The UK population are returning to the polls, in a bid to resolve the Brexit impasse. Abundant uncertainties about the election result argue against significant positioning in sterling assets in either direction.

My six-year old recently asked me, “Mummy, why are you still talking about Brexit?” Good question. “Well”, I replied, “the UK used to be in a club with the EU, but has decided it doesn’t want to be in the club anymore. But it’s still complicated because the UK needs to decide whether to end its friendship altogether, or stay friends and play with them sometimes at break time”.

The original referendum question didn’t add this nuance. The question was: do you want to be in the club, or not? In a general election on 12 December, the UK population will be asked for more clarification. Exactly what future friendship does the UK want with the EU? This is no ordinary election. This is a new referendum.

Parties will campaign on their vision for this friendship. On one end of the spectrum, the Brexit Party will appeal to those in the UK population that want to break all ties. These individuals have high hopes of creating new friends elsewhere in the global playground and thus are confident any economic challenges will be short-lived.

On the other end of the spectrum, the Liberal Democrats want to remain in the club: to revoke Article 50 and forget the whole thing.

The two traditionally major parties – the Conservatives and Labour Party – are having a much harder time clarifying their Brexit ambitions.

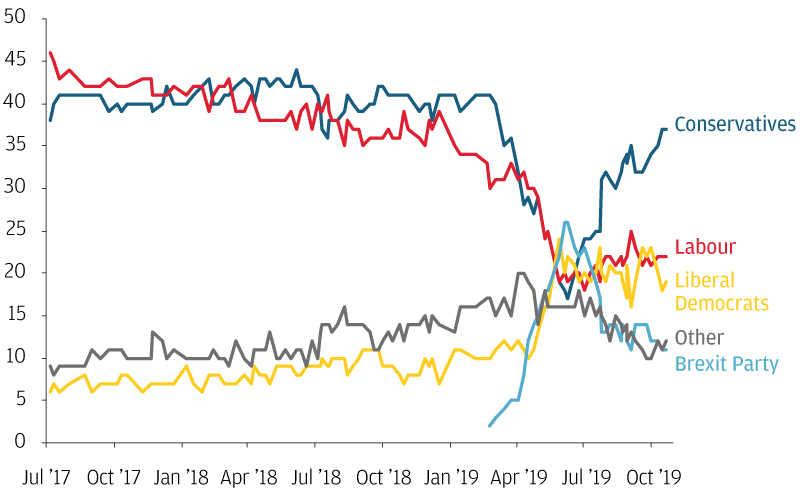

Since Boris Johnson took office as prime minister, his “do or die” approach to Brexit has coincided with an increase in Conservative support, at the expense of the Brexit Party (see chart). However, recent weeks have seen him focus his efforts on a deal and request an extension – something he said he would not do. He must now decide where exactly to position his party on the Brexit spectrum. We suspect he will focus on passing his deal but this leaves the question of whether, as a result, he will lose support to the more definitive stance put forward by the Brexit Party.

UK general election voting intentions

% of respondents

Source: YouGov, J.P. Morgan Asset Management. Data as of 21 October 2019.

The Labour Party are having a similarly hard time defining their Brexit position clearly, though have swayed towards something softer and, when pressed, have outlined a deal based on a customs union. As a result, Labour appears to have lost support to the more clearly defined Liberal Democrats.

In summary there are still a lot of moving parts. And, to make matters worse in terms of predictability, the UK has a first-past-the-post electoral system that has traditionally favoured the Conservative and Labour parties. The strong polling for the Lib Dems and Brexit Party complicates matters. The potential for increased turnout from younger cohorts also makes life harder for the pollsters, as does the resignation of Ruth Davidson as leader of the Scottish Conservatives, given she was credited with bringing 12 MPs to Westminster from north of the Border.

For all these reasons, we will be treating polls with a healthy degree of cynicism. 12 December will be a sleepless night.

What are the implications for markets?

For now, sterling has held on to the gains made since early October, as the imminent threat of no deal has receded. Indeed, markets should take comfort from the fact that the EU will not call time on this saga. If no deal occurs, it will be because the UK has chosen it.

But the coming weeks may generate further market volatility. A majority for the Labour Party, and the potentially unfriendly market policies that would ensue, seems a low probability scenario. However, sterling assets may react negatively to any signs that Boris Johnson is struggling to compete with the Brexit Party, which could push him to return to his no-deal rhetoric. We continue to believe that a no-deal Brexit would coincide with sterling in the region of 1.10 against the US dollar.

By contrast, the Liberal Democrats may continue to be well supported in the polls, and remain-inclined Conservative MPs could keep the pressure on the prime minister to retain a deal-focused approach. If the first-past-the-post system helps Johnson achieve a Parliamentary majority that allows him to pass his negotiated deal, the UK is facing a near-term Brexit reprieve at the same time as a sizeable fiscal expansion in excess of 1% of GDP. Sterling assets would likely cheer such news. In that scenario, it wouldn’t be inconceivable to see sterling rise back towards our fair-value estimate of around 1.40 against the US dollar.

It is also entirely possible, however, that the UK population is as divided as it was three years ago and as a result no party will obtain a majority. While this might appear to be the worst-case scenario for resolving the impasse, it is possible that it would force a cross-party solution to Brexit and ultimately a softer Brexit outcome. After all, if a more comprehensive free-trade agreement was not negotiated over the period of transition, Johnson’s deal could still see significant disruption to UK trade.

Given the twists and turns likely in the coming weeks, significant positioning in sterling assets in either direction looks unwise. I will be sticking to the tactics I deployed in my school days – observing playground politics from a distance.

Important information

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own professional advisers, if any investment mentioned herein is believed to be suitable to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields is not a reliable indicator of current and future results.

J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. This communication is issued in the United Kingdom by JPMorgan Asset Management (UK) Limited, which is authorized and regulated by the Financial Conduct Authority, Registered in England No. 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.