16 Jun 2022

For professional investors only

Hamish Chamberlayne, Head of Global Sustainable Equities, answers key questions on the drivers shaping environmental, social and governance (ESG) and sustainable investing in 2022 and beyond.

Equity markets have faced stiff headwinds this year, and for ESG investing it has been a near perfect storm. The Russia/Ukraine conflict, rising inflation, slowing growth, central bank activity, and the lingering impact of the pandemic have created much uncertainty at a macroeconomic level. This has combined with a shift in market rhetoric to a strong anti-growth and less positive ESG stance leading to stronger performance from sectors typically not associated with sustainable investing, such as energy, defence, tobacco and commodities. The good news, however, is that we see this as a natural correction and a logical outcome of the excesses of the ESG bubble that formed in markets last year.

2021 saw strong upward momentum for all things ESG and growth stocks with a ‘story’ behind them. Appetite reached peak levels for these ‘story’ stocks, with the promise of what’s to come in the future trumping cash flows and profitability today. This was particularly apparent with demand for special purpose acquisition companies (SPACs), ‘shell companies’ formed to raise money through an initial public offering to buy another company, often with an ESG angle. These included companies associated with solid-state batteries, hydrogen, plastic recycling, fuel cells, and new electric vehicles.

We put SPACs in the same category as highly speculative crypto and meme stocks (which receive strong followings based on online and social media platforms). While the stories could potentially look exciting, our approach was to avoid all SPACs. We believed this to be a vast speculative ESG bubble and, in line with our long-held approach, did not participate. In 2022, we have seen the bubble burst in a high-profile way.

While the current environment is challenging for growth and ESG, it is actually reinforcing the medium-term trends we are focused on. Energy security, economic resilience, and supply chain re-localisation are all very aligned with our sustainability themes. Regulators and governments have also maintained their focus on ESG with steps being taken to support the migration to a more sustainable global economy. Recent sustainability developments included the latest report from the Intergovernmental Panel on Climate Change, which suggested that global warming is happening at a faster pace than previously believed and that the need for action is intensifying. Meanwhile, the Taskforce on Nature-related Financial Disclosures (TNFD) released the first version of its risk-management framework, the US Securities and Exchange Commission said that it is planning to improve climate disclosures, and the European Union agreed to introduce a carbon tax on imports of highly polluting goods such as steel, cement, and fertilisers from 2026.

Short-term challenges for ESG investing have been meaningful, but the longer-term direction of travel is unchanged, and has potentially accelerated. We therefore view the volatility as an overdue shakeout of the excesses in the system and supportive of the sustainability investment trends that we as a team are focused on.

Energy stocks have been some of the big winners this year and sustainable investment approaches, such as our own, that do not offer exposure to oil and gas companies have been negatively impacted. While a negative for ESG and sustainable investing in the short term, we believe higher oil and gas prices will accelerate the adoption of products and services from companies providing sustainable solutions. Sustainability is closely linked to innovation and we seek businesses that are transforming the world for the better. An obvious example is the renewable energy sector and related development projects. As oil and gas prices rise, the number of projects that can generate acceptable returns increases. More broadly, we are witnessing greater demand for many renewable projects.

Another example would be electric vehicles (EVs). Higher oil and gas prices make electric vehicles more attractive to consumers. While we no longer have direct exposure to EV manufacturers, we do like companies that supply key technologies within electric vehicles. This can be connectors, wiring, semiconductor chips or electric motors, for example.

In terms of inflation and the rate of change of interest rates, which is currently worrying markets, we believe this should be viewed as a move back towards normalisation. From a relative perspective the increase in interest rates is significant given the starting point of close to zero but, taking a step back, interest rates are still at multi-decade lows. We therefore continue to see these levels as representing favourable conditions for growth.

Currently, there is a common narrative in the media that growth suffers in a rising interest rate environment. This is not actually based on fact. Looking back to the early 1990s, there have been four US Federal Reserve interest rate tightening cycles and in three of those four, growth outperformed value. In addition, technology was often the best sector to invest in during those four periods. While growth may not outperform value this time, we do think it is important to point out that this narrative is detached from recent history.

It is important to note that we are long-term investors, which means not reacting to short-term trends, notably the sector moves and style rotation we are currently experiencing. We believe the trends we have built our approach around remain very much in place and, if anything, have accelerated. When we look globally, we see a lot of concerns around supply chain fragility, economic resilience, reshoring manufacturing, re-localising supply chains, and energy independence. These play into the sustainability trends that we are focused on. We therefore see volatility as an opportunity to take advantage of a market shaped by short-term fear. This has meant adding to names where we have conviction in the long-term thesis.

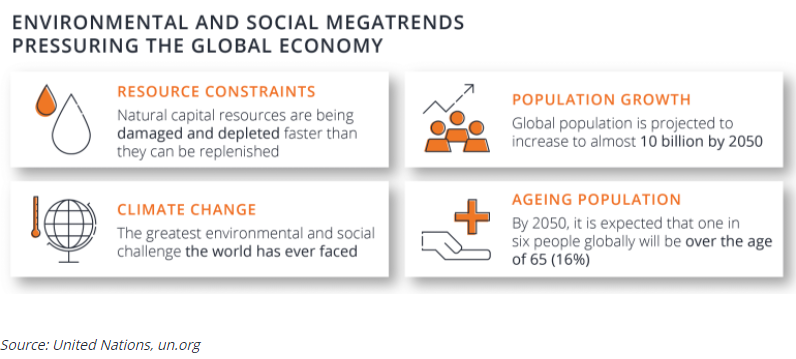

We believe the sustainability challenge is captured by four megatrends – and these will continue to drive the global economy of the future:

Our focus has always been to seek companies with proven business economics and cash flows. Many sustainable companies offer strong compounding potential because they provide solutions to key societal and environmental challenges. They also have the potential to do well in an inflationary environment. Many have pricing power and are offering solutions that, in many cases, are deflationary. Technological innovation is a case in point as it presents efficiencies in the production of goods and services at scale. Lower-cost energy via renewables is another deflationary benefit.

It is very important to distinguish between the short, medium and long term. There is no doubt we are experiencing some of the most adverse investment conditions over the last decade. However, for the first quarter, this contrasts with what we are seeing and hearing from the companies we invest in. Examining companies’ strengths and weaknesses from a fundamental analysis point of view currently shows many positive signs, good growth, and resilience in business models.

At the country level, governments are increasing their focus on making investments in renewable energy and helping to re-shore and localise supply chains. This has led to announcements from semiconductor companies on the building of new fabs (factories for making advanced electronic products) in the US and in Europe. This has led to those companies supplying the parts, equipment, and technologies that go into these new factories reporting increased order books, rising demand, and a strong product pipeline.

This emphasises the importance of focusing on the true health of companies today as opposed to the ‘stories’ of tomorrow. The short-term challenges for ESG investing have been meaningful, but, in our view, the longer-term direction of travel is unchanged. While the ‘weather’ will continue to blow through markets, we welcome the longer-term opportunities they bring.

Visit our website to find out more about the Janus Henderson Global Sustainable Equity strategy and discover the latest expert insights from the team.

Important information

This document is intended solely for the use of professionals, defined as Eligible Counterparties or Professional Clients, and is not for general public distribution.

Past performance does not predict future returns. Marketing communication. The value of an investment and the income from it can fall as well as rise and investors may not get back the amount originally invested. There is no assurance the stated objective(s) will be met. Nothing in this document is intended to or should be construed as advice. This document is not a recommendation to sell, purchase or hold any investment.

There is no assurance that the investment process will consistently lead to successful investing. Any risk management process discussed includes an effort to monitor and manage risk which should not be confused with and does not imply low risk or the ability to control certain risk factors.

Various account minimums or other eligibility qualifications apply depending on the investment strategy, vehicle or investor jurisdiction. We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

Issued in Europe by Janus Henderson Investors. Janus Henderson Investors is the name under which investment products and services are provided by Janus Henderson Investors International Limited (reg no. 3594615), Janus Henderson Investors UK Limited (reg. no. 906355), Janus Henderson Fund Management UK Limited (reg. no. 2678531), Henderson Equity Partners Limited (reg. no.2606646), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Henderson Management S.A. (reg no. B22848 at 2 Rue de Bitbourg, L-1273, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier). Investment management services may be provided together with participating affiliates in other regions.

Janus Henderson, Knowledge Shared and Knowledge Labs are trademarks of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.

D10068