28 May 2026

A more uncertain and fragmented macro backdrop is changing the way investors think about resilience, diversification and market access., Here, our macro and ETF team examine the key forces shaping markets, including geoeconomic fragmentation, the impact of AI, widening return dispersion, and outline how investors can use ETFs selectively within asset allocations.

The current macroeconomic environment looks significantly different from the one that defined much of the post-global financial crisis period. Geopolitics is having a greater impact on market pricing, while inflation remains persistent, particularly in the US and the UK.

The recent Iran conflict has surfaced this tension and impact of markets once more. A contested Strait of Hormuz, continued stockpiling, and higher tariff levels can keep a geopolitical premium embedded in oil prices and add to inflationary pressure around the world. The longer that the conflict persists, the greater the level of volatility and uncertainty that markets will need to contend with, creating real consequences for growth, prices and asset allocations.

At a broad level, fixed income has already begun to adjust to this new regime. Longer-dated government bond yields across major economies have moved materially higher as inflation expectations and term premium have risen. Higher yields improve the starting point for future bond returns, but they also make duration risk more important when inflation is one of the main drivers of market moves. A world of higher inflation risk and structurally higher term premium is not the same as the low-yield, lower-volatility regime many investors grew used to since the global financial crisis of 2008.

Equities on the other side, remain uncertain, with many different factors meeting to generate higher levels of volatility and dispersion. This, combined with fast-evolving macro themes such as AI or demographic shifts, mean that investors require a nimble approach to navigate uncertain markets.

Alongside higher inflation and geopolitical stress, market dispersion is elevated relative to the past decade. Returns are no longer being driven by a narrow set of assumptions or a single regional leadership pattern and many established themes are flagging, while others are establishing themselves further.

Within the US, market concentration remains a central issue. AI-driven valuations with mega-caps at the top of the market make it look more expensive than the broader opportunity set actually is. Looking past those mega-caps that represent some 30% of total capitalisation, much of the market appears more fairly valued. So far this year, flows have moved towards equal-weighted index ETFs in far greater numbers as investors recognise this fact. In a concentrated market, refocusing on fundamentals or more long-term structural drivers can help identify areas of opportunity - there remain many compelling stories further down the market cap spectrum, even in a market dominated by expensive leadership.

In this context, long-term equity exposure remains a crucial component of portfolio construction. Over long horizons, equities have historically had a high probability of beating inflation, supporting their role as a core component of strategic asset allocation. While that does not remove short-term volatility, it does support the case for looking past short term geopolitical or market shocks. Remaining invested, while taking a more selective approach to exposures can help navigate uncertainty and risk.

The diversity of return drivers that are emerging across not only the US, but also markets around the world, enhances the case for a more research-driven and selective approach to allocations. This is especially pertinent when it comes to considering deliberate regional diversification beyond the most concentrated parts of the US equity market, or beyond those sectors that have seen rapid valuation increases due to AI-hype.

While AI and its impact on global markets will likely take time to play out, investors must also assess their approach to the immediate environment. One of the clearest implications of the current regime is that diversification cannot only be looked at through a traditional bond-equity split. In an environment where inflationary volatility is a persistent characteristic, broad government bond exposure can struggle at the same time that equities come under pressure, meaning that alternate means of diversification are needed. That does not weaken the long-term role of bonds, but it does change how investors may need to think about defensive assets.

A more resilient approach may require a broader set of diversification approaches. Gold can still have a role in diversifying some geopolitical and monetary risks, and has still acted as somewhat of a safe-haven in recent geopolitical flashpoints. However, other areas such as private assets or dividend-focused strategies can provide a greater level of diversification in times of volatility. For some of these diversification approaches, ETFs can enable a more dynamic and nimble approach to allocations - a crucial consideration for investors when the macro landscape can change rapidly.

Artificial intelligence is now increasingly relevant not only from a technology angle, but as a broader macro force with implications for growth, productivity, capital spending and market leadership. Its impact is unlikely to be confined to the narrow group of US technology companies that we currently see leading markets. Instead, it is unfolding across a much wider ecosystem that encompasses a greater number of different sectors and demographics than we see at first glance.

The global nature of the AI transition is particularly important in the current market environment. No country is self-sufficient across all parts of the AI value chain, and several Asian markets play a significant role in areas such as semiconductor manufacturing and broader hardware supply chains. China, South Korea, Taiwan and Japan all have important positions within that system, which means the AI story may reinforce the case for thinking beyond the largest US names when assessing where long-term opportunities may lie.

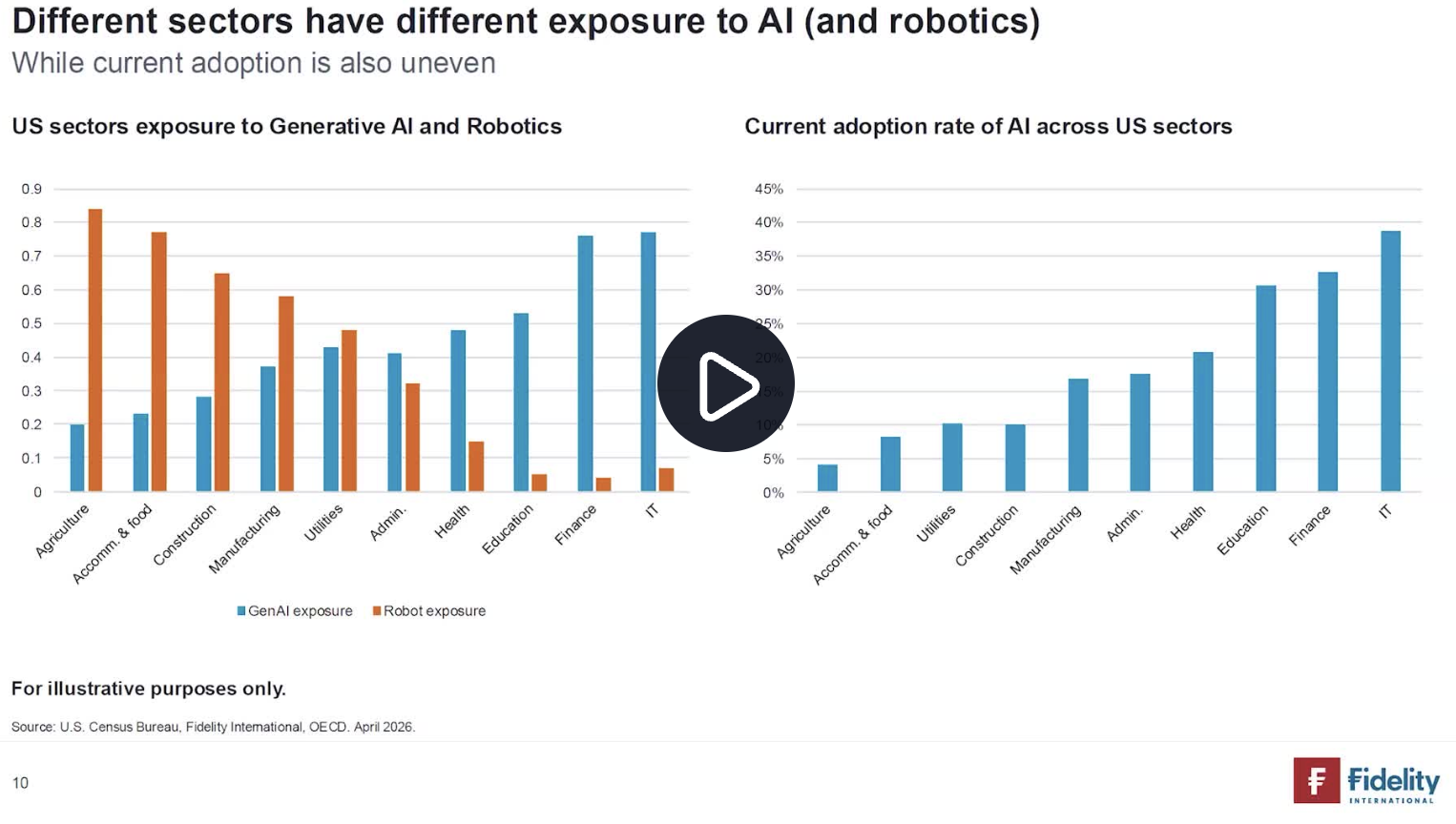

On top of a more global impact, the economic effects of AI are also likely to be uneven across segments of the market. Service-oriented sectors such as technology and finance may face both benefits and disruption earlier, while areas such as manufacturing and agriculture could be affected more through adjacent advances such as AI-integrated robotics.

Over time, AI could support stronger earnings growth and help lift economic growth above long-term averages, but the gains are unlikely to be evenly shared across regions, sectors or businesses. Therefore, selectivity matters. The opportunity set may broaden as AI-adoption and enablement becomes more widespread, but it is unlikely to reward investors taking a simplistic or overly concentrated approach, and may require a deeper integration of research when assessing allocations.

Overall, the backdrop is becoming harder to navigate with yesterday’s assumptions. Inflation is more persistent, geopolitics is a more constant source of risk, traditional diversification is less automatic, and market concentration demands a more selective approach to allocations.

Structural themes such as artificial intelligence may continue to support long-term growth, but their benefits are likely to be distributed unevenly and shaped by a more fragmented global system. This increased dispersion over the longer-term supports the integration of research to a much greater extent in order to make informed portfolio construction decisions. In that environment, ETFs can support investors by enabling a nimble response to market shocks as they emerge, and offer both a flexible and efficient way to implement research-enhanced allocation decisions.