09 Jul 2026

Geopolitical tensions are accelerating fragmentation of the global economy. Governments are prioritizing energy security, domestic industrial capacity, and diversified supply chains over efficiency, raising costs and making markets more sensitive to shocks.

Markets have remained relatively strong so far this year, supported by corporate earnings, AI‑driven growth, and limited spillover into global demand. However, repeated shocks could test this resilience if higher energy prices, tighter supply chains, and volatile inflation expectations weigh on financial conditions and risk appetite.

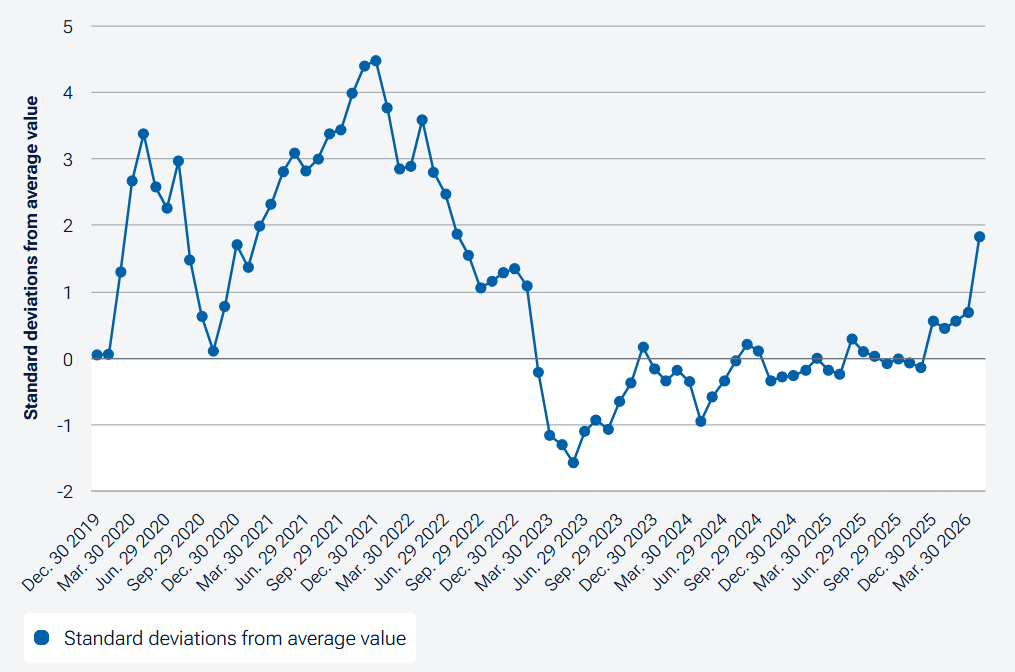

With global supply chain pressures rising again (Figure 1), security means different things across regions. Large economies are seeking more domestic production, while others are building redundancy through diversified suppliers, inventories, and logistics networks. These shifts reduce reliance on the most efficient provider, raising costs and complicating inflation.

(Fig. 1) Energy shocks and AI demand are lengthening delivery times

As of April 30, 2026.

Sources: Global Supply Chain Pressure Index (GSCPI), Federal Reserve Bank of New York.

Notes: The GSCPI gauges supply chain conditions. A positive standard deviation indicates likely supply chain pressures. GSCPI readings for the most recent months can be revised as realized data become available, replacing the imputed values generated through principal component analysis. Further, for some series, mainly the Bureau of Labor Statistics airfreight cost indices, each new release comes with revisions to up to 12 months of previous data. Thus, revisions can have an impact up to a year back in time.

Fragmentation is likely structurally inflationary as reshoring, tariffs, supply chain duplication, and higher defense spending lift costs globally. This points to a tougher growth/inflation trade‑off for central banks, more volatile policy paths, and greater dispersion in currencies and interest rates.

Central banks may face pressure to accommodate higher spending, even at the expense of inflation targets. Defense, technology, and critical infrastructure remain central to this transition. Europe and parts of Asia are exposed to external shocks, reinforcing the need for strategic investment, key commodity reserves, and secure supply networks. Rising tensions are prompting a reassessment of security assumptions, with greater emphasis on cyber capabilities and local defense capacity.

For investors, this points to an environment in which geopolitical risk carries a steeper premium. Regional divergence is likely to widen, with resilient economies and strategically important sectors benefiting from policy support, while globally exposed and trade‑sensitive sectors face pressure.