betting the house on it.

So how do investors choose the next big themes for the markets from here? When there is a change in market leadership, you have to look at those managers who have been successful in the past and ask whether that manager can adapt to the new changes or whether it is time to change the manager.

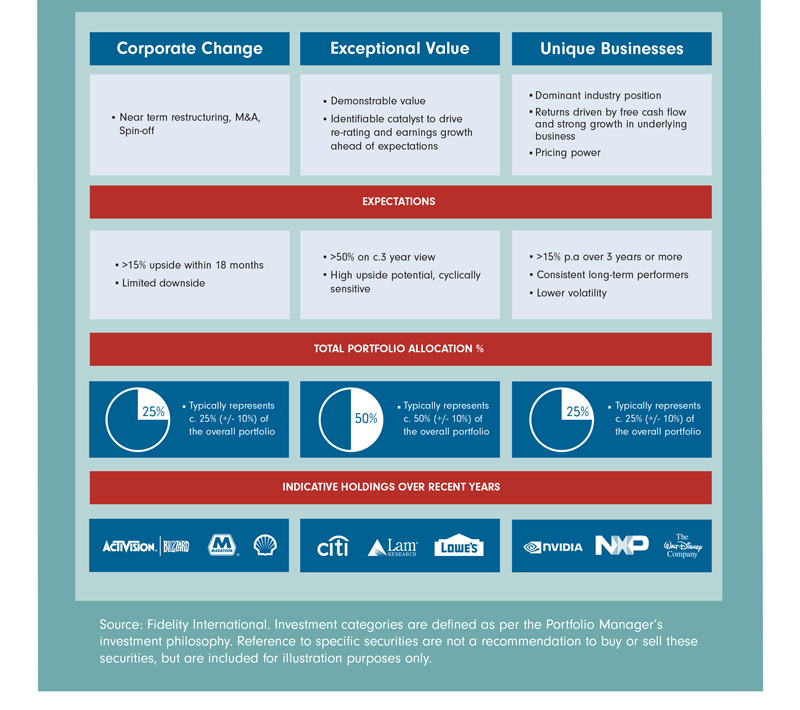

In the Fidelity Global Special Situations Fund, we prefer to deploy many ideas rather than one big one. We have a consistent selection process in three categories of investment types which include both value and growth situations. Which themes come out will largely be a function of which stocks are judged to be most attractive, particularly from the point of view of valuation and long-term profit potential.

Over the past six years, this has led to some great successes in semiconductor companies, in healthcare services, in recovery stocks in Japan and in financial stocks in emerging markets, to name just a few areas. The stock selection discipline is designed both to unearth areas of opportunity that may develop into sustained long-term winners and, we hope, to move out of them when they have run their course.

Jeremy Podger, Portfolio Manager

Jeremy Podger joined Fidelity in February 2012 and manages the Fidelity Global Special Situations Fund and the Fidelity World Fund (SICAV). He is an experienced investor and has been managing global equities mandates for more than 20 years. Prior to Fidelity, Jeremy was Head of Global Equities at Threadneedle, a fund manager at Investec for seven years and a global and pan-European fund manager for Saudi International Bank. Jeremy has a degree from Cambridge University and an MBA from London Business School.