25 Jun 2026

The conflict in the Middle East is lasting longer than initially hoped. Our base case is for a messy resolution. Tensions are likely to persist for some time, with supply chains disrupted and energy carrying a geopolitical premium.

Following the initial shock, investors’ minds are now contemplating the next phase of the conflict. It’s clear the after-effects are likely to linger, with knock-on effects on inflation, growth, and policy decisions. Crucially, these forces will not be evenly distributed across regions or individual countries.

For asset managers, this complex environment needs to be considered when constructing portfolios. We are likely to see increasingly divergent outcomes across both developed and emerging economies. Some countries will be more exposed to higher energy costs and supply disruption. Others nations may benefit from the same dynamics.

Against this backdrop, building resilience within a Model Portfolio Service, for example, requires creating portfolios that are better placed to navigate a wider range of potential outcomes. Importantly, they also need to be able to capture the opportunities that uncertainty creates.

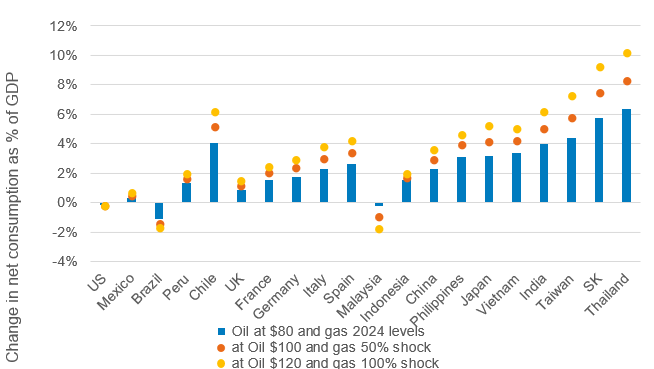

Developing economies sit at the centre of this divergence. The closure of the Strait of Hormuz illustrates how different countries can be impacted by the same shock. Economies heavily reliant on imported energy, like many in North Asia, will be more exposed to higher input costs, weaker growth, and currency pressure. On the flipside, commodity-exporting nations with a positive energy balance are better positioned to absorb, and even benefit from, these dynamics.

These differences will only become more pronounced the longer the Strait of Hormuz remains closed or disrupted. The opportunities, in terms of portfolio construction, will therefore be increasingly driven by country-level fundamentals, policy settings, and sensitivity to external shocks.

Asian economies are bearing the brunt of the energy shock

Source: Fidelity International, Bloomberg, EIA, BP 2025 EI Statistical Review of World Energy, April 2026. Net consumption is calculated as total consumption of oil and gas less oil and gas production. Net consumption is as of 2024. We do not assume any change to net consumption levels across our price shock scenarios. We use Brent for oil prices across countries. We use different gas prices across regions; For Americas we use Natural Gas prices at NYMEX, Europe we use TTF prices and for Asia we use the Japan Korea Marker.

From an investment viewpoint, emerging markets have many attractions. Fundamentals in many regions are improving, valuations remain attractive relative to developed markets, and several central banks have scope to ease policy.

However, the fallout from the Iran conflict means we have to pay closer attention to how these opportunities differ. As a result, we have increased exposure within our own portfolios to regions that offer more attractive fundamentals and valuations, as well as increased macro resilience.

In practice, this means tilting towards Latin America, especially Brazil – a commodity exporter with a positive energy balance. Higher oil prices can support Brazil’s terms of trade, which helps underpin growth and currency stability. This should provide a valuable buffer in an environment where energy prices remain elevated and supply disruption persists.

Brazil’s domestic policy backdrop is also becoming more supportive. Interest rates are on the way down, and while the initial move has been cautious, there is scope for further cuts. The Brazilian stock market tends to be sensitive to changes in interest rates, and a gradual lowering of borrowing costs should support both valuations and corporate earnings. Even after a period of re-rating, Brazilian equities remain at a discount relative to both their own history and the broader emerging market universe. This creates a margin of safety in a more uncertain environment.

What’s more, inflows from overseas have held up relatively well, even as other emerging markets have experienced outflows. In addition, investor positioning remains far from stretched – both domestic and international investors have scope to increase their exposure to Brazil.

As ever, risks are a key consideration for us. The upcoming Brazilian election is likely to influence market sentiment, while a stronger US dollar or tighter global financial conditions would create headwinds for emerging markets more broadly, even for those with relatively supportive domestic dynamics.

As we go forward, dispersion within emerging markets is likely to become an increasing feature of performance. This creates a more nuanced opportunity set.

By tilting our emerging markets exposure towards Latin America, we retain exposure to what we believe is one of the best growth opportunities while also strengthening overall portfolio resilience. By favouring regions that are better aligned with the current macro environment, and tilting away from those that are more exposed to its risks, we believe our portfolios are well positioned for growth and better equipped to navigate uncertainty.

This view is being reflected across the three ranges within the new Fidelity WealthBuilder Model Portfolio Service – Active, Passive Plus and Blended. These open architecture portfolios, all powered by Fidelity’s active heritage but with different investment approaches, offer alternative ways to access Fidelity’s global scale and resources, process and insight, as well as market-leading investment managers from across the industry.