22 Sept 2023

In a more volatile, multipolar world, should investors be reconsidering portfolio allocations and revisiting the opportunities on offer across Asia? Investment Directors Catherine Yeung and Vanessa Chan outline the attractive growth potential and diversification characteristics of Asia’s financial markets in the wake of recent macro and geopolitical shifts.

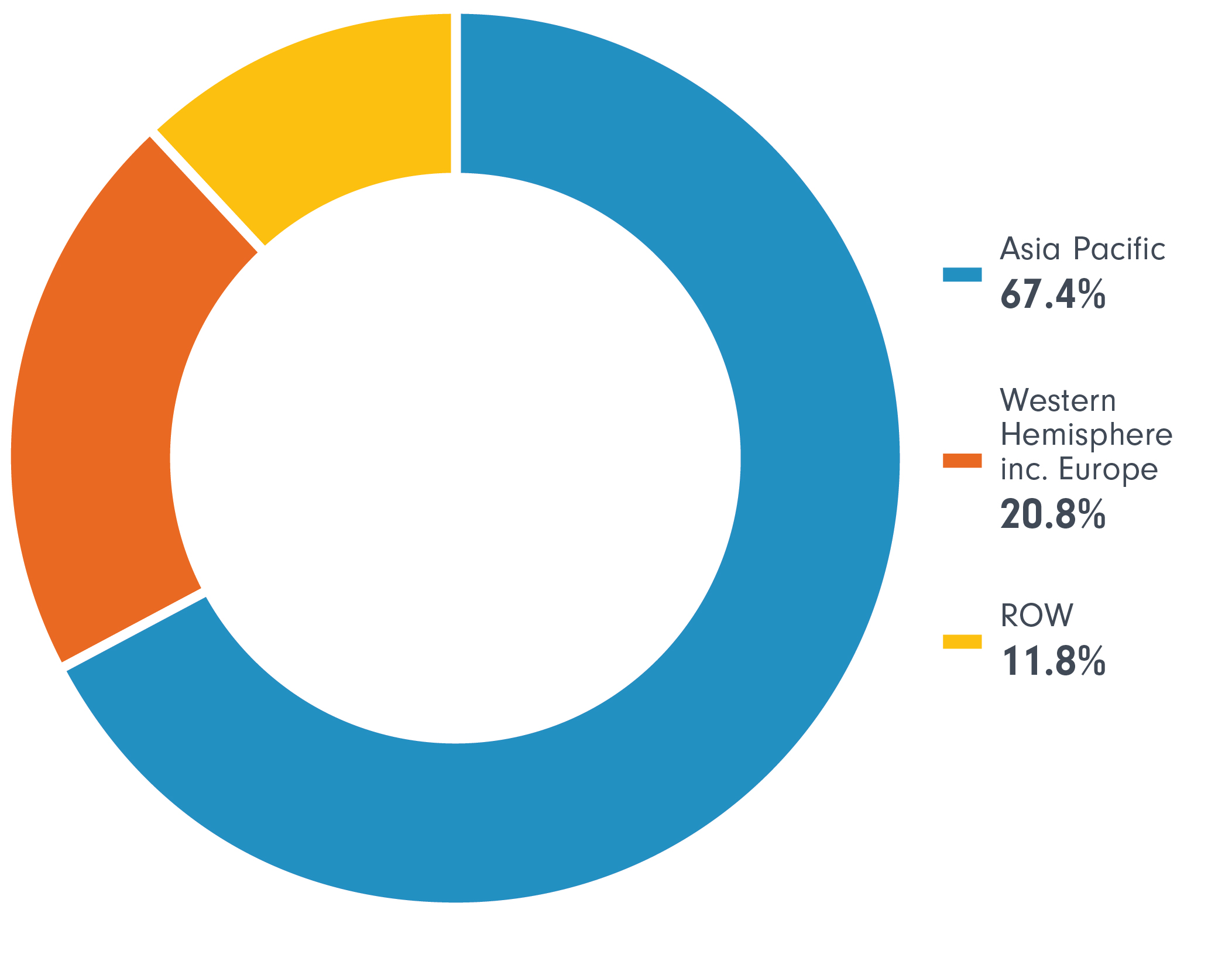

As investors consider their global portfolio allocations in a fresh light, given significant macroeconomic and geopolitical shifts this year, Asia broadly — even allowing for current China concerns — offers valuable diversification and growth potential, with the region forecast to contribute approximately 70% of global growth in 2023.

Projected share of global growth in 2023

Source: IMF, World Economic Outlook, April 2023.

Note: Groupings based on IMF Regional Economic Outlook classification.

Despite recalibrated market expectations on China GDP growth and policy support, the credible case for investment in China continues to draw on:

While geopolitics cannot be ignored, we believe Sino-US trade dependency will continue to bring both parties to the table and set a tone of “de-risking” rather than “de-coupling”.

Asia is not China and broader Asia offers depth, breadth and attractive relative macro-fundamentals as 2023 has shown.

Asian high-level fundamentals hold up well on a relative basis. Corporate issuer credit metrics remain broadly solid and equity valuations are attractive relative to developed markets. On sustainability, there is potential for significant structural growth in Asia across a range of themes, including better access to good health, energy transition and financial inclusion.

In practice, we see considerable nuance and dispersion both within domestic markets and across Asia. Key success factors to investing across the region therefore include:

Not allocating to Asia or maintaining a significant underweight to Asia risks missing out on extremely valuable, nuanced diversification and opportunity at a time when diversification and growth are at a premium.

Important information

This information is for investment professionals only and should not be relied upon by private investors. Past performance is not a reliable indicator of future returns. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of investments in overseas markets. Investments in emerging markets can be more volatile than in other more developed markets. The value of bonds is influenced by movements in interest rates and bond yields. If interest rates and so bond yields rise, bond prices tend to fall, and vice versa. The price of bonds with a longer lifetime until maturity is generally more sensitive to interest rate movements than those with a shorter lifetime to maturity. The risk of default is based on the issuers ability to make interest payments and to repay the loan at maturity. Default risk may therefore vary between government issuers as well as between different corporate issuers. Due to the greater possibility of default, an investment in a corporate bond is generally less secure than an investment in government bonds.