23 Jun 2023

After years of political turbulence which have caused innumerable headaches for UK equity investors, the UK now seems to be in the early stages of a calmer period, which could see it regaining some of its past reputation as a well-run advanced economy. Against this backdrop, Fidelity UK Select Fund portfolio manager Aruna Karunathilake reviews the market environment and outlines why he is feeling increasingly optimistic on the outlook for UK equities.

Key points

Excitement over?

From the Scottish independence referendum through to Brexit and Liz Truss’s short-lived experiment with unfunded tax cuts, UK equity investors have experienced plenty of policy uncertainty in recent years. However, when we look forward, the ideas put forward by the main political parties have converged back into the centre ground. It is nothing like the 2019 election when voters were asked to choose between Jeremy Corbyn’s far-left agenda and Boris Johnson’s push for a hard Brexit.

The Starmer vs Sunak contest is more akin to Blair vs Hague in 2001 when there was little substantive difference in economic policy. Obviously, things can change after an election, but the recent round of press interviews given by the shadow chancellor, Rachel Reeves, indicate a sensible, safety-first approach to the economy very similar to the one taken by Jeremy Hunt since he took the reins last autumn. In fact, the UK stands out as one of the few major economies that does not either have a populist party in power or one poised to challenge at the next election.

Reasons to be positive

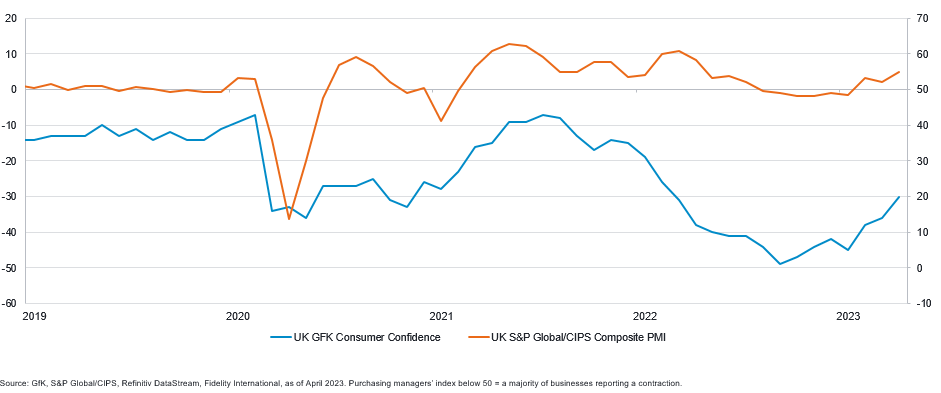

If politics aren’t going to be a big driver, then what about the domestic economy? Here too there are reasons for optimism. The Bank of England (BoE) has quietly removed its forecast of the economy going into recession this year. While growth remains sluggish (the BoE now forecasts GDP growth of +0.25% in 2023 versus their previous estimate of -0.5%), there are encouraging signs beneath the surface. Consumer confidence, while still decidedly negative, has picked up from the lows and businesses are also feeling a bit more confident with the PMI (Purchasing Manager survey) also ticking up a little.

Some economic indicators picking up

Even the housing market, widely tipped to collapse last autumn, is showing signs of life with Rightmove and Zoopla reporting a pickup in early indicators of demand such as new buyer inquiries, new instructions and sales agreed.

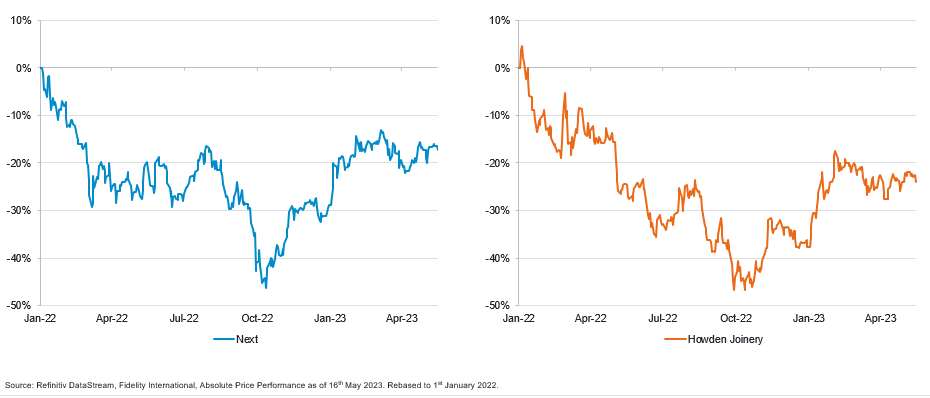

The equity market is an efficient discounting mechanism, and it has re-evaluated the outlook for UK domestic companies after sentiment towards the UK reached its nadir in the wake of September’s mini budget. Companies such as Next and Howden Joinery, which we have previously highlighted as being solid long-term businesses trading at attractive valuations, have begun to recover.

Next and Howden’s see a recovery in stock prices

Of course, risks remain with rising interest rates continuing to put pressure on consumer budgets with the BoE estimating only one third of mortgage borrowers have so far felt the pain of higher rates due the lag introduced by 85% of loans being fixed rate. Hence, we are yet to see the full impact on consumer spending from the rate hikes seen so far. However, there are positives too with companies we meet reporting that wage pressures are moderating and supply chain and logistics bottlenecks (remember the tanker driver shortages?) have eased considerably. This, coupled with lower energy prices, mean we could be close to the end of the rate hikes.

While the economic outlook remains uncertain in the face of rising rates and associated stresses such as the LDI Pension issues and recent US bank failures, it is possible we have already passed the point of peak uncertainty for UK equities. At the very least, politicians don’t look like they will be putting a spanner in the works anytime soon!

Important information

This information is for investment professionals only and should not be relied upon by private investors. Past performance is not a reliable indicator of future returns. Investors should note that the views expressed may no longer be current and may have already been acted upon. The Fidelity UK Select Fund has the potential of having high volatility either due to its composition or portfolio management techniques. It can also use financial derivative instruments for investment purposes, which may expose it to a higher degree of risk and can cause investments to experience larger than average price fluctuations. Reference in this document to specific securities should not be interpreted as a recommendation to buy or sell these securities, but is included for the purposes of illustration only.