19 Dec 2022

John Pattullo and Jenna Barnard, Co-Heads of Global Bonds, believe the confluence of attractive yields and an inflection point in rates should make 2023 an opportune year for high quality investment grade and government bonds.

Every so often, ideal conditions present themselves. For the titan arum – the world’s largest unbranched flower – it can be anything between two to ten years between blooms, but when it flowers, the results are impressive. We think high quality investment grade bonds, especially government bonds, are in a similar sweet spot heading into 2023, as a confluence of attractive yields and an inflection point in rates opens up the potential for strong returns.

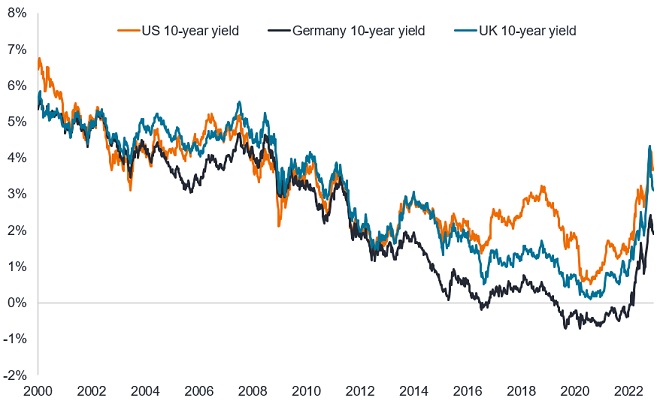

For bond markets, policy tightening in 2022 to tackle inflation was painful as yields rose. Yet the price correction lifted government bond yields back to levels not seen in more than a decade. It was a similar story with investment grade corporate bonds where both credit spreads and yields moved higher.

Figure 1: Yields on government bonds

Source: Bloomberg, Generic US Government Bond 10-year yield, Generic UK Government Bond 10-year yield, Generic Germany Government Bond 10-year yield, 1 January 2020 to 29 November 2022. Yields may vary and are not guaranteed.

The rapidity and magnitude of central bank tightening caused yield curves to flatten and invert, meaning that shorter-dated bonds are paying similar (if not higher) yields than longer-dated bonds. This is creating a rare opportunity for investors to earn a higher income from holding shorter-dated bonds than longer-dated bonds, while also being exposed to less interest rate risk. For example, at the end of November 2022, yields would have to rise by a further 282 basis points (a so-called breakeven) to wipe out the positive total return from shorter-dated US 1-3 year investment grade corporate bonds. This compares with a breakeven rise of 78 basis points for US investment grade corporate bonds in general.1

Attractive income levels on bonds, however, are only half the picture. We think 2023 will also be an inflection point for the rates cycle – as central banks shift their policy in response to declining inflation and an economic downturn. This means that while we like short-dated bonds, there may be an opportunity cost to holding only short-dated bonds and that is potentially foregoing bigger capital gains from holding longer-dated bonds as rates decline.

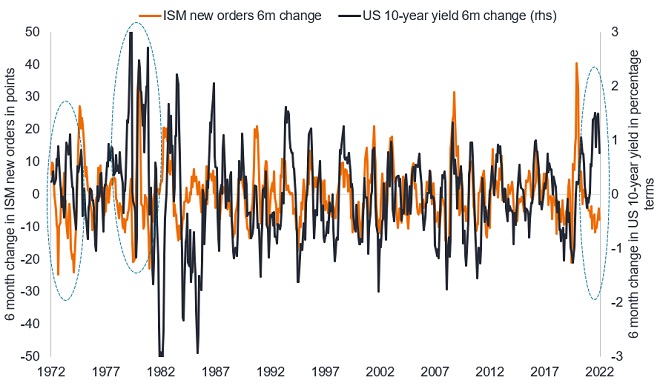

Bond yields have often overshot when core inflation spikes heading into an economic downturn. This decoupling of government bond yields from economic prospects occurred in late 2022 as bond yields rose despite manufacturing new orders declining (Figure 2). We expect government bond yields to recouple with the economic data. From above 4% in the fourth quarter of 2022, we think the US 10-year government bond yield could be close to 2% by the end of 2023. This could lead to strong capital gains on government bonds and should also have positive implications for better quality investment grade corporate bonds, since these bonds are typically sensitive to rate moves.

Figure 2: ISM new orders versus US 10-year government bond yield

Bond yields overshoot when core inflation spikes into growth downturns (circled)

Source: Bloomberg, Janus Henderson Investors, Institute for Supply Management (ISM) manufacturing new orders, US 10-year government bond yield, 30 November 1972 to 30 November 2022. Past performance does not predict future returns.

There is no guarantee that past trends will continue or forecasts will be realised.

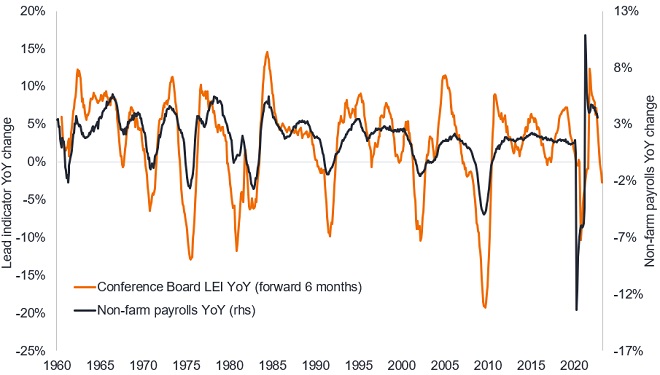

We think we are progressing through a typical economic cycle, with the over-stimulus of the past couple of years giving way to a downturn and recession as policy tightening bites. Lead economic indicators are flashing red. Pain is already being felt in the housing market and corporate earnings appear to be peaking. We think it is only a matter of time (as soon as early 2023) before non-farm payrolls begin to reflect other employment data that companies are shedding jobs. In the US, the Household Survey is already registering job losses while data on withheld employment taxes appears to support the falls in employment seen in the survey.2 The Conference Board Leading Economic Index (LEI) – a highly reliable indicator on employment since the 1960s – suggests non-farm payrolls are set to tumble.

Figure 3: LEI leads employment by around six months

Source: Bloomberg, Janus Henderson Investors, Conference Board Leading Economic Index (LEI) for the US advanced by six months, US Bureau of Labor Statistics, non-farm payrolls. 30 November 1972 to 31 October 2022. Past performance does not predict future returns.

Markets are pricing in a pause in rate hikes in early 2023 by the US Federal Reserve (Fed), followed by a plateau while it assesses the landscape, with a cut maybe coming in late 2023.3 We are not convinced this is how 2023 will unfold. More importantly, it is not how the Fed typically operates. The Fed rarely stands pat. Back in the 1970s and 1980s, it hiked rates until it had control of inflation and then immediately started cutting. Its tolerance of rising unemployment was low.

We think the Fed will take fright and start cutting rates after a few negative non-farm payroll prints – and this could come as early as the first half of 2023. Recessions kill inflation, so if unemployment is rising, we believe the Fed will look again at its dual mandate – stable prices and full employment – and switch to paying more attention to the second part.

This shift in policy is reliant on inflation coming down but we already think inflation has peaked in the US and could come down rapidly in 2023 in Europe as well despite the distortions caused by the energy crisis. Commodity and freight prices have tumbled and this should help pull down inflation numbers. A collapse in broad money growth also suggests that the recent upsurge in inflation is set to wash out over the course of 2023. Even lagging measures, such as market rents, are now softening.

None of the key economic lead indicators we look at have even bottomed so we expect to see further economic deterioration and struggle to see the economy achieving a soft landing. In such an environment we think there is little to be gained from stretching too far in terms of credit risk, particularly as credit spreads on sub-investment grade high yield bonds are pricing in a soft landing and would be vulnerable to widening in a recession. A sell-off in high yield could potentially create a great buying opportunity for this asset class later in 2023 but we see no reason to be an early hero when the risk-adjusted reward potential is so appealing today in investment grade bonds.

The risk to our view is that data does not co-operate, with the jobs market remaining robust and inflation refusing to fall. If that is the case, however, then we would expect to see central bank policy being more restrictive and the economic downturn being even more severe – an outcome that would ultimately favour higher rated bonds, particularly sovereign bonds, as investors would seek relative ‘safe havens’. As we see it, we think there is simply too much data stacking up in favour of our view that we are in touching distance of investment grade government and corporate bonds putting on a strong display in 2023.

1Source: Bloomberg, Janus Henderson Investors, ICE BofA US Corporate Index, ICE BofA 1-3 Year US Corporate Index, at 30 November 2022. Note. The calculation of the breakeven is the yield to worst divided by the modified duration. Basis point (bp) equals 1/100 of a percentage point. 1 bp = 0.01%, 100 bps = 1%. Yields may vary and are not guaranteed.

2Source: US Bureau of Labor Statistics, Current Population (Household) Survey employment level, Refinitiv Datastream, US Withheld Income and Employment Tax, at 30 November 2022.

3Source: Bloomberg, Fed Funds Futures, 6 December 2022.

Important Information:

The views presented are as of the date published. They are for information purposes only and should not be used or construed as investment, legal or tax advice or as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. Nothing in this material shall be deemed to be a direct or indirect provision of investment management services specific to any client requirements. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent, are subject to change and may not reflect the views of others in the organization. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. No forecasts can be guaranteed and there is no guarantee that the information supplied is complete or timely, nor are there any warranties with regard to the results obtained from its use. Janus Henderson Investors is the source of data unless otherwise indicated, and has reasonable belief to rely on information and data sourced from third parties. Past performance does not predict future returns. Investing involves risk, including the possible loss of principal and fluctuation of value.

Not all products or services are available in all jurisdictions. This material or information contained in it may be restricted by law, may not be reproduced or referred to without express written permission or used in any jurisdiction or circumstance in which its use would be unlawful. Janus Henderson is not responsible for any unlawful distribution of this material to any third parties, in whole or in part. The contents of this material have not been approved or endorsed by any regulatory agency.

Janus Henderson Investors is the name under which investment products and services are provided by the entities identified in Europe by Janus Henderson Investors International Limited (reg no. 3594615), Janus Henderson Investors UK Limited (reg. no. 906355), Janus Henderson Fund Management UK Limited (reg. no. 2678531), Henderson Equity Partners Limited (reg. no.2606646), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Janus Henderson Investors Europe S.A. (reg no. B22848 at 2 Rue de Bitbourg, L-1273, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier).

Outside of the U.S.: For use only by institutional, professional, qualified and sophisticated investors, qualified distributors, wholesale investors and wholesale clients as defined by the applicable jurisdiction. Not for public viewing or distribution. Marketing Communication.

Janus Henderson, Knowledge Shared and Knowledge Labs are trademarks of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.